Economic Numbers Starting to Slide

Nasdaq lower Nvidia hit?

As Magnelibra has pointed out over the last year, the FRB has painted itself into a nasty corner, shackled by QE and ZIRP which were allowed to perpetuate their thievery of future earnings, bringing forward realized capital at the expense of future growth. Then came Covid and the real transitory inflation of DC money hand outs known as “stimulus.” Long time Magnelibra readers know that we are in full agreement with the great Milton Fr. and his economic viewpoint that,

INFLATION IN THE UNITED STATES IS MADE IN WASHINGTON AND NOWHERE ELSE, IT BEGINS AND ENDS IN DC - Milton Friedman 1978

The current situation is a lot worse than they want you to believe, yet it is masked by the FRB and their policies alongside the US Treasury and the rest of DC, which instead of allowing institutions to fail and for investors to take on losses, they claim or Yellen claims that they have the ability to backstop everything.

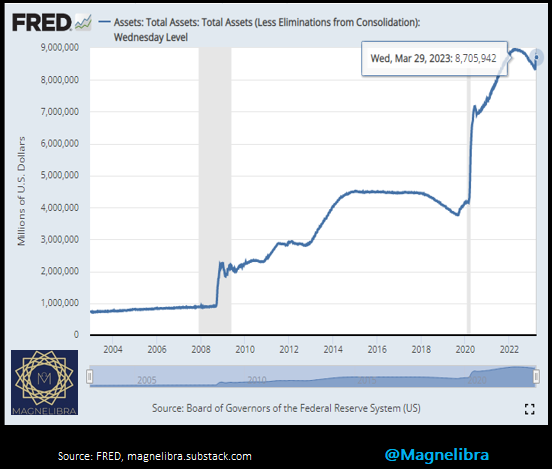

Who believes such hypocrisy! Their idea of backstopping is simply solving a debt problem with more and more debt! Case and point it is taking more and more asset expansion by the FRB, increasing their balance sheet by many factors to just keep the status quo. This utility has outstripped the rational economic output of the general economy and is destroying real value now by deflating the purchasing power of ordinary Americans and the rest of the globe for that matter:

If inflation was the real “sticky type” problem, then this would not be the type of balance sheet approach one would expect from the central bank. Rather they would be reducing this pig as fast as they could, but they are not.

Instead their monetary policy approach is to push short term rates higher (which we agree with) but at the same time, continuing to increase their balance sheet (which we DO NOT agree with). Not to mention the permanent effect of destroying retail banking Net Interest Margin and HTM portfolios, which is why we see SVB and the rest suffering!

These are counterproductive forces and one that clearly benefits Wall Street/PE/IB etc. at the expense of the mortals on Main Street. What this also does is that it removes to very important and structural economic mechanisms by which Main Street has been allowed to survive up until now.

These two forces are the de-facto ATMs of Main Street Credit Cards and Housing Refinancing, both of which now are very much working against the main street consumer.

On the credit front, we have record usage, coupled with 20% plus interest rates and an increasingly tighter lending standard market. (Now imagine if people start to lose employement) We also have housing refinance virtually destroyed with mortgage rates at 6% plus and until that rate goes to < 3% well, you can rest assure that ATM is no longer going to be tapped, and will real estate even hold values to continue this duration extension for the consumer??? Its probably only a matter of time before we see FNMA and FRMAC, HUD start to change some rules or implement some type of loan products with kickers at the request of the FRB and US Treasury.

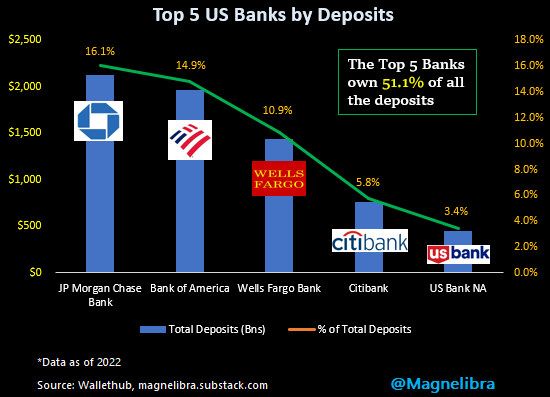

Don’t think for one minute the FRB doesn’t know what it is doing either! It is doing exactly what Section 165 SubCp C prohibits (or used to, the rule has probably been struck from the act):

