Continued Defensive Play

Tesla no help

Well Tesla earnings didn’t help things and pre NY open has Tesla ready to open down about -6%. As far as the 3*1 put spread we proposed at the end of Sept…well #winner to those that took a look at that, in fact its down about $80 a share since then so that play was highly conservative:

Last nights trade was defensive once again in Equity futures, however the Chinese came out around midnight and announced a possible reduction in Covid quarantine times…yea they are still doing this…and futures jumped about 20 handles in the SP500. Anyway the charts are obvious, 3675/3680 area is huge and rest assure 1 DTE options are heavily purchased and sold against a breakdown here. We will go more into that after a look at the charts 3735 and above is key for bulls:

As far as the Nasdaq a massive triangle has been built and our next move will be born out of a break of this:

Back to what we were saying about 1DTE options (days to expiration) A lot of deployment out of levered fast money firms to utilize these given the levered games they play and having to have the appearance of risk tolerance. 1DTE options do a great job in masking overall delta risk and they are being increasingly used. Secondly and as Nomura’s Charlie Mcg. has recently said,

“Unprecedented “Weaponized Gamma” from the “institutionalization” of 0-1DTE Index / ETF options trading causing “intraday chase” flows we’ve never seen the likes of previously. US Equities options front-Delta to trade into Op-Ex at levels only seen during prior Vol Shock / “crash” periods” -Nomura Charlie Mcelligott

In his recent piece he also talked about the Yen and we have also, in fact we posted this chart on one of our feeds yesterday:

They know full well what they are doing, they are hoping nobody notices and that the US reverses their rate hikes in 6>12 months…good luck with this, right!

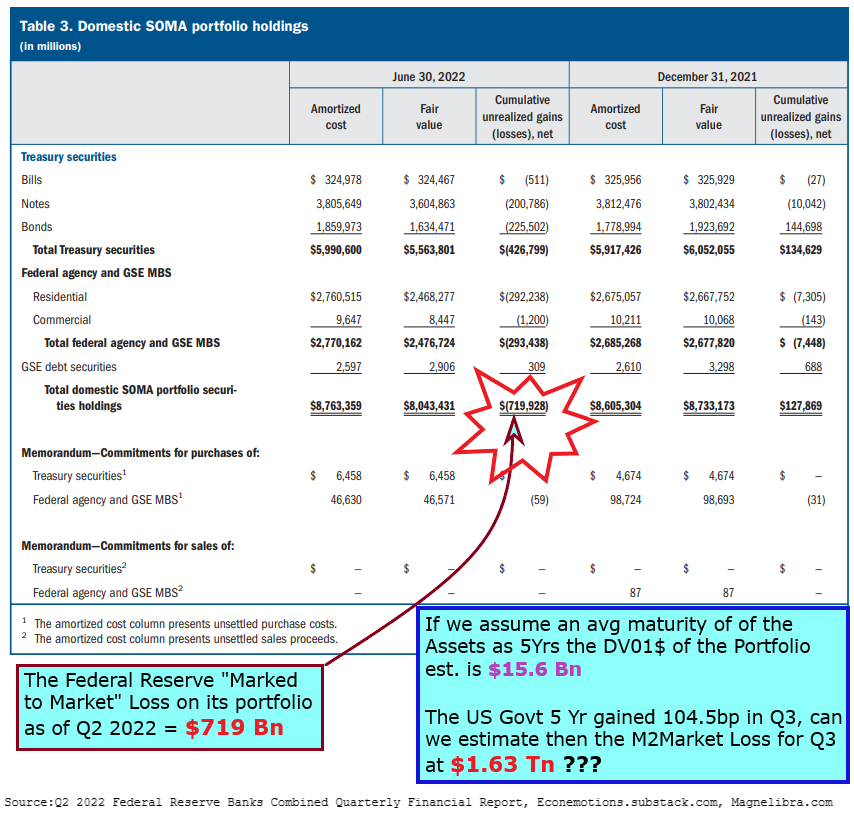

We also posted a graphic on the Federal Reserves Mark to Market losses they are incurring. We have done extensive research on this and we know they do not need to make a profit, however, let’s be honest, You can’t reduce your balance sheet much if you expect to conduct your mandates appropriately. From our estimates, they will lose close to $1.6T, yes with a T this coming Q3 report. We peg their DV01 at about $15.6B. We hope we are overshooting and yea they do have MBS which are longer term, however those are not USTs and if housing cracks…well we know how that stuff will be priced. Anyway here is our graphic which shows the Q2 loss of $719B:

Finally and something we will touch upon is the US 30 Year cash treasury, it continues to get pounded both outright and vs their corresponding futures…i.e. a consistent and unrelenting seller exists and you know what with 60/40 portfolios taking it on the chin, how can we blame them…60/40s aren’t suppose to work that way, in a theoretical world, perhaps, but as debt rises…rest assure all outcomes are possible.

To say this year is an outlier is well, an understatement. Magnelibra has been warning for years that the monetarist “inflate at all costs” house of cards is nothing more than a mirage of wealth.

As we state time and time again, unless you sell you don’t monetize. However even now, if you monetize your actual return is discounted by a large 8% plus inflation rate. Its pretty obvious at this point that the size of the US debt and the Federal Reserves Balance sheet can go nowhere but up and if geopolitics has their way and the United States continues its current ways, well the empire will have a very tough future. In fact if you start to look at the integrity of our communities, well, you begin to wonder, if we haven’t already begun our descent…

Till next time.

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Econemotions covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2022