Dollar Down So Futures Green Across The Board

ZIRP = Greater Risk Taking

Just a quick mid-day update here as futures markets across the board are rallying off of the US Dollar weakness and more importantly QE is beginning to ramp up once again as Arbitrageurs will continue to front run all the FED POMO operations forthcoming. Any way here is a good heatmap from Finviz:

Per our Asian market update last night we noted the stop hunt on the open in the SP500 which promptly ran the futures down below 3030 to only see a constant bid, run right into our 3090/94 resistance. The market stagnated around this level for the last 5 hours, however now the bulls seem to be in short term control above the 50eMA and important 3093 area which has now led to higher probes above 3100:

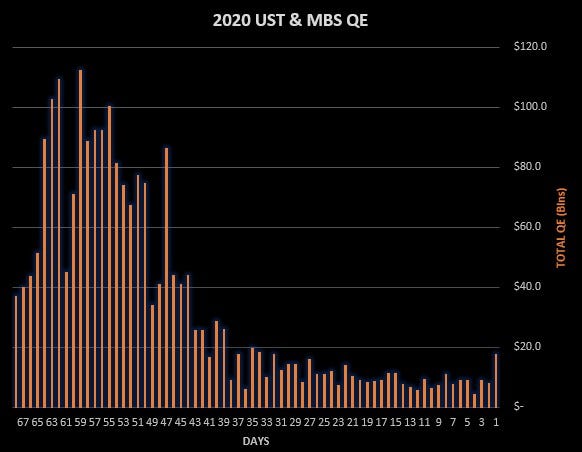

We can’t help but think the GFBP Program Tracker will have a very short tolerance here with the equities having such a seemingly easy time bouncing 60 to 70 handles. We know the volatility isn’t conducive to keeping the tracker held down and rather its built in mechanisms will reduce positions given this type of behavior as its an indication of relative uncertainty and lack of true conviction and more of an algo based HFT predatory environment. So we will keep you in the loop as to any changes made for our subscribers. For now the global markets seem to be front running what is for sure going to be a steady, linear rise in this total QE - UST & MBS in the months to come as depicted in this chart here:

QE goes a long way in buying record asset prices and has a tendency to induce a widening of the risk spectrum for investors as they hunt for yields in a never ending ZIRP environment. This is not how free markets work, in fact here is a graphic of how they should work:

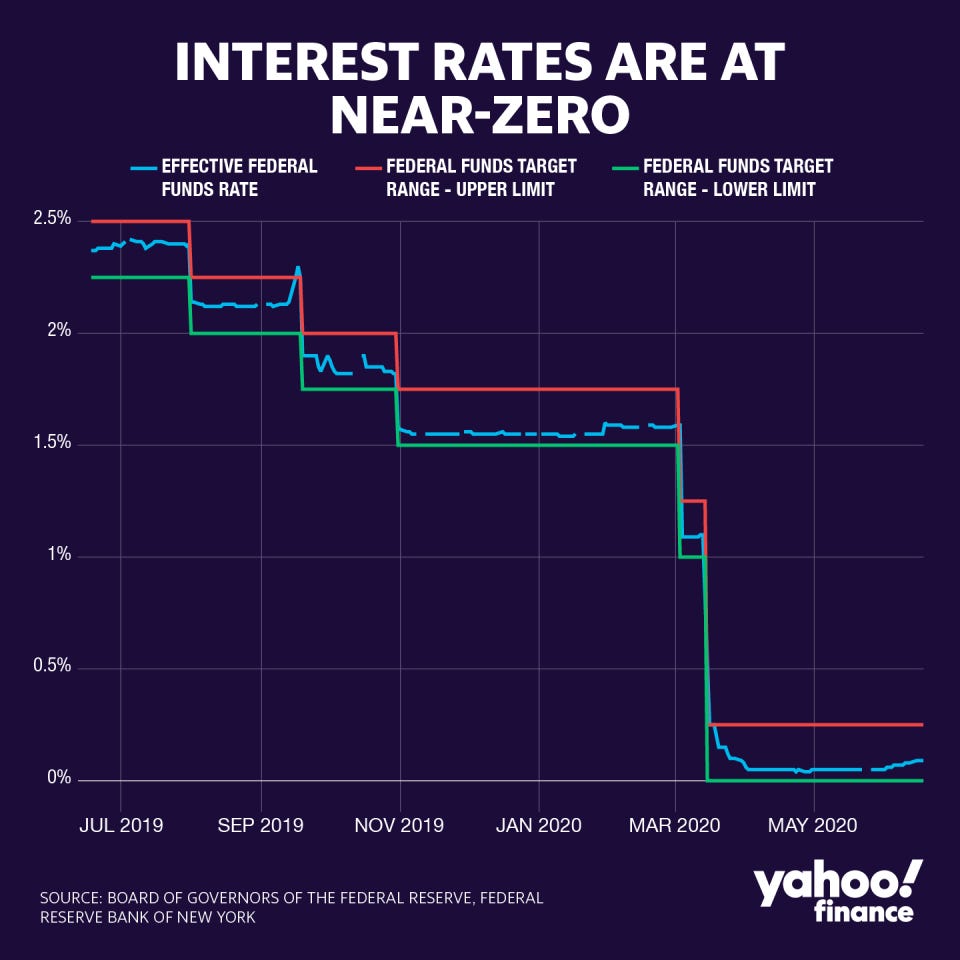

Since that is no longer the way things operate and in fact, Shelia Bair was out this week as a contributor to Yahoo Finance with an article on this very subject of low interest rates inducing risk taking. For those that didn’t see this article, Low interest rates widen the gap between Main Street and Wall Street Sheila Bair does an excellent job of explaining the mechanism by which low interest rates transfers into higher equity prices despite the risk difference between the two. Yahoo posted this nice graphic:

She also touches upon the mechanism by which corporations arbitrage low rates and change their capital structure to accommodate issuing debt via lower rates and issuing dividends and buying back stock which also contribute to higher equity prices. At the end of the article she said this:

“I am happy for investors that the stock market has done so well despite the pandemic. But the giant chasm between the struggling real economy and inflated stock values is something we should all care about. If we need more stimulus, instead of charging households for saving their cash, maybe we should think about just giving them more of it.” -Sheila Bair is the former Chair of the FDIC

This is a very telling statement, is she advocating for a supplemental program like Universal Basic Income? Sure sounds like it, so on one hand the article is defining a low rate mechanism designed by central banks and done so artificially via printing debt, yet she throws in the towel at the end advocating for direct UBI which would require even more debt printing.

OK, we hope you have a great week and we hope you continue to spread the word on our work here with your friends and colleagues, remember, knowledge is key and it is the absolute goal of Magnelibra’s Econemotion to put you always ahead of the pack. When your family, friends and neighbors ask, how you know all this stuff, we hope you point them in our direction. We hope you consider contributing to our work and joining as a monthly subscriber and for the professional traders and investors, join our Founding Subscription because the position tracker is a uniquely proprietary driven model designed as a global macro market analytic that we believe can help to advance your trading and investing game.

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.