Banking Woes Continue FRB to Raise 25bp

The KRE bank index coupled with the JOLTs and Factory orders today, sent the US bond market higher, which was a complete reversal of yesterday’s move. JOLTs dropped to 9.59M from 9.97M previously (we don’t believe there are this many openings btw) and Factory Orders came in at 0.9% expecting 1.3%. We also saw the continued slide in the US domestic banking sector as the KRE Bank Index which dropped another 6.27% today!

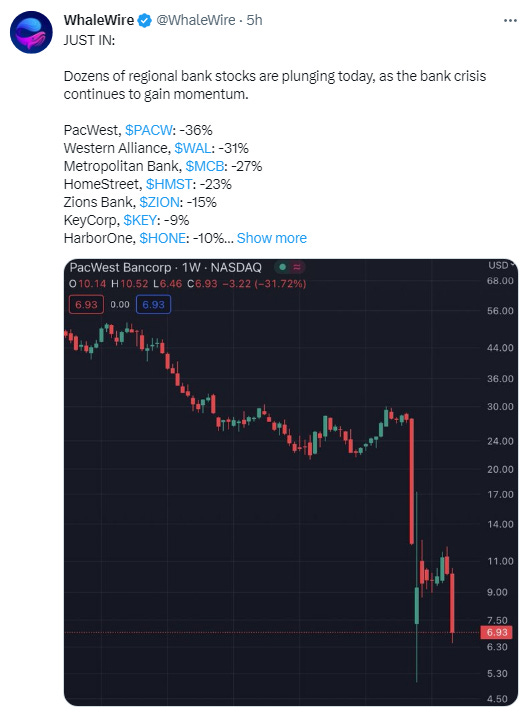

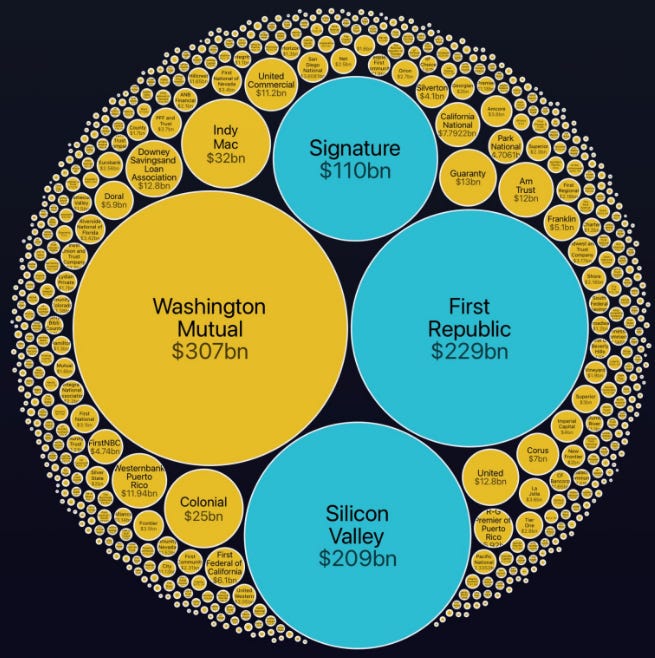

WhaleWire on twitter had this post up today showing the carnage:

We have been warning for a long time that all of these FRB created reserves and deposits would start exiting stage left from the low paying banking sector to Treasury Direct and MMMFunds. This indeed has been the case and we are also noticing money exiting the system entirely, probably going into Bitcoin or into mattresses. This is not the kind of action one wants to see with the FRB on tap to raise another 25bp and an already mega sized inverted 3M/10Y spread which once again is back out to record inversions of -172 basis points!

This type of negative carry is a balance sheet killer and if you are levered, in short term interest only debt, well you will be getting carted out feet first and defaults will rise, asset prices will plummet, fire sales will ensue and contagion will spread. All of this and we aren’t even in a recession yet. The bank sector is being exposed for the fallacy that it is, Deposits are LIABILITIES and banks are being scrutinized right now as they should. The fact that JPM Chase lowered their deposit interest rate to 0.01% is a testament to the arrogance, yet confirmation that they are indeed the FRBs defacto bad bank. Now they are getting a juicy $50Bn loan from the FDIC to smooth the FRepublic takeout, which from our standpoint, isn’t even legal. There is no precedent for the FDIC to loan a bank funds for this nor actual authority.