(C) prohibit any company from merging, acquiring, consolidating with, or otherwise taking control of, a depository institution if the resulting company’s consolidated insured deposits would exceed 10 percent of the aggregate consolidated insured deposits of all depository institutions; and

We suppose forcing smaller banks to close and shift deposits to larger banks is not considered “consolidation” via legal take over semantics, but the reality is the banking sector is consolidating rapidly and will soon hit anti-trust levels. Maybe JPMCs 16% has only 10% insured, but if Yellen says they are going to insure all deposits, well, then we suppose this rule will just be bypassed under 13(3) like everything else the FRB does:

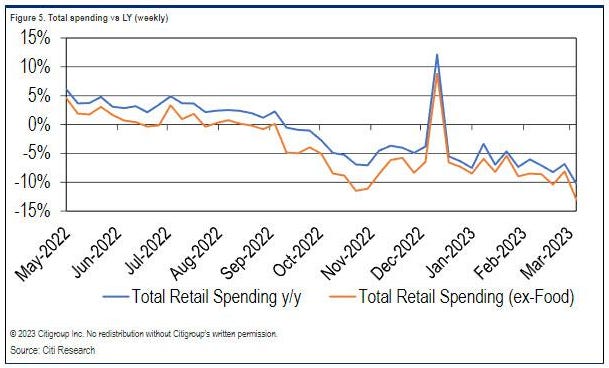

All in all we know that the general economy is getting hit on all sides and we are starting to get confirmation in the numbers, JOLTs, Retail Spending, ISM services, they are all pointing to a coming slowdown. Look at this total spending progression, does this look like a booming economy to you?

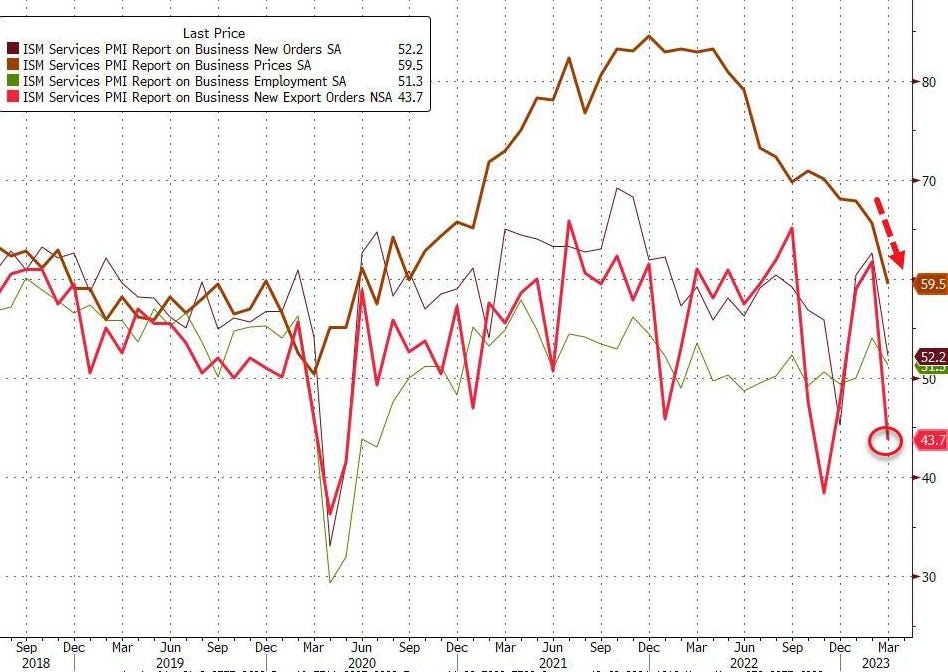

Also that pesky ISM services Powell still thinks is running hot, well its at the lowest level in nearly 2 years:

With all of this in mind, with the US Yield Curve continuing to steepen out, we can’t help but think the bond market knows something. We know money is hiding in the Nasdaq, its the wealthy bank accounts, yet if the tide is really turning, then asset prices will be discounted and as Magnelibra has pointed out time and time again, equities peak and fall “AFTER THE ACTUAL FIRST RATE CUT.” The US Govt 2Yr is down about 125bp off its peak, if that is not a cut, I don’t know what is!

