Big Numbers Coming & QQQ dislocates from Big Tech Names

Citadel Driving pricing and efficiency

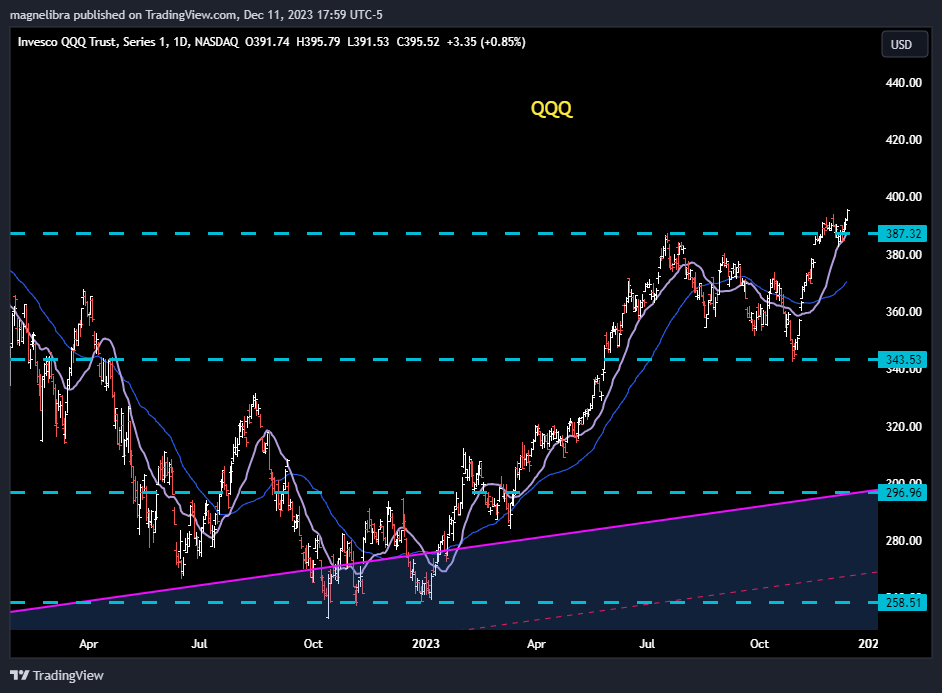

Alright so we have to digest a lot today, let’s first begin by taking a look at the QQQs today the tech heavy Invesco ETF which heavily weights the global tech companies. Well today we saw something we haven’t seen in quite some time, the MEGA8s as we like to call them were mostly down on the day, but the QQQ was +3.35 today above the 395 marker:

We like the continued run here and will not be dissuade from further upside as long as we are above 387. We saw many a confused posts on X today as to why QQQs were higher but the mainstay techs were not, how can this be?

Well we obviously know the answer and its a clear start of major diversification out of this concentrated risk of the MEGA8s to the broader markets, in fact this is why we cover the MEGA8s, so we can see the reversal of this trend.