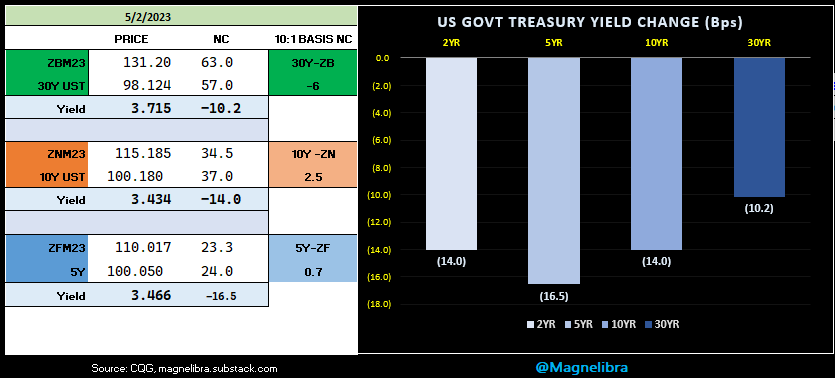

So we are playing it as it comes along, flying by the seat of our pants as it seems and the US bond market continues to punish the FRB and their short rate by cutting yields in the longer end down in size. Here is today’s action with the 5Y the big winner dropping 16.5bp:

The odds of a 25bp hike tomorrow out of the FRB stands at 90%. We know they don’t want to but they have to tow the line and with inflation still well above their target, there is no excuse, not even the regional banking crisis should deter them. There is still room to go before inflation comes even close and there is far too much speculative money still buying up properties to relent. This is and will always be about too much money, too much concentration of capital and the FRB has its work cut out for itself.

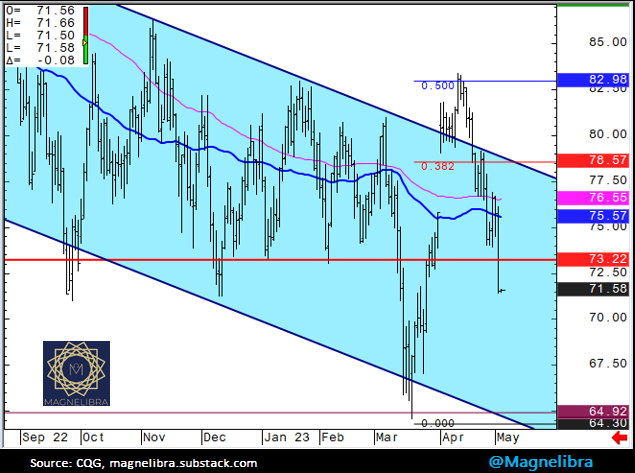

As far as equities today, they were hit on banking woes and continued weakness and worry out of that sector. The SP500 lost 49 ticks closing at 4136.75:

We like that the FRB is coming in at a time where this is right at the top of our trend channel. This trend channel has marked the sideways trade for nearly a year bouncing between 3700 and 4200.

As far as the Nasdaq we know Apple is the bigger deal this week, but it closed down 122.25 points today closing at 13184.50. We are still in the camp that the market is putting in a major top here and that Apple will be the catalyst for renewed selling pressure in the weeks to come. Above 13350 and maybe we negate this technical level, so that is our parameter for now:

June Crude Oil continues to work off that OPEC cut and the recessionary worry seems very evident in the complex:

