Another Brick In The Wall

“We don’t need no education, we don’t need no thought control” (Another Brick in The Wall -Pink Floyd 1979)

As most of our longtime readers know, we love the analogies that movies and music paint. We understand that these medias are mere extensions of the artists thoughts and artistic creativity. We believe that the field of economics exhibits more attributes to art than science. Artificial Intelligence, metadata, the new great buzzwords of our time are nothing more than an extension of this insatiable human desire to retrofit chaos into order.

We aren’t calling AI out for being a fraud, but rather that the AI itself is nothing more than an extension of one programmers idea, an artist interpretation if you will. There is no doubt that AI and the construct of analyzing and decoding massive amounts of data at lightning speed has a profound effect upon our markets today. This is why we cannot discard them as outliers, but rather understand that they are becoming an ever-increasing driver of our global financial markets. With that said we must also understand that we cannot become so blinded by technology that we fail to realize chaos is dynamic and it adjusts according to every stimulus no matter where it is coming from AI or Human. The dependence on technology has become pervasive and frankly rather misunderstood and certainly overly miscalculated in terms of quantifying real market risk.

We wrote a piece a few weeks back entitled The Vol Monster Strikes Again, which outlines perfectly how risk can never truly be accounted for on all fronts. There are simply too many variables and of course no shortage of willing takers of the koolaid, or those thinking their positions are verified, quantified and immune to high bouts of volatility. The markets which are driven by AI and HFT have to account for the decreased potentiality of available exits. We are dumbfounded by large players ineptitude to quantify the single known fact that increased volatility begets increased volatility and in such a realm bids and offers become virtually nonexistent. This means your exit parameters are not what you thought and thus your risk is further extended out the standard deviation curve.

We have now read stories how FCMs were caught and accounts went debit and obviously the FCMs are liable. What we don’t understand is where exactly in the “risk” chain of command did things fail. The regulators need to take a much tighter look at certain leveraged products and ask whether or not they are what they say they are. Needless to say, we expect class action suits to ensue, so it will be interesting.

The reason we used the Pink Floyd quote this week is there is this seemingly massive, divide in the collective conscious of where the global economies are truly at. What seems to be happening is that the global economy is split even wider in terms of Wall Street vs Main Street. We can disregard DoddFrank and all its regulatory over reach. We can disregard the shill known as Liz Warren and the consumer protection safety board or whatever the waste of time that is or was. The reality is we don’t need any further authoritarian education and we certainly don’t need any further thought control. One look at the disastrous main stream media and you can see this divisiveness clearly.

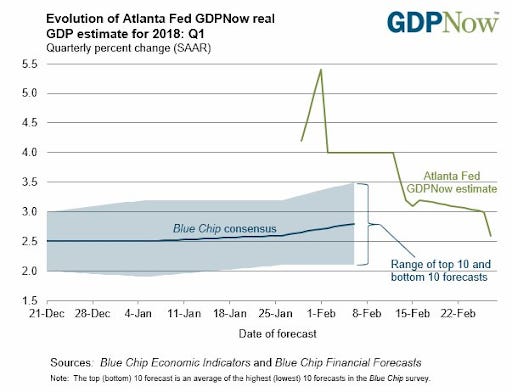

It is in this negative polarity that we need to rid our thought process in order to clarify and dig deeper into what is truly going on. We can’t simply rely upon some data driven AI to tell us what we actually see what we actually feel, we know what that is, but its interpretation is being suppressed. We need to seek out sources like this letter that have decidedly chosen to open your eyes and cut through all the BS that exists. Your investing future depends upon clean data that can be used to make intelligent decisions. We cannot rely on the likes of central bankers to give us data to interpret because they have one goal and that goal is to paint a picture of perpetual stable growth. As much as we adore their perpetual positivity, as traders and investors that’s all great, but unfortunately, we don’t have printing presses and we are subjected to the laws of economics, solvency and risk. One clear example of the Feds inabilities is the recent reduction in the Atlanta Feds GDPNow forecast model. We laughed when we saw this last month and the guys at the Chicago Economic Summit quoted it stating this clear hopium induced plus 5% GDP call. Well here is the latest updated chart:

So, in no time at all the GDP forecast is now 2.6%, a 100% reduction! As much as we laughed, we didn’t think less than one month later they would cut this thing in half. Now we certainly don’t need any more cannon fodder for the FEDs terrible prognostication skills, but this is just flat out absurdity. You would think and if it’s not apparent by now that paying 700 PHD economists is absolutely worthless than there is no changing your mindset. We were enlightened long ago and each year that goes by the central bank modus operandi becomes increasingly questionable.

