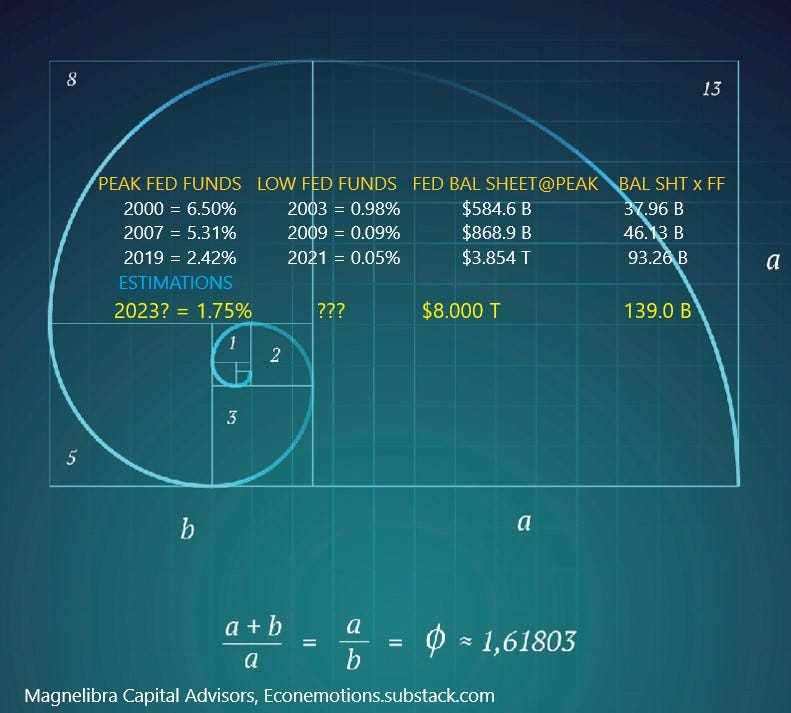

Base Case FED FUNDS

A fundamental exploration

So we know historically that the Federal Reserve cannot function independently of the US Treasury’s fiduciary function. The Federal Reserve is private for one very important reason, to act as the US Treasuries defacto supplier of its product. Yes its strange, but the US Treasury’s product is debt, the Federal Reserves responsibility is to print said debt. In return the FEDERAL RESERVE gets paid a dividend, less expenses of course.

This system of debt used to come with interest rates that actually signified some sort of risk free rate, a benchmark if you will. However once every entity from public governments to corporations went full tilt Modigliani/Miller Debt instead of equity, well interest rates would no longer be an appropriate measure of risk. Instead we have a pegged system by which interest rates are kept artificially low so that our government can borrow Trillions ad infinitum at ever decreasing longer term rates. Basically as the Federal Reserves balance sheet grows, interest rates have to operate inversely else said game of debt is over.

With all that said, we want you to know that as Austrian’s we do not believe in this system as the result is always the same, hyperinflation/deflation. This system will suffer that same fate, some day, but that is still to be determined. We do think that time is always drawing closer, however the US game is still the only game in town and until that changes, the cooperative/collective will stay play within its confines.

So with the FOMC about to raise 50bp (We think they should have gone 50bp the last time) at least the FED is doing the right thing…finally. We do believe that they will do this again at the next meeting and get Fed Funds to 1.25% then slow walk this with a wait and see mode A simple algo would be

if SP500 is negative then walk slow, if positive then go gradual. In a nut shell its drop two 50bp bombs then play the waiting game.

We estimate that by 2023 they will get Fed Funds to 1.75bp based upon our call for a reduction in the FED balance sheet to $8T and consistent with their historical pattern. Anyway here is the data from the last 20 years in regards to Fed Funds peak to trough:

The Federal Reserve cannot afford to be too aggressive given the current economic starting point. Its their own fault, they should have raised rates in Q3 2021 but they dropped the ball. Now its catch up time and not an envious position by any means.

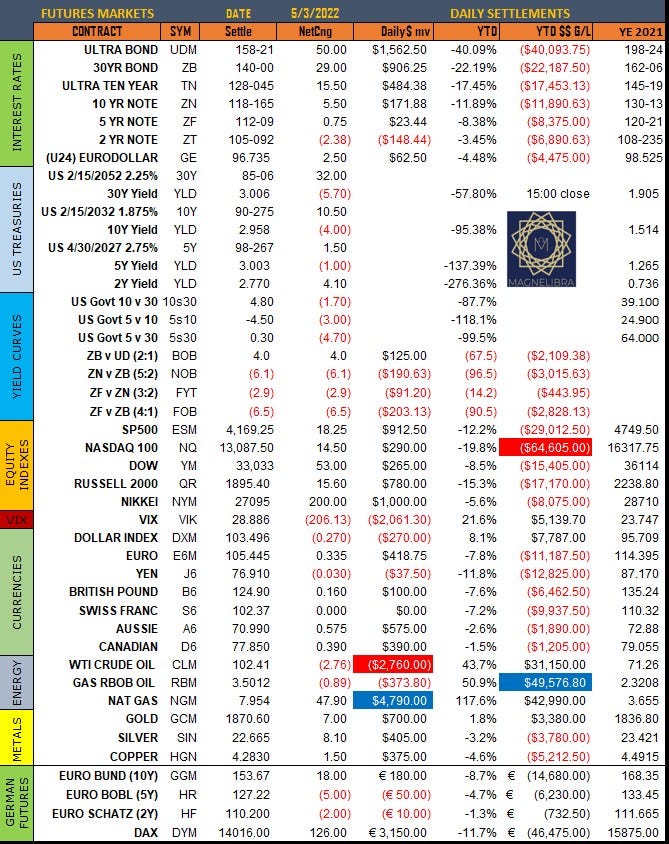

Here are today’s settles:

Bitcoin has major support at $36800 and we can only assume if equities bottom, so to will Bitcoin and Ethereum.

Alright readers, that’s it for today, keep your eyes, ears and hands upon the wheel and understand that markets are chaotic and navigating them takes an awful lot of precise angles and definitive execution, we hope our info helps. Remember if you aren’t going to subscribe at least share our work with others!

Please think about joining the ranks who subscribe and support our mission here and if you can’t help monetarily then please at least share with one other person. When you read Econemotions trust that you will obtain a different thought process a different way to look at things while you are on your own journey. Your support is greatly appreciated and we have new tiers to support us, every little bit counts. You should be able to implement a lot of this into your game plan not just in trading, but in all walks of your life. We are in this together whether you believe that or not, it doesn’t matter, we are all connected, so stay positive and know your atoms do have an effect on everyone else around you, so STAY CALM and SIGN UP TODAY!

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Econemotions covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2022