Credit Suisse Bailout? NQ Safe Haven?

Alright as we have noted plenty of times, it is the contagion from these bank issues that is problematic. For those that haven’t been around long enough to remember LTCM in 98, Tech bubble in 99, the 2009 TARP, we can only tell you the global central banks do nothing more than give electronic credits to systemically troubled firms in order to slow the sentiments of collapsing value.

Ultimately nothing structural ever truly changes and the risk is born or transferred to the bigger fish for discount.

In fact this what the central banks do, they concentrate money and risk at the center while the peripheral economy is caught in the crosshairs with defaults, real risk, real wealth destruction and of course INFLATION.

Speaking of risk, we would like to know exactly how the US Treasury and Federal Reserve are getting around Section 165 of the Dodd-Frank Act specifically this statute under Part 2 Section C here:

(2) CONCENTRATION LIMITS.—The concentration limits referred to in paragraph (1)(B)(v) shall—

(A) prohibit such a company from merging, acquiring, consolidating with, or otherwise taking control of, another company if the resulting company’s consolidated liabilities would exceed 10 percent of the aggregate consolidated liabilities of all financial companies;

(B) prohibit such a company from merging, acquiring, consolidating with, or otherwise taking control of, another company if the resulting company’s consolidated total assets would exceed 10 percent of the aggregate consolidated total assets of all financial companies;

(C) prohibit any company from merging, acquiring, consolidating with, or otherwise taking control of, a depository institution if the resulting company’s consolidated insured deposits would exceed 10 percent of the aggregate consolidated insured deposits of all depository institutions;

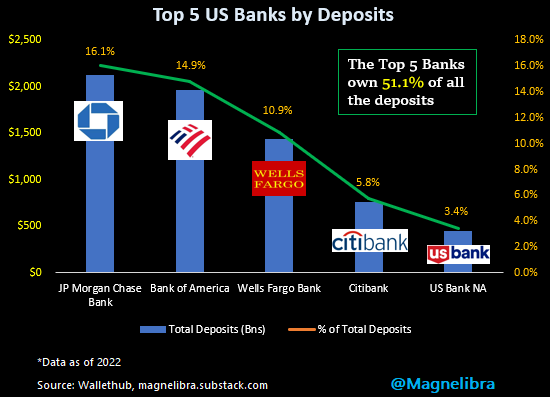

As this graphic clearly points out, there is no doubt JPM, BofA and WF are above this threshold and we would have thought Congress would have to amend Dodd Frank to do this legally at least…then again, we suppose emergency measures are exempt from this like every other time. Our bank graphic has the deposit breakdown here:

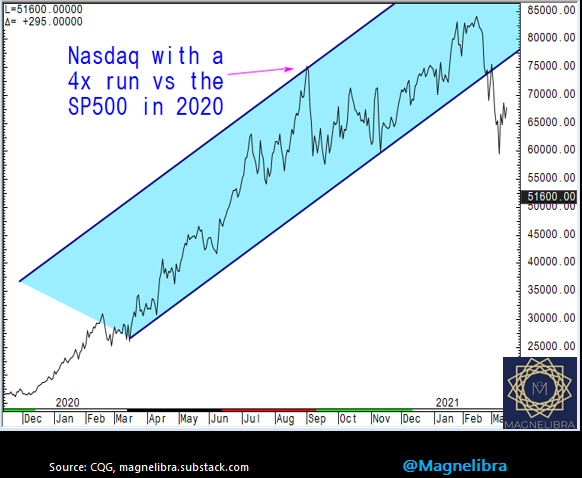

Despite everyone knowing that that Credit Suisse is next up and that the Saudis said no thanks, which means the SNB will of course be part of the solution, the equities in particular the Nasdaq were a safe haven trade today. The chart structure is a bear market downtrend counter rally and we aren’t surprised to be honest we saw this with the Nasdaq Index post Covid as it well out paced the other indices to move onto record highs. Here is 1 Futures Contract of being long the Nasdaq vs Short 1 SP500 during 2020:

Now we aren’t showing you this chart to say the NQ is about to explode, rather we are showing you this as a spread product trade by which you can employ a long equities position while shorting another equities position. We believe the NQ is being looked at as a safe haven as money is flowing out of weaker names and into the Tech heavy index. This makes sense especially if you are a young asset manager that hasn’t seen a lot of bear markets in your life.

Anyway this chart set up seems ripe for a big move either way. We aren’t saying that we believe the Nasdaq will tank, nor are we saying it will bust out of this structure to the upside but one thing is certain, it is going to move and we suspect by quite a bit. By the way, buying into these chart channel highs has not worked out very well:

Technically, 12263 is our terminal line for the train moving south and we suspect sellers will be patient waiting up at 12440/12465 area. As for a couple of options plays one can look at both put and call spreads with a skew towards puts given the location of the market vs the chart structure.

With a June Futures settle of 12377.75, the week 4 Nasdaq Friday Expiration 12500/12700 call spread settled at 83.75 which is a risk reward of 2.38:1 (200/83.75). While the 12250/12050 put spread settled at 62.50 which is a risk reward of 3.2:1 (200/62.50). Seems like the market skew is to the upside as options players are suggesting further price increases, but obviously with the ECB and external factors that could change very quickly.