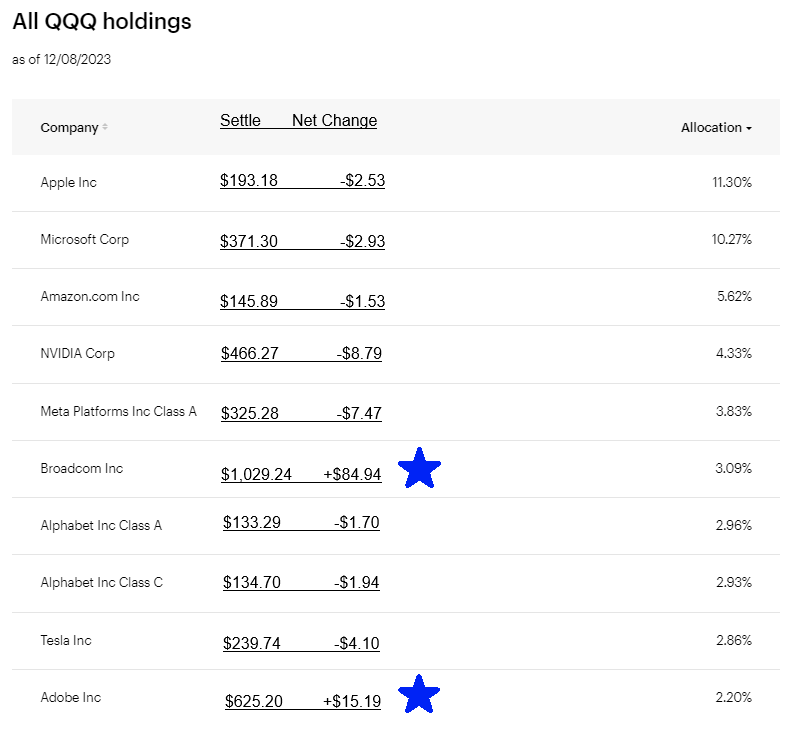

We aren’t saying the overall markets are going to move lower, but rather that major players have begun diversifying out of the main household tech names for the broader plays, such as Broadcom (AVGO) which is a major component of the Invesco QQQ ETF, it was up 9% today. Adobe Systems(ADBE) was also up big today and we show you the breakdown of the top holdings where Apple and Microsoft dominant the ETF making up over 11.5% of the ETF weightings:

So we weren’t confused about this rather its why you need to be informed because if you were trading the top names and buying because the QQQs were up then you were losing money! We do think its a bit comical that Ken Griffin of Citadel spoke last week how its firms like his that,

“Drive the value of companies toward where they think it should be valued.”

What he really meant is they position their book according to analysts prices and drive with momentum and balance sheet securities toward this specific value. In the case of Broadcom, Citi came out with a $1100 price target and thus we are certain Citadel algos were all over this creating a vacuum higher:

Griffin went on to say that passive investing “enjoys” the market efficiency that they create…what he means to say is that they have the technology and the balance sheet to price any security wherever they deem fit, and that my dear friends is power.

Griffin brings out some massive haters for this positioning, but in reality he is just being honest. We appreciate his honesty and its the economy of scale that he has ascertained that allows for them to enjoy this position, so we aren’t going to hate on that kind of power creation. We have always said the markets are not dependent upon economic principles or old investment metrics, rather today’s markets are all priced upon active manager positioning and balance sheet opportunities or constraints.

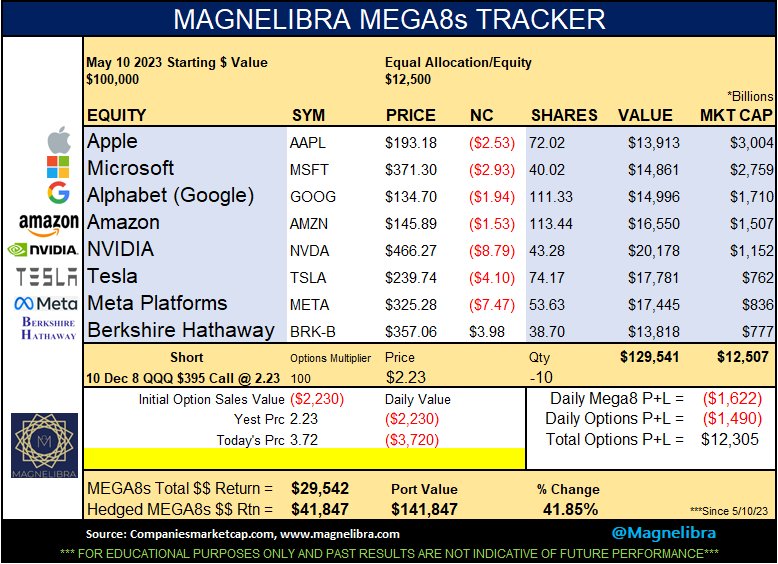

Ok so let’s take a look at todays MEGA8s tracker, our options hedge is on a short 2x leash for liquidation on a settlement, so we won’t let that hedge go to far a close above 4.5 and it will exit out of it:

The market cap of this group is still up an astounding $5T plus since May, truly an amazing run:

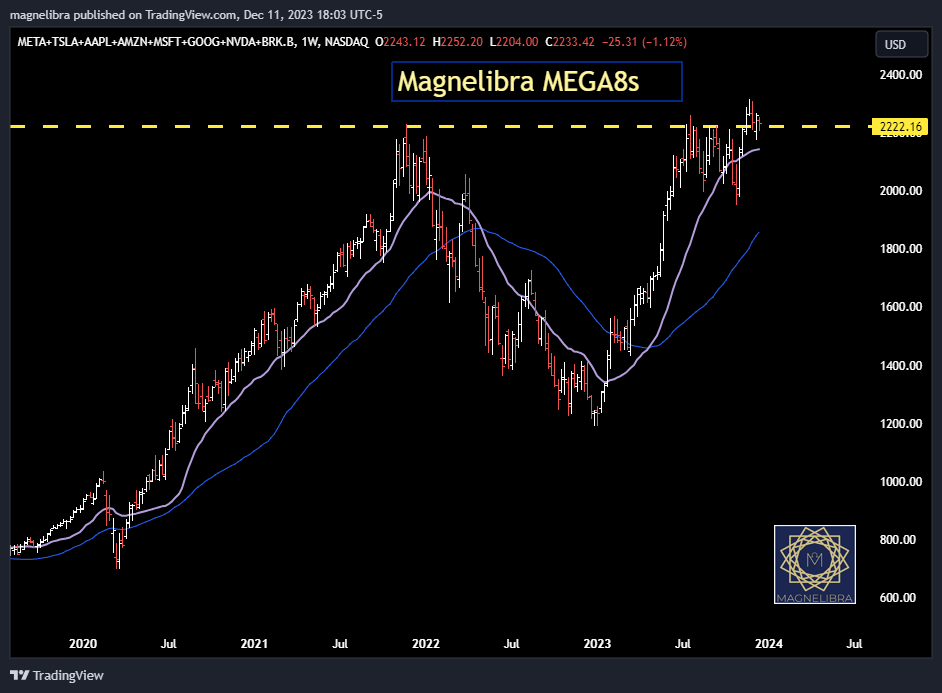

As far as the chart of this overall group we may get into a situation where the Nasdaq can move higher but this group stagnate and lose ground. Ultimately though we don’t view that as an overly bullish signal for the broader market, this is more of a position reallocation by some very large funds:

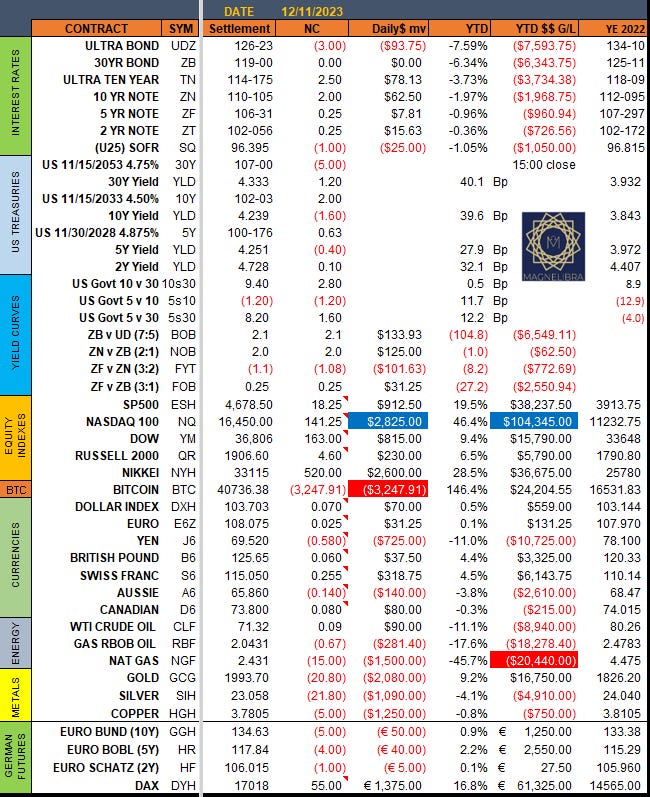

Let’s look at the settlements of the markets that Magnelibra follows below, please note we have rolled the equities and currencies now from December to March Futures. Bitcoin also showing some weakness today, nothing more than profit taking here in our opinion:

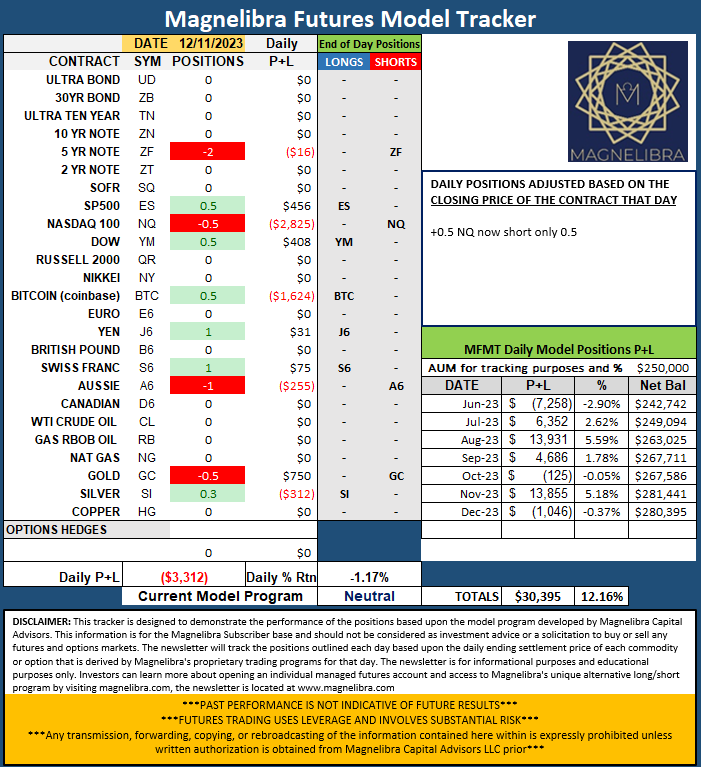

As far as our Futures Model Tracker, one change covering half the NQ short position here:

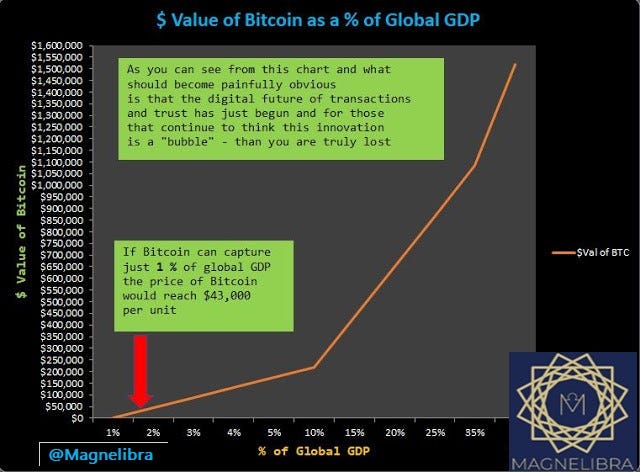

We also wanted to reshare our Bitcoin pricing model which we put out a few notes ago and first covered and shared in 2017. We feel its important that our readers stay well ahead of the game and informed that Bitcoin no matter what people say about it, is a TECHNOLOGY above all else and owning Bitcoin is an ownership stake in that technology:

Ok let’s move to some futures market technical charts, first up is the SP500 futures where we continue to plot the blue arrow path that we put out a few weeks ago. We suspected a massive run toward the highs as many firms play catch up to the outperformance of the indexes:

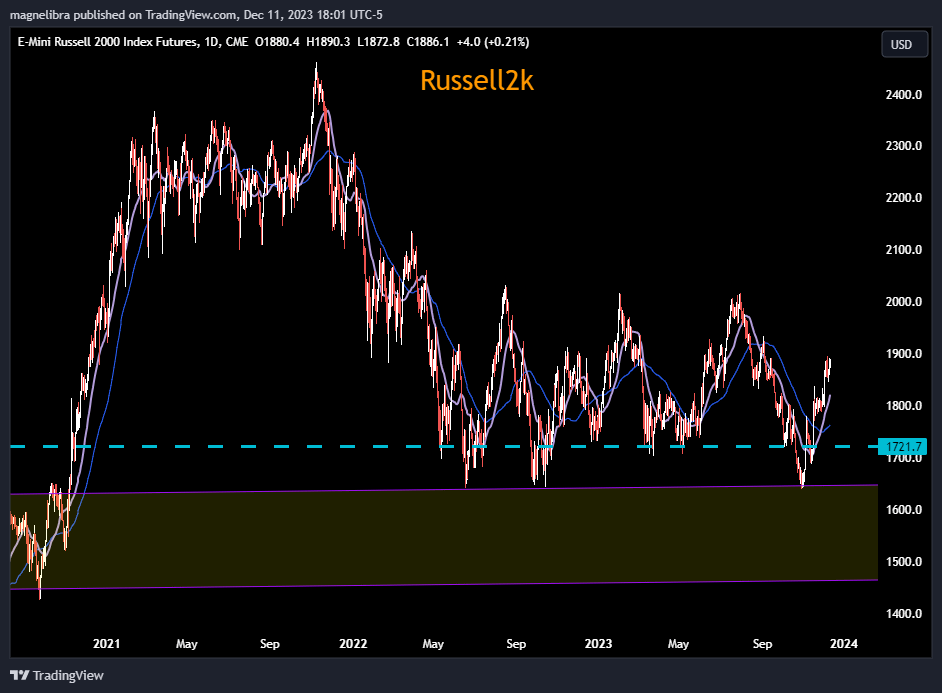

The Russell2k has made some presses upward, but greatly lag behind the Nasdaq and SP500:

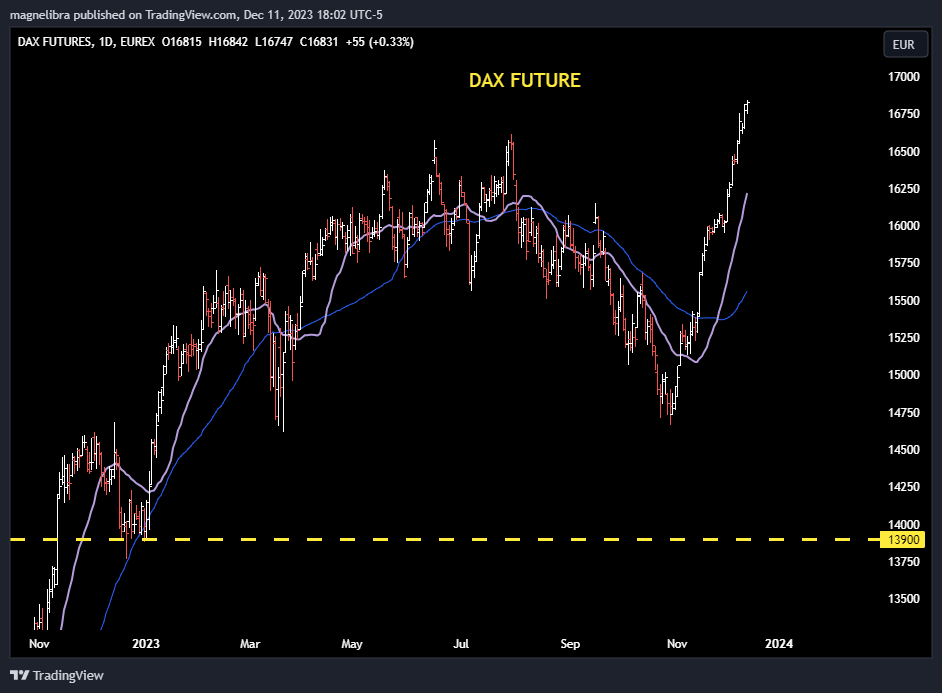

The DAX futures have come alive as well with a decent run into year end thus far erasing a 3 month slide in 1 month:

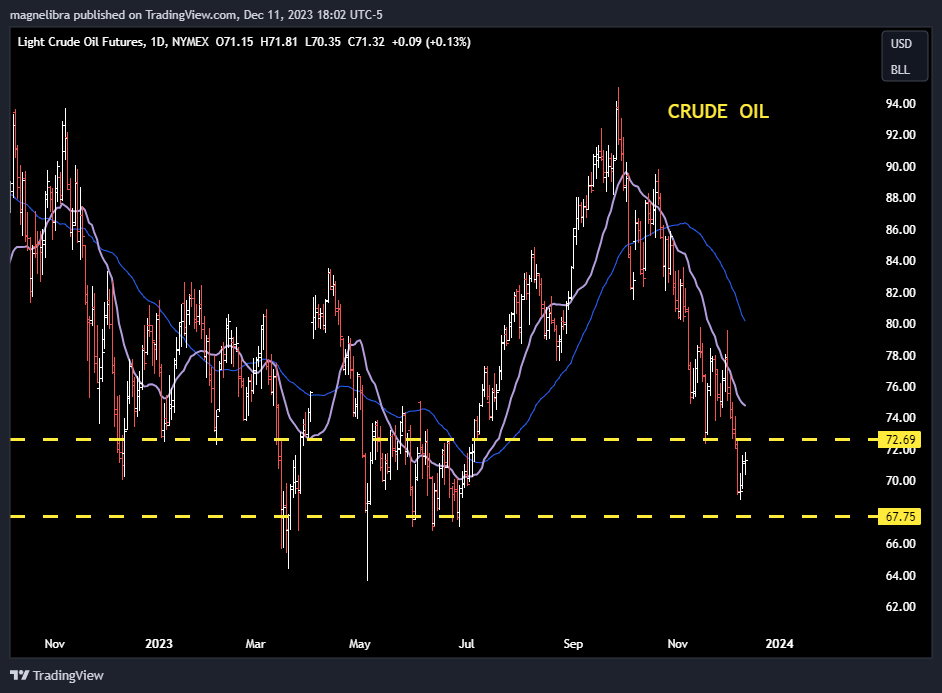

The Crude Oil market is trying to put in a bottom here at prior supports which should be expected here. The outlook for Crude is still negative given the overall future path for global economies next year:

