Bond to Equity Correlations Continue Negative

This seems to be an ongoing theme here now as the reality of higher rates is setting in for major industries and businesses across the globe. Higher rates have eroded the free carry arbitrage that so many have stealthfully employed (think $80T in FX swaps unaccounted for generally). It has also eroded the leveraged players ability to factor up in hopes for continued asset price appreciation, hint, that ain’t happening any time soon. Now that higher rates are finally making their rounds throughout the global economies, not to mention a stronger dollar wreaking havoc on EMs, although now looks like the USD is cooling off a bit, the prospect of weaker asset prices moving forward should be the path of least resistance and that will most likely surprise many.

Anyway we continue to expect US yields to fall if equity prices continue to move lower (more negative correlation) as they are now becoming a necessary component, not only for balance sheet and liability matching as they always are, but more importantly a protector of wealth.

Many will be looking for return structures over the next decade that will not be provided by equities in this inflationary, higher rate environment, as well as a global central bank consortium that has already hijacked and brought forth earnings in the form of QE an monetary stimulus, probably some 2 decades worth in fact. So we will continue to pound the negative correlation theme and believe bonds are going to be much more in vogue than equities for some time here. Subscribers saw our 1972 to 1987 analog chart this week and we do believe that is a very real decade prognostication.

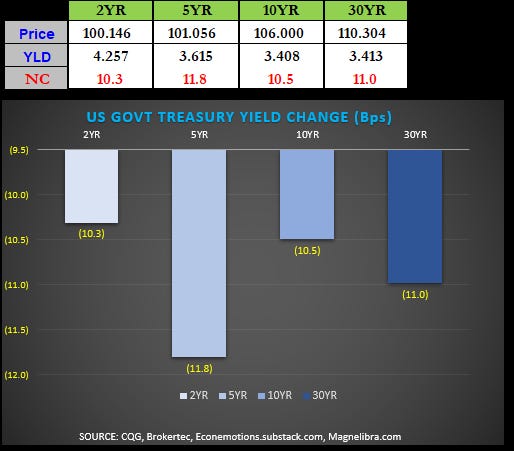

Today’s action saw yields parallel shift down, with the 5Y actually leading the way as it closed today via our 3pm Est. closing levels -11.8 bp:

The US Govt 10Y chart looks increasing bullish (price) as yields are now targeting a 3.22% area:

Consumer credit was posted this afternoon and we see a continued increase in consumer leverage as credit hit an all time high at $1.171T and the savings rate plunged to 17 year lows, increasing the weakness of the consumers balance sheet:

We know this band aid can last however the pain in regards to interest rate costs will erode future discretionary spending and when the recession comes, then the wave of defaults follow. This is basic business cycle stuff, its what QE and the global central banks try to mask, but in reality all they do is hijack future monetary growth and bring it forward, to be realized by the very few at the top!

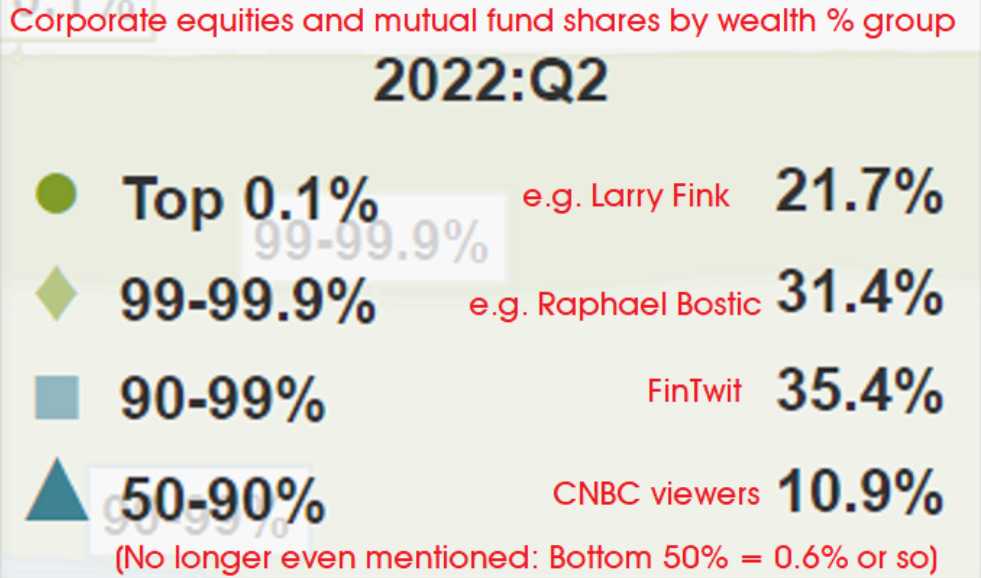

The top 10% of elites own 88.5% of all the equity wealth (Corp. Shares and Mutual Funds) the top 1% own 53.1%. So yea concentrating wealth is what QE does, period:

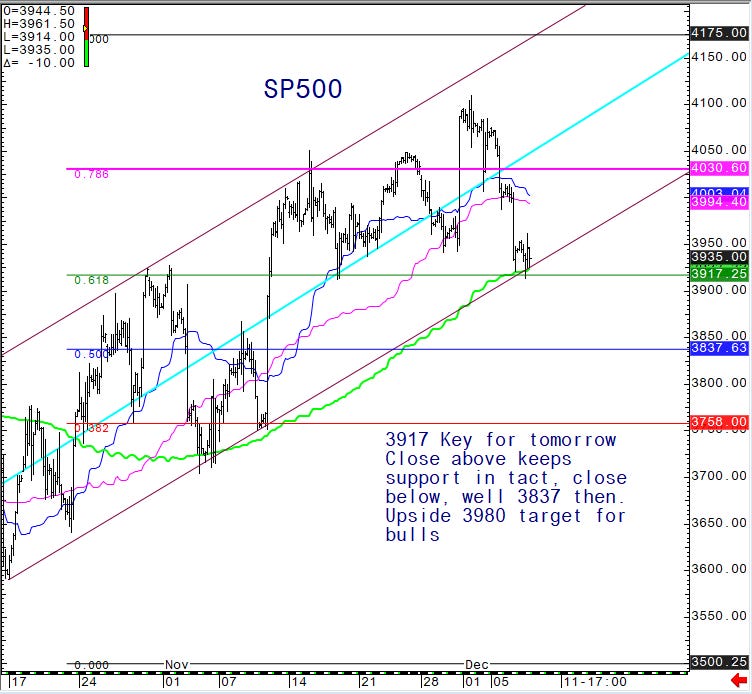

Alright as far as equity futures, 3917 in the Dec SP500 held its first test and we have bounced. However tomorrow is key and we would need a close above this again as well as Friday to keep any chance of higher prices in tact, if we close below, well straight to 3837:

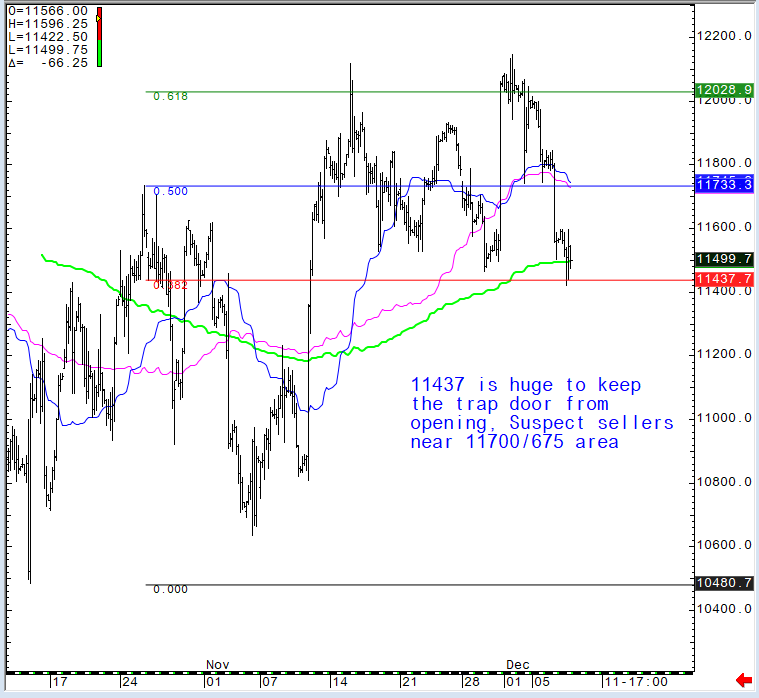

As far as the Dec Nasdaq, 11437 is huge and 11675/700 area will most likely see sellers again:

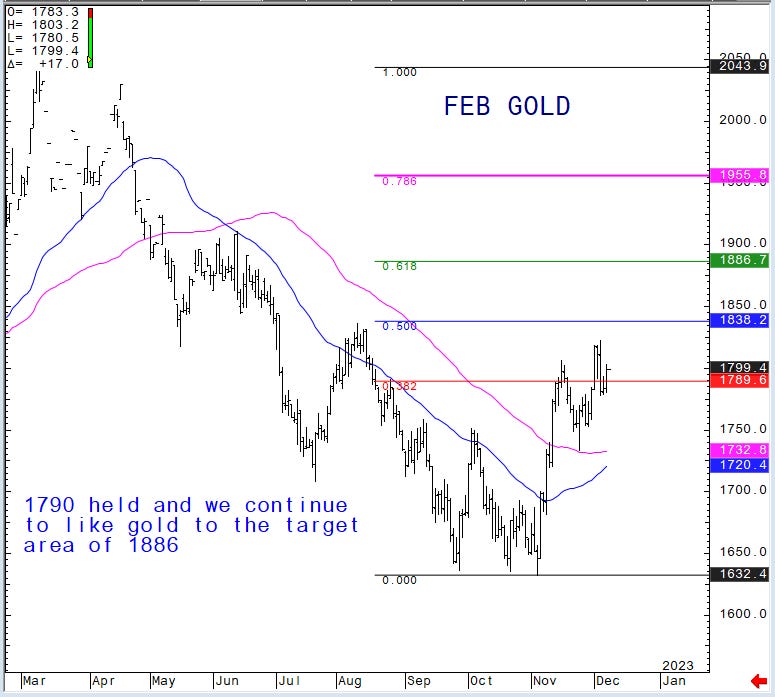

One last chart today, Feb Gold it has held that 1790 level and we like the fact that downward equity pressure is no longer correlating into lower gold prices. We also know China and the rest of the BRICs are hell bent on removing themselves from the Petrodollar and in fact, Zerohedge had an article out about that very topic today. We do believe this is a substantial threat to US Dollar Hegemony and one that we do not take lightly nor should you. This is a very big deal and it adds to the global geopolitical uncertainty moving forward. Anyway we like 1883 as our target here:

Ok that is it for now, good luck out there and we hope you continue to learn from our work, please like, share or subscribe, we believe we can add value to many in regards to retooling your thought processes in regards to our financial construct, but also increase your intuitiveness in regards to understanding how our system truly operates.

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Econemotions covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2022