Another Day Another NQ Outperformance

Well, we had a slew of FRB speakers today and we aren’t going to go into their jargon as we don’t take anything they say seriously, its all doublespeak. One talks a bit dovish, the next hawkish all in all, we know the truth, Fed Funds is 5% to 5.25%, inflation is still > 4% and the FRB will continue to stick with the “higher for longer” motto.

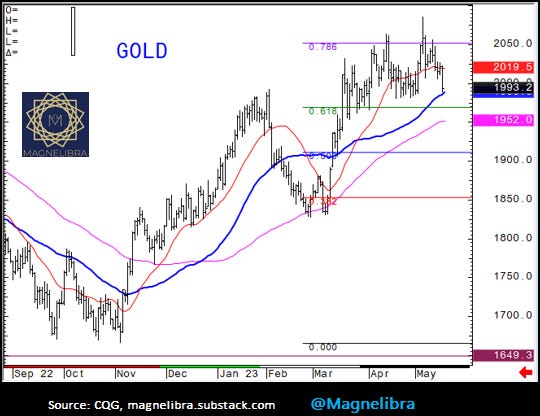

In any case we are beginning to see the Metals markets breakdown and the usual stalwart Gold contract wasn’t immune today, June Gold was down $29.70 today to settle at $1993. The target/reversal level has been confirmed and we should see continued pressure in the complex:

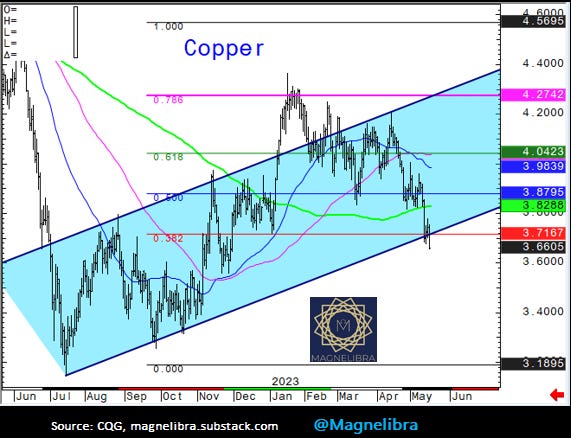

It hit the 50 Vwap on the head and held for now. However Copper has had other ideas. Obviously the great China recovery has been a dud and this solidifies this fact as we are now breaking out of a very long year long trend channel which may see a rush to discover just exactly how far and how deep we can probe those 2022 lows:

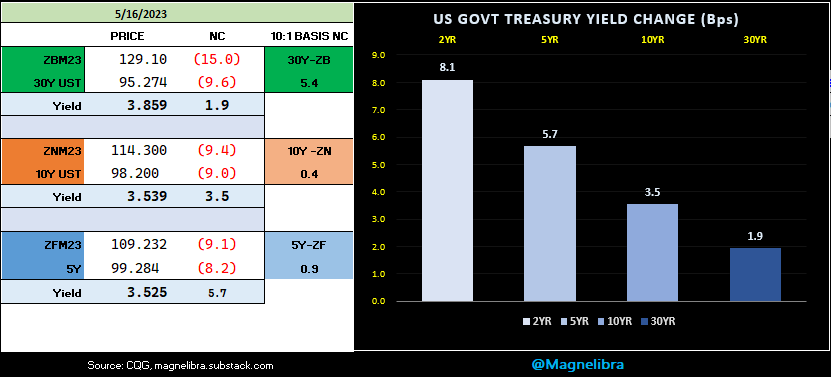

In the US bond market today, we saw retail sales stronger but a lot of it was inflation priced thus not necessarily more activity just higher prices paid per unit. However the Bond market after holding onto gains overnight, post Retail Sales continued to lose ground and the US yield curve was hit as the 2Y gained 8.1bp on the day:

As far as the equity indexes, once again our MEGACAP Nasdaq was the star performer on the day as it closed the day +15.25 at 13483.25 while the SP500 and the R2k lost 27.00 and 26.60 respectively. Its almost comical the flight to quality now so obvious in the tech. The first tell we had months ago was the fact that Apple issued a 30Y Bond with a coupon of 2.875% meanwhile the Feb 2053 30Y US Treasury came with a 3.625% coupon…

With this in mind, can the US Treasury yield higher than certain Corp. debt and still be considered the “risk free rate?” It seems some investors do not think so and we are beginning to believe that as well. This is a major structural change and has major upheaval type implications, but it all lends credence to our thesis that the US dollars time is waning and maybe waning faster than many could possibly conceive.

You know the Pound Sterling was the worlds reserve currency, until it wasn’t and there is no doubt the US dollar will suffer the same fate. Anyway if this is indeed true, than you can figure many insurers, pension funds, investors are going to have to rebalance, retool and rethink what is considered a safe comparable return…

As far as the technical picture the SP500 continues to sit at the top of the range but the longer it does so, the more power the bears have here to push downward:

We know its a weaker link than the Nasdaq, but the Nasdaq itself is showing a clear divergence in the strength and breadth of this up move and its support is not broad based. We aren’t sure what the catalyst will be, but something has to give here, either the Nasdaq takes a break and consolidates, or it drags the rest of the market higher with it, time will tell, but technically this doesn’t look that appealing right now:

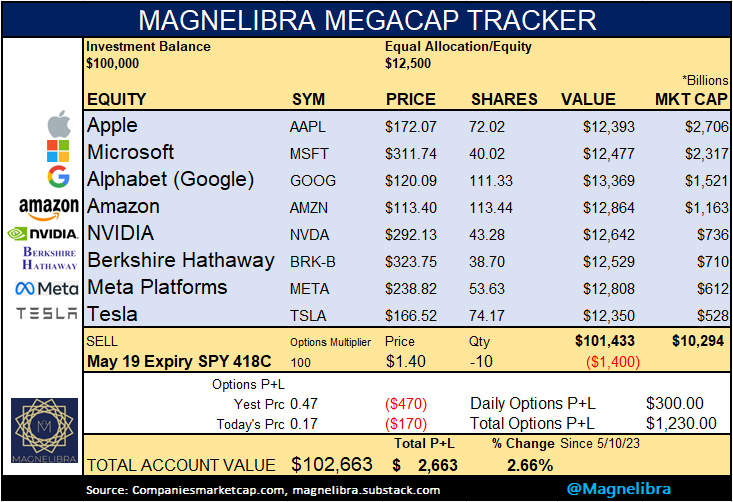

However we know the MEGACAP Tracker is still performing so until that changes, our sentiment for this consolidation in AI Tech boom will continue:

The options hedge is adding a nice premium as the SP500 is weak and the Nasdaq Megas continue to shine!

Ok till next time!

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023