Speaking of young asset managers, we had the luxury of speaking with a former CIO of a very large public pension fund yesterday and we discussed the gamut of topics. One thing in particular that really stood out during our conversation was that he pointed out the fact that the markets are generational and that a lot of managers over 55 have retired or moved on and now the monetary flows are controlled by those in their late 20s/30s types. This has a profound effect upon markets given the psychology of this generation. In fact this all made perfect sense as to why at times the overall markets trade with a consistent bid to them equity wise, because its a whole generation that has been conditioned this way. So with that posted this on LinkedIn today:

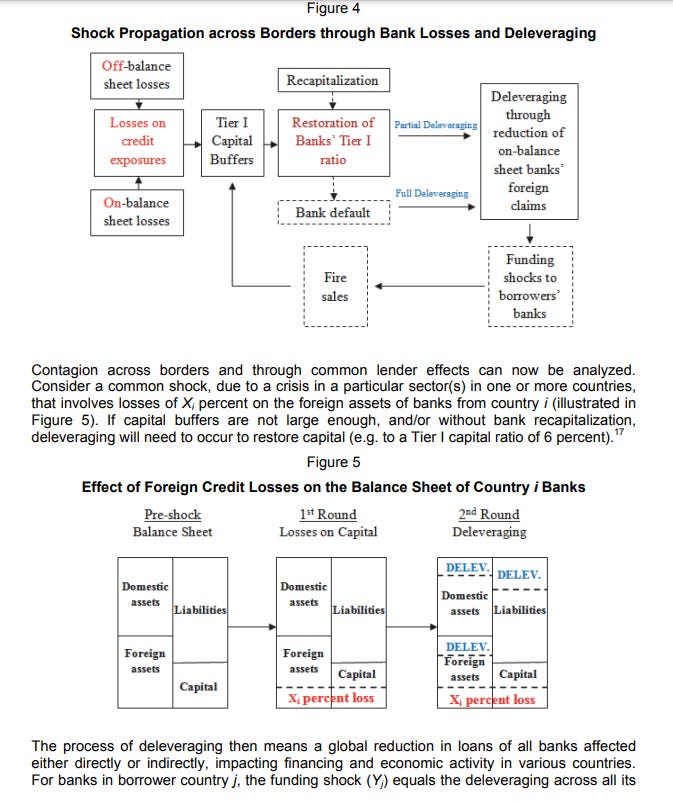

For all you late 20s and mid 30s investment managers out there who have never experienced a regime that wasn't BTFD, here is a graphic for you on how the deleveraging process works when it comes to GSIBs. This BIS paper from 2012 offers some good insight into a problem that will always exist in a QE fiat fractional world (banking credit risk) and best that we all brush up on it, so that we can all try to stem the tide of what is coming...SVB is just the start, these things have a way of spreading like a virus, so you have been warned...and no the FOMC and the US Treasury cannot cover all deposits, that is something they shouldn't even plant inside investors heads...their system is not designed that way. The graphic attached is the deleveraging flow chart. With Credit Suisse and no doubt countless others on the global watch chart we felt this is relevant.

Here is the link to the 2012 BIS paper, BIS Systemic Risks in Global Banking and yeah we know most of the managers out there now were drinking Fireball at the Frat/Sorority house when this came out, hey that’s ok there's a time for everything!

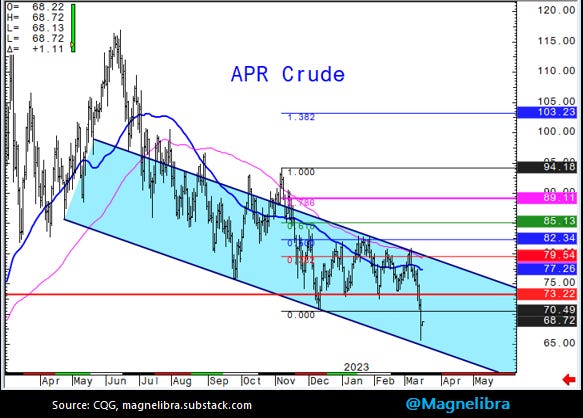

In other markets, Crude continues in the bear channel and today we saw our first real test of the bottom of this channel. April Crude sold off to the $64 area that we talked about yesterday and it was firmly rejected and rallied $4 from these lows. This is not a hole you want to be caught short in…

April Gold hit $1940 today and put in a real decent technical top here and we would suspect better sellers here now:

Alright that is it for now, here is a more in-depth piece from Zerohedge a bit more technical but its all about following the monetary flows. We have for years followed FRB H4 and now H8 will be under scope as well to see any hints of big changes to A/L. Here is the link, How To Track Bank Runs In (Near) Real Time

Hope you learned a little bit of something, please share our work and subscribe today, in order to subscribe its like 17 cents a day or something like that for information that to be honest is invaluable if used correctly!

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023