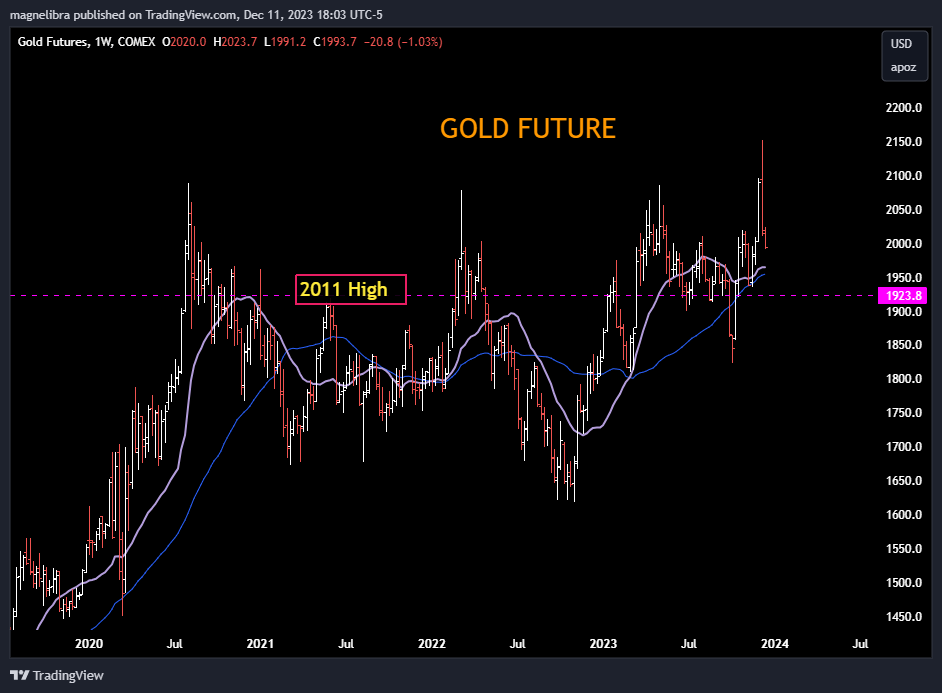

This is the same theme for Gold Futures where we suspect support will come in down at $1925 and that level should be a longer term buy area but a deeper probe below $1900 could signal some liquidity issues globally:

Alright, tomorrow is CPI, PPI and FOMC are Wednesday where the expected move is to keep the Federal Funds rate unchanged. We suspect Powell may signal that he is happy with the progression of the weaker inflation numbers, but will always be data dependent and not risk easing off the pedal of monetary tightening till their 2% level is hit.

We know China is slowing big time and they will export that deflation here, this is a them the US bond market has scene but we feel that inflation will not move too far down given the massive $3T plus still sitting in reserves. Reverse Repos are still $800b plus and providing a back stop of ample liquidity for the risk markets. We would suspect the FRB has a lot of work to do in regards to its balance sheet reduction, but as long time readers know, the only real tool the FRB has is QE.

We feel they can keep rates elevated and continue to reduce the balance sheet as long as non farm payrolls remain positive. If and only if that starts to print negative will we be comfortable with the long bonds, short equities thesis, until then its status quo march to higher highs and lows.

If you think our work has some validity and you want to explore your options in regards to diversifying your long only static portfolio, feel free to reach out to us. We can customize any portfolio’s risk level to your specific tolerances. Every portfolio should contain an ample amount of asymmetrical risk product to offset the basic long only longer term static style of investing. Yes equities and bonds are traditional long only investments and are a large portion of ones holdings, but we believe in alternative structures not only from a hedging perspective, but from a more broader opportunistic sense, whereby even a small 5 to 10% allocation to an alternative strategy could greatly enhance ones overall performance.

Please share our work with your associates or please think about supporting what we do here. We put a massive amount of time, effort and thought in formulating and interpreting this data so that you can remain informed. If you can’t share it or support it, a simple like will suffice! Cheers and we hope you all have a great evening.