Employment Better Than Expected

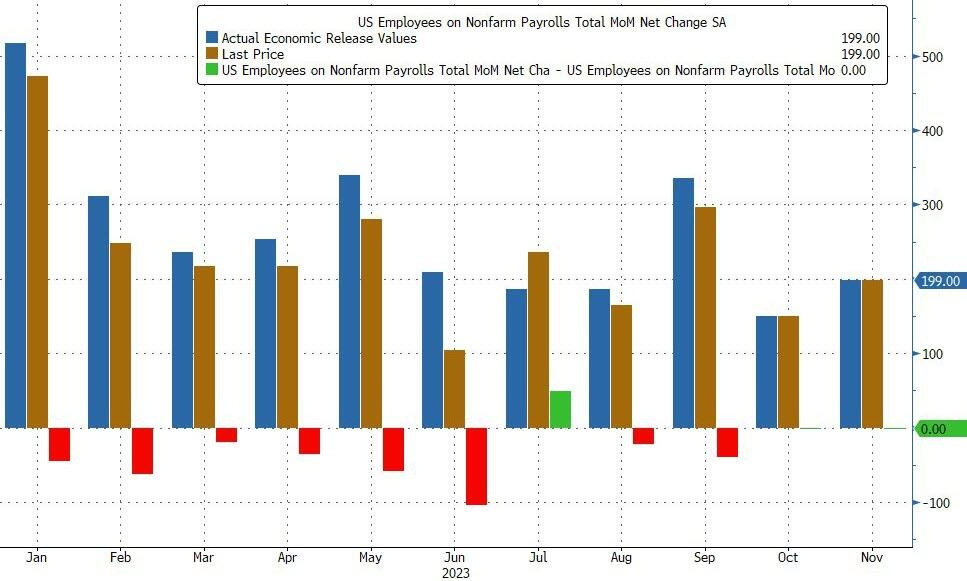

What has been a continued and ongoing theme, once again we saw the November employment number beat expectations coming in at +199k above the +183k consensus. The majority of gains came from the striking workers returning back to work and as has been the case much of this year prior months once again revised lower. September was revised lower by 35k and October was magically unchanged.

We knew today’s report was most likely going to follow the trend this year of beats and revisions lower. The equity markets initially sold off on the news but the day is not done yet, so will see how the masses take it. The equity markets aren’t really a function of anything other than consistent employed 401k in flows. Economics don’t matter unless there are massive layoffs and redemptions and it is apparent that having $3.5T in reserves is enough base money to support current valuations.

The fact that the US bond market over the past few weeks has decided that 100 to 150bp in rate cuts next year are expected, todays number today should put a little damper in that expectation! For now bond yields are up about 10bp in the front end and +7bp in the long end so a decent flattening of the curve there. We continue to believe the FRB will keep rates higher while desperately trying to reduce the balance sheet. The Reverse Repo Program continues to hover around $800 billion and so the liquidity is still ample, until we see this drop to zero, we won’t expect the leverage to be fully purged yet. Weaker hands will have a harder time once this liquidity is drained and then we will see if the equity and real estate markets start to show signs of cracking. We aren’t there yet, so we don’t expect any major moves out of any of the markets until then.

As for our subscribers the settlement page, trackers and further insight are up next.