China/US 90 Day Cool Off Period, Subscriber Data for May 9th

Risk On

Subscribers, here is the summary of this weekends tariff summit and what was announced per Zhedge:

The United States will remove the additional tariffs it imposed on China on April 8 and April 9, 2025, but will retain all duties imposed on China prior to April 2, 2025, including Section 301 tariffs, Section 232 tariffs, tariffs imposed in response to the fentanyl national emergency invoked pursuant to the International Emergency Economic Powers Act, and Most Favored Nation tariffs.

The United States will suspend its 34% reciprocal tariff imposed on April 2, 2025 for 90 days, but retain a 10% tariff during the period of the pause.

The 10% tariff continues to set a fair baseline that encourages domestic production, strengthens our supply chains and ensures that American trade policy supports American workers first, instead of undercutting them.

By imposing reciprocal tariffs, President Trump is ensuring our trade policy works for the American economy, addresses our national emergency brought on by our growing and persistent trade deficit, and levels the playing field for American workers and producers.

Unlike previous administrations, President Trump took a tough, uncompromising stance on China to protect American interests and stop unfair trade practices.

The more we watch and listen to Mr. Bessent, we feel that the United States has a very formidable secretary that has our overall best interests in mind. He is very resourceful, tactical and clearly has the will to execute the administrations overall policy sentiments.

The risk markets are running with this and its something that we have seen building for some time now. Its also why our Magnelibra CTA markets sentiment had switched the equity complexes to a long bias. This is the thing about our analysis, we generally do not have a personal opinion, we try to keep any emotions truly outside of the markets will.

A lot of people will dismiss technical analysis and so many focus upon fundamentals, but we have found that the actual pricing provides the best outlook because it is the culmination of everyone’s decisions. The actual price reflects all the short term and long term available data all in one, or at least we assume it does, but there are nuances, there are short term volatility structures that can skew the numbers, but over a long enough time frame a pattern does emerge.

Anyway it has become apparent over the last few weeks, that many have bought the dip and have thus far been proven correct. When we look at the news that has propelled the markets higher, well many felt the risk of any further market deterioration based upon the tariffs, would be worked out sooner rather than later. This has proven an accurate assessment and now the markets are rising.

When we look at the SP500 futures, we have moved our resistance target this week up to 5885 and our support areas now at 5675. We don’t anticipate this higher trend to reverse unless we start to see a close underneath our pivot level of 5550:

As far as the Nasdaq futures the resistance is now at 21375 and 20100 is the support and this will not flip negative till we trade below 19550. You can see the long term trend slope line that the bulls are targeting once again :

So we have the risk assets being bought up again and well supported here now but it looks as if that is coming at the expense of the metals markets as we are seeing some consolidative selling occurring. Gold is getting hit hard on the new tariff announcement and is trading at $3227 -$101.50 or 3%. Here is the gold futures chart where a break of $3150 may finally see new sellers enter to push against the weekly support at $3025:

As far as Silver futures, we can’t help but think this topping pattern which has the $30 area as the key for now is still up for grabs. We know that Silver is undervalued vs Gold historically here and we may start to see Silver hold up better than gold here if we do indeed start to pull back. Just to put silver into perspective the $32.50 area is exactly where it was one year ago. Compare this to Gold, where last May it was trading $2350 and now its $3240!

The U.S. Bond market doesn’t like the risk on theme or so it seems as yields are jumping today. The US Govt 10Y is +9.5bp now nearing 4.50% once again:

This is an interesting dynamic and we know yields in JGBs aren’t helping at all either but they are long overdue for their yields to rise there. As far as yields here in the US, we suspect once these trade deals are finalized that the US will be in a much more better fiscal state and the FOMC will begin to cut rates even if it is at a slow pace will go a long way to reducing the U.S. net interest costs.

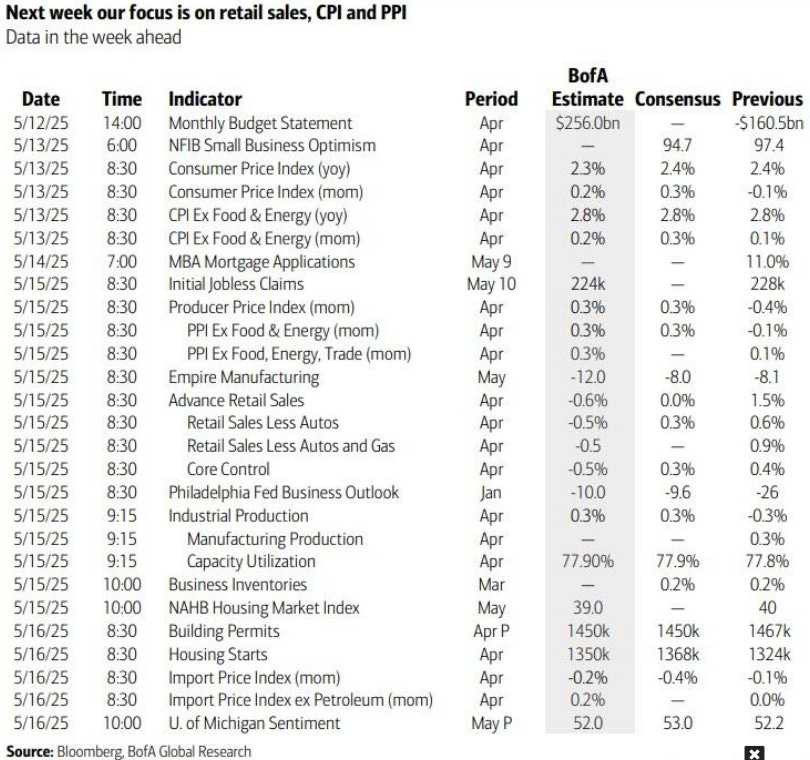

Alright, all eyes this week will be on the CPI report tomorrow and PPI report on Wednesday. We feel the Federal Reserve can play the waiting game here to see if Trump’s tariff policies end up hitting the markets again, or if China concedes and we start to see a bigger shift transpire over time in regards to lessening the trade imbalances that we have. There is so much confliction right now in the datasets and in the overall market tone, it is truly quite bifurcated and it makes informed investment decision making processes that much harder. Anyway this week does have some good data points to take into consideration:

We have all the MTR Subscriber data and trackers up next, we urge you to become a full subscriber and truly break through that barrier of understanding in regards to our global financial system.

We offer you a mindset that you cannot get anywhere else.

We offer you access to our data across a multitude of market segments and structured in a unique way for you to easily understand market movements and the values of those movements.

We offer a more in depth vantage point, to incorporate our work into your own investing and trading processes.

You won’t be disappointed! Sign on today and feel the power of being the smartest person in the room, when others pretend they know, YOU WILL KNOW!