2022 Year End Projections

SP500, NQ, Tesla over heated

Alright, so we’re mature enough to know predictions are futile, yet a necessary evil to gauge risk vs reward profiles. We have seen enough, decades in fact of merciless moves in all markets that we cover from bonds, to equities to metals and energies, no market is immune from volatility. A recent observer asked us for our opinion on the upcoming year and we are certainly glad to oblige and put our two cents in, for whatever that may be worth…

We know 2022’s big story will be the FED and its taper then post taper rate hike cycle. Well we know it won’t be much of a cycle as the minute the equities start to flat line or tumble the FED will have to reverse course. For those that don’t understand our modern day monetary system its really not that complicated. However it is driven by shadow banking forces that use monetary leverage and esoteric complex derivatives that pretend to give the semblance of risk offset, but we know the truth, none of that works when you get a massive one off liquidity event, especially bond market style events. Hey but it paints a good picture for the chief risk officer and their army of statisticians as the present to the investment advisory committee.

In regards to the monetary system, The Federal Reserve and the US Treasury are effectively working in unison, and their role in our monetary production is paramount to the appreciation of nominal pricing in all asset classes from global equities to domestic real estate prices. The wrinkle in this mess is two fold:

One, state corporations hell bent on collecting their rake via taxes and distorting affordability in the housing market as taxes eat up nearly 50% of all monthly mortgage payments and

Two, the massive concentration of wealth that is guaranteed by the central planners bond buying programs as those first inline to the spigot leverage this new found cash and buy all and every asset they can.

The final point in this monetary mechanism is that we need to realize that since the Federal Reserve is effectively run by the US treasury,

does anyone honestly think the US government will tolerate higher interest rates?

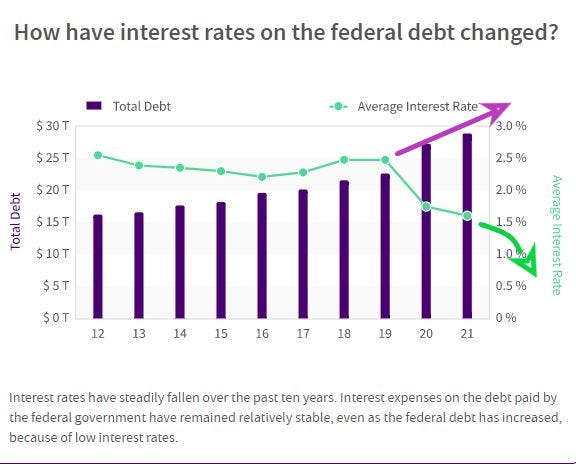

With $29.5 Trillion in debt, a mere 1% rise means an extra $295 billion, certainly not a paltry sum by any means, well you get the picture. In fact it seems as if 2019 was the singularity point by which higher debt can only be sustained with perpetual lower rates, as this chart clearly posits:

With Covid still being pushed as a pandemic of epic proportions, despite the fact we have known preventative treatments, you have certain states willing to push the brink of insolvency even further for both itself and its local citizenry. As far as those state governments that continue to push authoritarian style lockdown and economic killing policies, well get used to meme’s like this:

Eventually the intelligent people wake up and in fact Illinois saw a massive net loss last year of over 114k, we expect this to continue especially as the mayor of Chicago continues on her pathway to destruction.

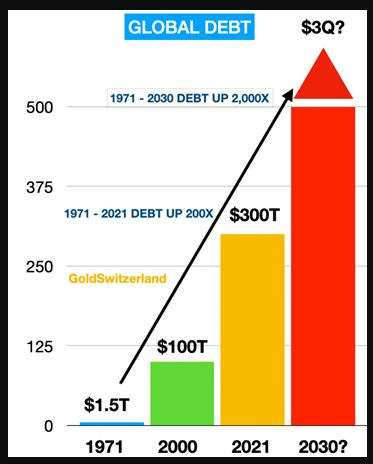

Look there are no free lunches and with debt running out of control, yes we will see inflation, yet this is exactly what the FED wants, especially when we see a juicy debt expansion chart like this:

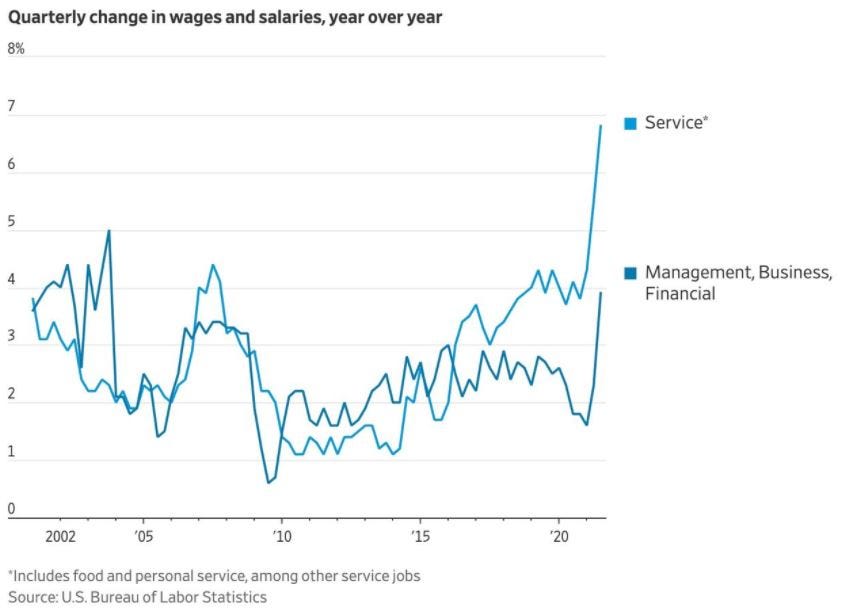

We will expect wage inflation to continue to offset discretionary and fixed costs inflation and this next chart is a testament to our belief that this is a natural response to overall inflationary pressures that will normalize at some point in the future as things run hot, till they don’t:

Anyway let’s get to our outlook for a few of the markets we like to cover.

First up the SP500 futures. We hope you don’t mind our visual end of 2022 chart here, but we felt our maturity and our conscious is better suited to providing a “range of possibilities. The magenta line is the expected trajectory we would suspect given $90bln a month in bond buying, but since that is waning, we have chosen a flatter growth trajectory with our range of yearly high to low expected close from 4625 worst case scenario to 5200 best case scenario and a base case of 5050 +6.1% for the year:

Moving onto the Nasdaq futures they too will be in a flatter trajectory from their longer term trend based upon the ideas we have discussed prior and our best case scenario for the end of 2022 is 21000 and worst case 16700 with an expected base case at 18600 +13.9%. Technology will continue to be the safe haven and the Fed may push the pedal too much and if it does the discount may lead Nasdaq down to that 12000 area which would gladly be scooped up by any available and willing levered hedge fund and long term player, who knows the spigot will be reopened at some point again in the future:

As far US Government 10 Year yields, we will expect some players to buy into the rate hike thesis and these flows will no doubt push yields higher and to their upward bound limit where we suspect resides up near 1.80%. The federal reserve would then unleash damage control rhetoric and Yield Curve Control mechanisms which will promptly lead to a reversal back down in yields. We don’t expect yields to go to far in either case 30bps risk to the upside and 25 basis points to the downside, with a relative flat base case profile to end the year at 1.47% -4.4bp:

Our next chart will be Bitcoin. We suspect the digital currency sector will follow equities especially if we see a risk off event as money always sells whatever is most available when it needs to raise cash. Bitcoin is no exception, yet those weak hands always fall into stronger more long term HODLERs and that is what drives the next pricing expansion. If we can get a decent risk off event, not the futile China government fluff about banning Bitcoin, but a real global risk off event, we suspect $28900 to be the absolute line in the Bitcoin sand where many whales would love to back the truck up for the long haul. That price would be a decadal gift to many and we would suspect a massive candle bottom from there to lead the next real expansion upward toward $100k. Our best case end of 2022 would be just short of that level at $98500, our worst case low would be that $28900 area, but we do not expect worst case settle there. Our base case rests at $73000 +58%:

Finally we wanted to touch upon Tesla where the $900 gap has led to a massive no doubt option related run up to our all important fib level 0.786 with a price of $1167. This is a terrible long location and please do not follow the crowd here. We suspect at some point this year to offer us a decent discount to pick this back up in the $800-900 area with much less expected volatility at that point:

Alright, we hope you enjoyed this note and we hope you realize we live in a very chaotic world by which the only thing we can do is parameterize the very nature of things. The systems by which we reside in stay stable for periods of time, but we all know those periods release to periods of volatility and we cannot accurately predict nor discount fully the veracity of such things, but we can at least set some limits so that we can at least be cognizant when the time does indeed show up. Good luck traders and investors, here is to a happy, healthy and successful 2022!

Please think about joining the ranks that subscribe and get our thought process when we see things that are relevant, that matter and not just the BS fluff you get everywhere else. Your support is greatly appreciated. We write about the equivalent of one book a year on this site and the volumes we speak should transcend a lot further than these pages. You should be able to implement a lot of this into your game plan not just in trading, but in all walks of your life. We are in this together whether you believe that or not, it doesn’t matter, we are all connected, so stay positive and know your atoms do have an effect on everyone else around you, so STAY CALM and SIGN UP TODAY!

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Econemotions covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed. ALL RIGHTS RESERVED 2022