30YR Auction Ugly Tail

Bond Auction Tail Tutorial via an Arb

Magnelibra Econemotions subscribers, we made this a free to everyone post because we feel it’s that important of a lesson for our readership. We hope you share this to gain us exposure and we ultimately hope you become a paying sub and support our work we do here.

We remember the auction days, it was one of our favorite days as a 30yr arb, bidding for bonds into the auction and selling futures to hedge, when the big tail hit, damn it was free free money! (well most of the time at least)! Today the 30Y auction saw a whopping 2.4 basis point tail. Without getting into Dv01s and to make this easier from an informative point of view lets just look at what the tail meant to prices.

The tail is the difference between the average price paid in the auction and the lowest price paid in the auction, however in the case of US Treasury auctions they are “Dutch” style meaning everyone pays the same price. So as a trader and as a bond arbitrage where we spent the majority of our career, we would look at the “When Issued” (WI) yield which is the yield of the soon to be auctioned bond and compare it to the auction award level when it is released.

In today’s case we saw the WI trading at 1.382% at noon auction time and when the auction results came out the award was priced at 1.406%, this resulted in a 2.4 basis point tail.

So what does this all mean for the bonds and in particular bond prices?

If we look at the On The Run (OTR) and use the 1.382% yield the price of the bond is $96.25 and if we compare that to the award yield of 1.406% the on the run price would have to adjust down or fall in price in order to match that yield. So when we reprice the bond for the auction results the new OTR price is $96.07 or a reduction in the price of the bond cash by 18/32nds. In US Dollar terms this equates to [18 x $312.50] or $5,625 per every $1M in US Treasury Bonds.

So as a bond Arb depending how many million you bid for pre-auction and how many hedges you decided to put on (which is the real skill) a 2.4bp tail would have a significant impact and would most likely result in a stellar long basis position that could be immediately be realized and swapped out completely for a risk free profit.

Ahh, The good old days before FINRA’s Rule 42.10 which changed the liquidity and capital requirements under the guise of “protecting liquidity and integrity” of the US Treasury Bond Market. From our expert opinion all that rule did was systematically remove more speculators and concentrated the game into a very few large players hands, which was the obvious true intent, because removing access doesn’t jive with the liquidity theme now does it?

Anyway here are the rest of the results from today’s $26Bn 30Y US Treasury Bond Auction:

Bid to Cover was a paltry 2.136 down from 2.50 (the lowest since July 2019 and one of the lowest on record! Can you blame the investors??? I think not)

In-directs plunging from 72% to 59.8%, significantly below the 66.2% six-auction avg.

Directs taking down just 11.9%, it left Dealers holding a whopping 28.3% of the sale, the most since July 2019

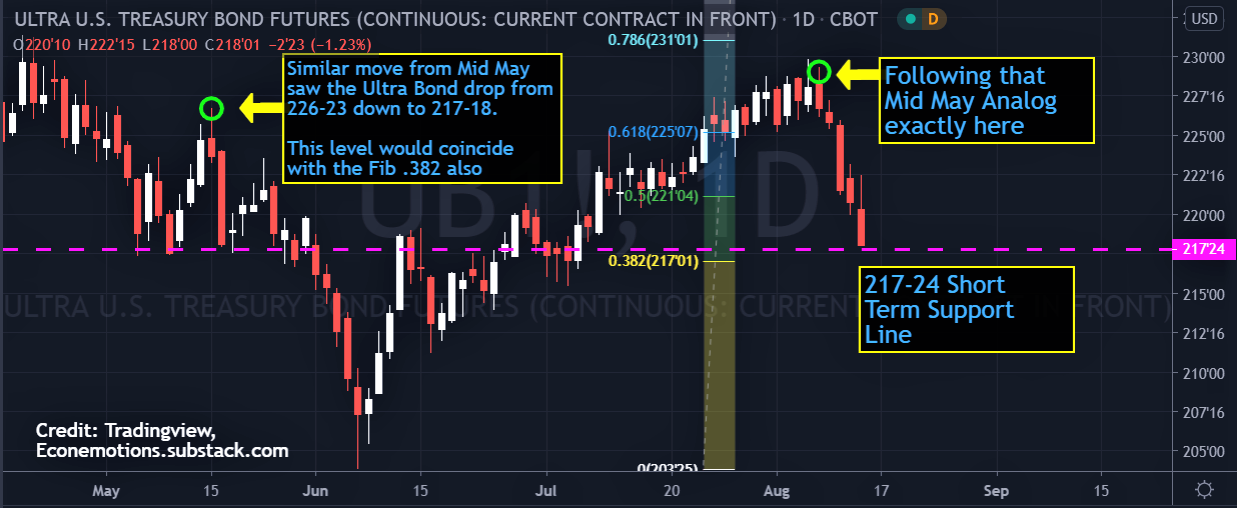

Magnelibra has been warning about the analog of the Ultra-Bond to our subscribers since that top reversal move on the 7th where we first posited the analog to that mid May move and take a look at the chart now:

That is it for now, we do think this current yields spike will eventually put downward pressure on the equities, which will only lead to further FED stimulus and POTUS action to alleviate any equity weakness. We all know the tolerance level for any such adverse equity move is scant at best. Anyway, hope you got something out of today’s note, stay versatile, stay nimble and realize the markets will have their way whether you like it or not!

If you aren’t currently a paying subscriber and would like access to our daily settlements page which our regular subscriber base gets or if you want to become a full Founding Member and have access to Magnelibra’s Global Futures Benchmark Program Positions Tracker. (Which is a truly unique global macro program that is a proxy to the systematic approach Magnelibra Capital Advisors the Commodity Trading Advisor uses for its individually managed accounts). Feel free to hit the subscribe button and or share our work below.

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.