Bank Earnings and Market Snapshot

Earnings (data from MarketWatch.com)

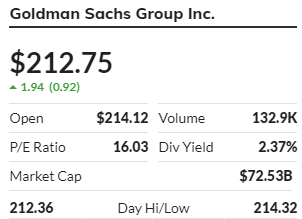

Goldman Sachs Group Inc. (GS) +1.9%

Net income nearly doubled to $3.48 billion, or $9.68 a share, from $1.79 billion, or $4.79 a share, in the year-ago period, beating the FactSet consensus of $5.54 a share.

Total revenue increased 29.5% to $10.78 billion, above the FactSet consensus of $9.38 billion, as annualized return on equity of 17.5% was the highest quarterly ROE since 2010.

Investment banking revenue rose 7% to $1.97 billion to beat expectations of $1.85 billion, while global markets revenue rose 29% to $4.55 billion.

Within global markets, equities revenue increased 10% to $2.05 billion to top expectations of $2.03 billion, while fixed income, currency and commodities (FICC) revenue grew 49% to $2.50 billion to beat expectations of $2.03 billion

Bank of America Corp. (BAC) -2.8% in premarket trading.

Net income fell to $4.9 billion, or 51 cents a share, from $5.8 billion, or 56 cents a share, in the year-ago period, above the FactSet consensus of 49 cents a share.

Total revenue declined 10.8% to $20.34 billion, missing the FactSet consensus of $20.8 billion, as the global markets, global banking and global wealth and investment management segments missed expectations while consumer banking topped forecasts.

Net interest income fell 16.9% to $10.13 billion, just shy of the FactSet consensus of $10.24 billion. Provision for credit losses increased to $1.39 billion from $779 million, but that was below expectations of $1.88 billion.

Wells Fargo & Co. (WFC), is -2.7% in premarket trading, the bank reported Q3 profit that was less than half what it was last year and was below expectations.

Net income fell to $1.72 billion, or 42 cents a share, from $4.04 billion, or 92 cents a share, in the year-ago period, to miss the FactSet consensus of 44 cents a share.

Total revenue dropped 14% to $18.86 billion, above the FactSet consensus of $17.99 billion.

Net interest income declined about 20% to $9.4 billion to miss expectations of $9.7 billion.

Net interest margin (NIM) fell to 2.13% from 2.66%, just below expectations of 2.19%. Provision for credit losses was $556 million, down from $608 million a year ago and down from $3.38 billion in the second quarter, while the FactSet consensus was $1.79 billion.

Pretty interesting the decline in NIM and this is one of those negative factors on low low rates and one by which spread compression in their product base will lead to tighter margins as consumers will jump ship to the lowest rate offers and competition from online non traditional financiers should continue to benefit.

Here is a quick snapshot of the futures this morning (Tradingview data)

BONDS:

EQUITIES:

FX:

METALS & ENERGY:

Finally, here are the QQQs and the QTFAANGMs this morning:

That’s it for now, good luck today traders and investors, we did see PPI this morning post a +0.4% expecting +0.2% so pretty significant. When you print as much money as the central banks have this year and you have supply side shutdown shocks, it shouldn’t come as too much of a surprise…

Please share our work and subscribe if you haven’t already, we have a free tier, a 2 latte a month style and a Founders which has access to our Global Futures Benchmark Program positions tracker daily. We hope you enjoy our work and we hope you continue to support us.

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.