This week saw new Fed head Jerome Powell take the helm at his first congressional testimony, as much as we abhor these theatrics, if this first one is any indication of what’s to come, God help us. Boring is an understatement and maybe it’s just his first time, maybe he will add color to his comments, but for now, sticking to the script was rather too obvious. Nothing ventured, nothing gained and status quo is certainly once again the utmost priority. So, we didn’t really learn anything new, the Fed will stay its hawkish course of 3 expected hikes and of course will be strictly “data dependent.” He did site high valuations and increasing leverage, gee thanks.

So, what does this all mean for the markets, what can we transcribe from the first two months of the year. First of all, the SP500 has seen volatility finally increase and a battle is being waged between monetary and fiscal policy, with abundant supply of equity induced buy backs. Let’s not even talk about the other part of the balance sheet known as debt, as we have been accustomed, that simply doesn’t matter anymore! (yea right!)

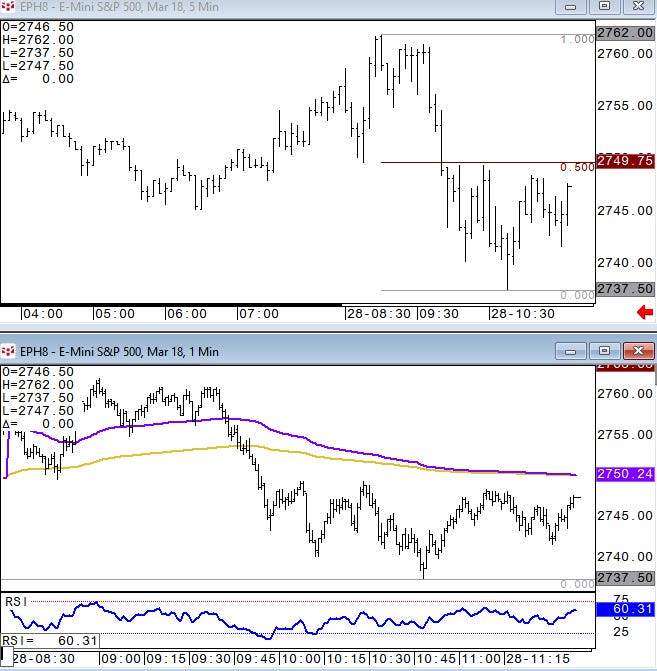

Anyway, after a nice January up move February opened up with the Vol shock and the markets saw its first 5% decline in years! Well overdue, but certainly welcomed by some fundamentalists, but who wants to rain on the equity up parade right? A big thanks to Keystone charts for setting up the following tech analysis and sending us this chart today. We tend to think that the 2750 level is a big deal and below 2700 will open more downside:

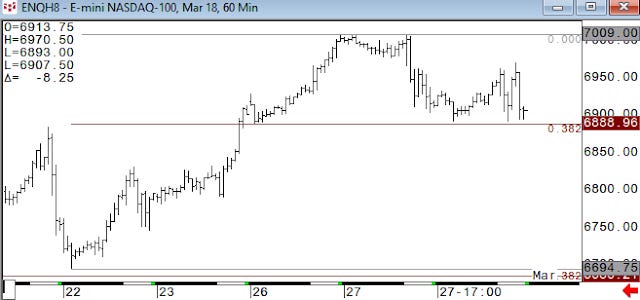

Keystone charts sent us this late in the day as the NASDAQ is nearing the all-important 6888 level in the Mar Future:

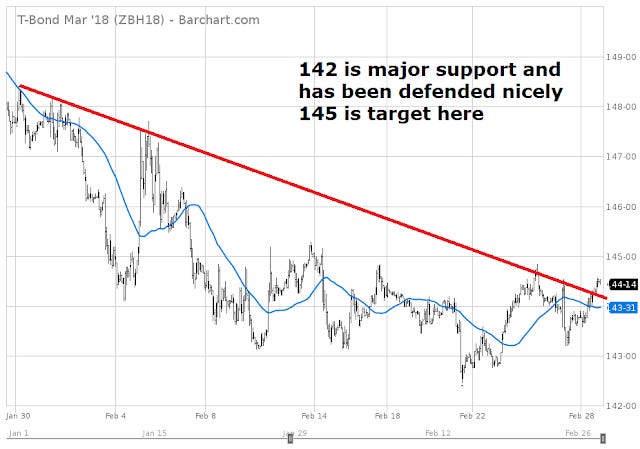

As for the bond market, it seems as if the long end is in a sideways wait and see mode here, it’s like they don’t know if they are a safe haven anymore, if they are wagging the equity tail or not or if they are simply in no man’s land. We would think many investors will use this rise in yields to lock in some long-term liability matches, anyway here is the bond futures chart:

Here is the Ten-Year futures chart which has carved out a nice trading range over the last few weeks:

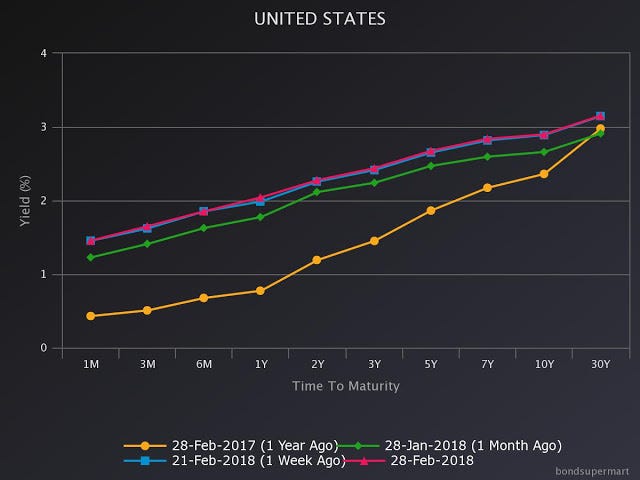

When we look at the US yield curve overall and compared to last year, it really gives you a sense of how far or how high short rates have come, while the long end seems to be anchored near that 3% level:

Getting a bit more granular we can see the 2s10 US Treasury yield curve spread has perhaps put in the range for 2018:

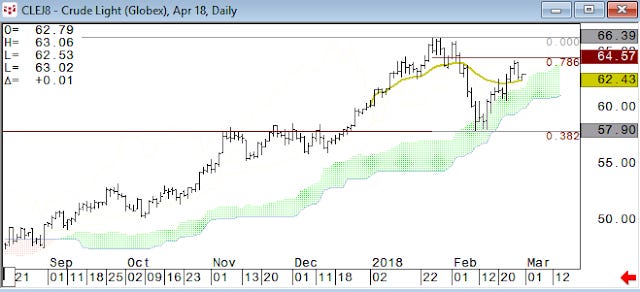

Looking at other markets we see Crude has support and resistance at $58 and $66 respectively, a break of $58 would open some deeper probes toward $50:

All the Fed hawkishness has led to some selling in the gold complex, although we would better suspect the selling is coming from leveraged positions that have either needed to lighten up the load or forced to sell in order to cover some other asset. Either way some technical probes have ensued down toward $1308 area:

Finally, we look at the dollar index which has had an anemic bounce at best off of the lows and faces stiff resistance at the 90-67 level:

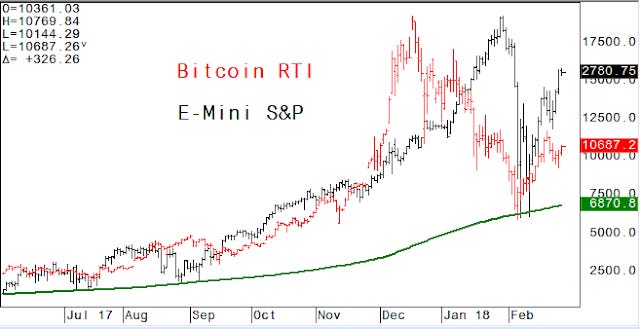

Something we covered in this week’s Crypto Corner newsletter but will display here is the increasing correlation of Bitcoin and the SP500. We caught a lot of flak on Twitter and Linkedin for even suggesting such a sacrilege but hey we have seen some increase talk of it this week, so we as always are ahead of the pack, here our two charts:

And the 90day rolling correlation which we present to display that the positive skew is rising and that this is certainly worthy of a look:

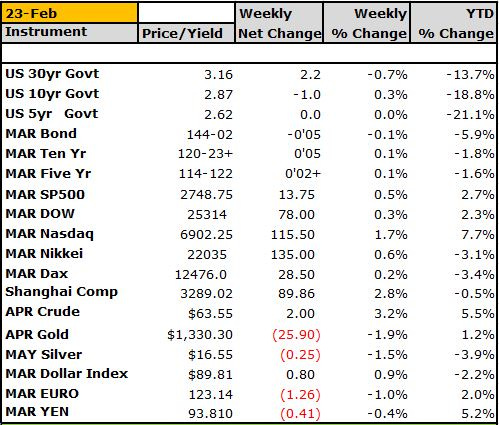

In conclusion we leave you with the weekly settlement prices of the markets that we mostly cover. Crude and Yen up near 5% YTD while the NASDAQ is once again the early standout up 7% riding the heels of all this technology, will it last? Is this time truly different? Only time will tell but we hope you enjoy the ride and that you stay abreast of all developing situations as we bring you analysis that you won’t get anywhere else, cheers!

DISCLAIMER: For Educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures nor an endorsement for the purchase and sale of ICOs or Cryptocurrency and should not be construed as such. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Mike Agne of Agne Asset Management LLC (AAM) and owner of www.econemotions.com and The CryptoCorner Newsletter, that you will profit or that losses can or will be limited in any manner whatsoever. The CryptoCorner logo and name is the sole right and property of (AAM). Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, (AAM) makes no warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed. DO NOT COPY OR FORWARD INTELLECTUAL PROPERTY WITHOUT PRIOR WRITTEN CONSENT AND OR APPROVAL.