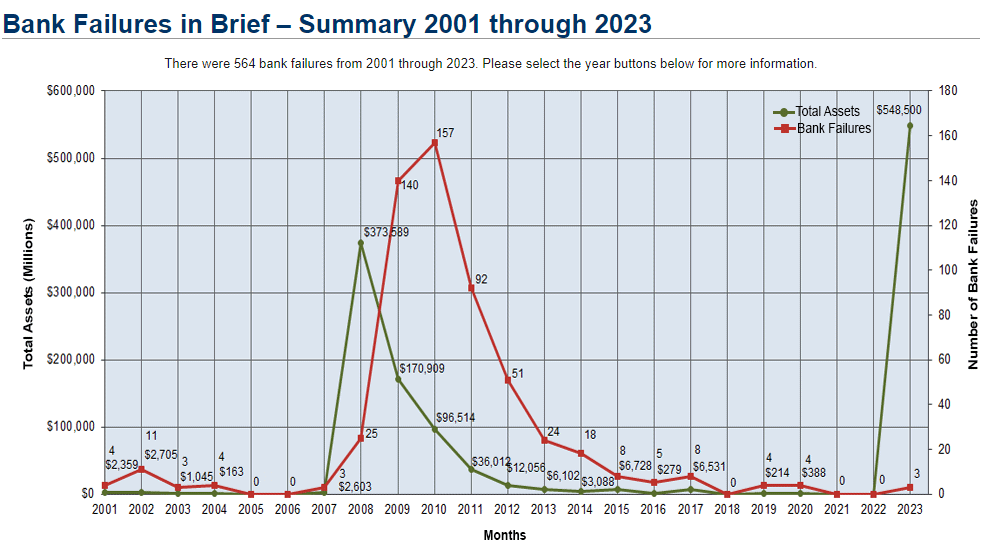

We want to drive home the fact that we have seen all of this before, we have seen the equity markets cheerfully, fully levered up call buying, VIX smashing enthusiasm to only give way to real market forces eventually. We want to solidify the fact that the economic backdrop is slowly deteriorating and like everything else that eventually breaks, it happens slowly then all of a sudden. We want you to be smart and cognizant and fact based in your decision making process. Look at this next chart and maybe you will begin to see that everything under the banking surface isn’t as rosy as Jaime Dimon wants to portray it:

And another graphic to put this all into perspective:

Maybe one day we will get a journalist to ask the FRB chair a real question, like,

Why is it necessary to grow the FRB balance sheet at a 12% annualized rate?

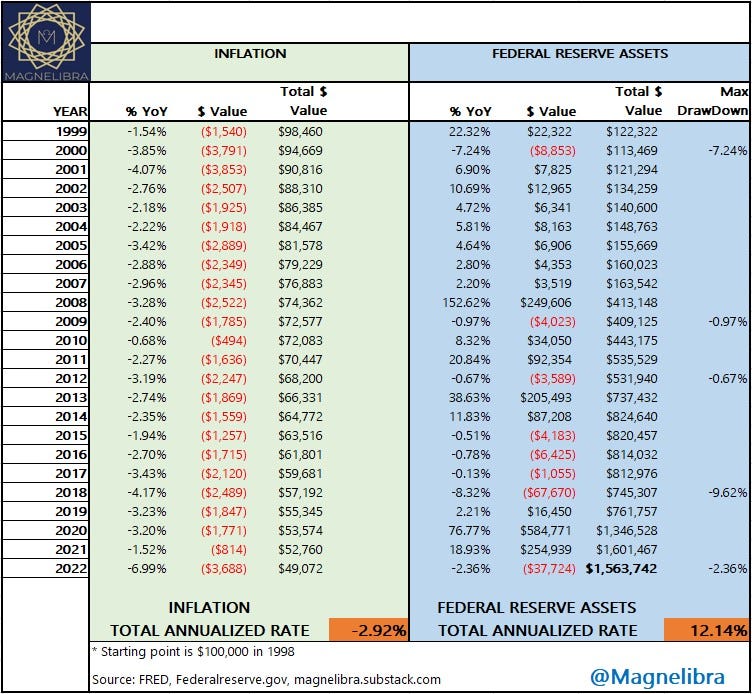

Not to mention inflation has never really been too far from 3%. This is one of our favorite graphics, so please share it if you can, it really drives home the point that nothing really matters, not earnings, not profits, nothing but being able to roll over debt, issue debt and have a central bank willing to expand their balance sheet ad infinitum:

This is absurdity at its finest, its the kind of absurdity that sways Capitalism to Socialism, or in the words of Karl Marx,

"The development of Modern Industry, therefore, cuts from under its feet the very foundation on which the bourgeoisie produces and appropriates products. What the bourgeoisie therefore produces, above all, are its own grave-diggers. Its fall and the victory of the proletariat are equally inevitable." - Karl Marx, The Communist Manifesto

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023