We suspect this time won’t be different and after the FRB does submit and tap out of the bond markets steep yield curve stranglehold, well even the Nasdaq will be hit, because its all just a wealth mirage as everyone cannot sell and monetize, just as the FRB and FDIC cannot give everyone cash for their deposits, despite the lunacy of such a claim. ($17T in deposits and only $3T in cash that exists) They must really think people are stupid…

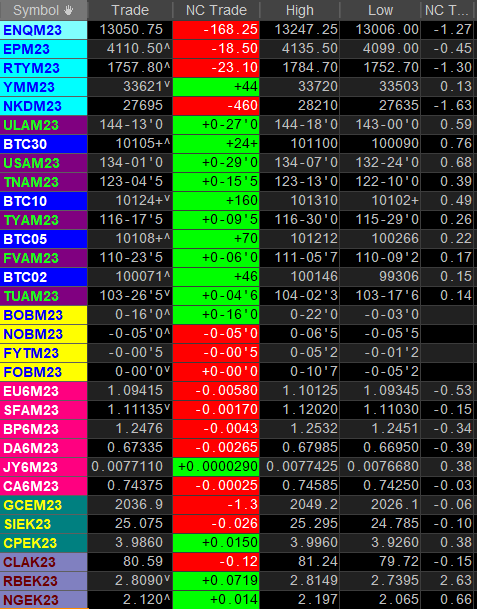

Anyway, let’s take a quick look at the markets today:

Its pretty muted across the board with the Nasdaq and Russell leading equities lower down 1.3% each(Nikkei -1.6%) and RBOB continues to power ahead with the energy supply constraints and cuts as the commodity is +2.6%.

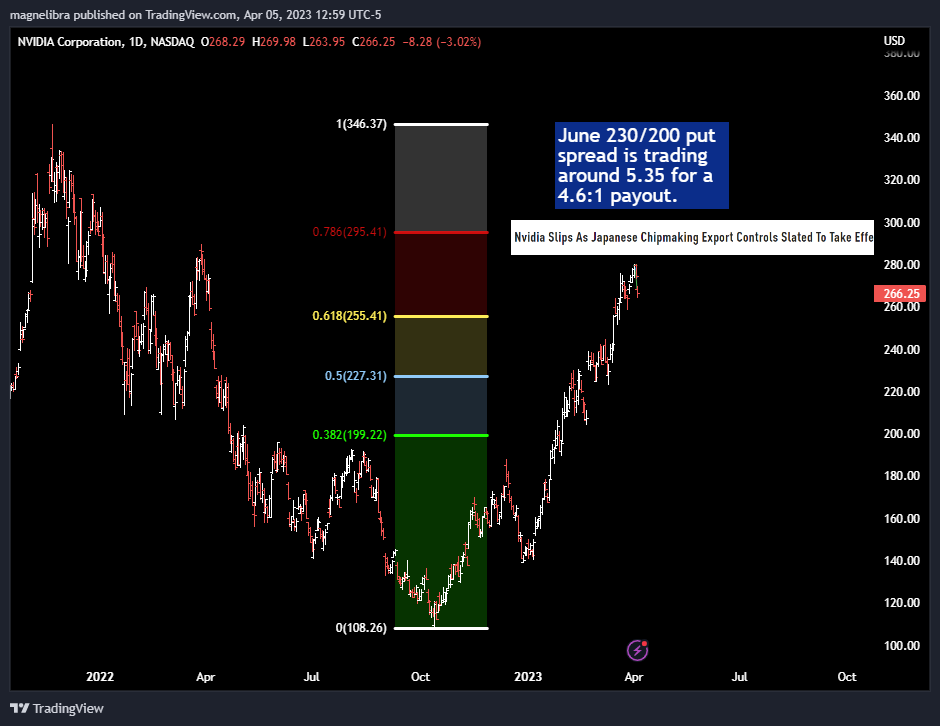

Speaking of the Nasdaq, we touched upon Nvidia last week and how its priced for perfection, well we are starting to see some fundamental news come out, so that means a few big shots have gone short and are confirming with news items (our take on how the system works)

Here is Nvidia and the put option we thought made some ratioed payout sense last week and today’s headline that Japanese Chipmaking export controls are upcoming:

This is not a recommendation to short Nvidia, rather Magnelibra looks at trade setups, cost structures, chart structure and future outlook vs past historical technicals. Trading and investing are personal attributes with varying degrees of understanding, capital constraints and risk tolerances. What you see, what we see can be very different but outlining setup, risk/return profiles are pretty static in nature and that as what we like to point out.

Ok keep things simple, we hope you continue to read our work and share it, we are making this one a freebie so share it so we can all grow and learn from each others experiences!

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023