Equities Showing Life

settles + bonus charts

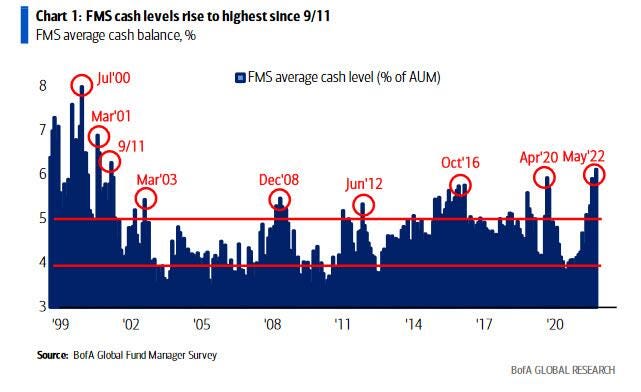

We have a couple of highlights out of the most recent BofA piece that we wanted to share. The first up is the ultra contra indicator in regards to Long/Short or Fear/Greed inverse indication. We know when everyone moves to cash [an asset whose purchasing power is falling around 10% per annum] that everyone is playing it safe. This has been a great historical indicator for market turns. We agree with some of the sentiments this picture paints as the easy trade of selling is no longer the case. Rather we suspect the pain trade to be a higher one in here for equities:

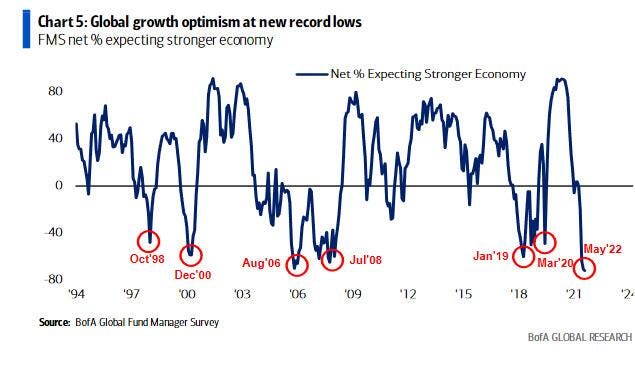

They backed this chart up with this one which clearly shows everyone on the same sentiment side for a weaker economy:

We have spent many years learning a very important lesson when it comes to the Federal Reserve and central banking in general, that lesson is solidified in this mantra

DONT FIGHT THE FED

We do not agree with their methodology for debt fueled growth but as we opined time and time again, the FED does an excellent job of buying time, decades of it and this time around won’t be any different.

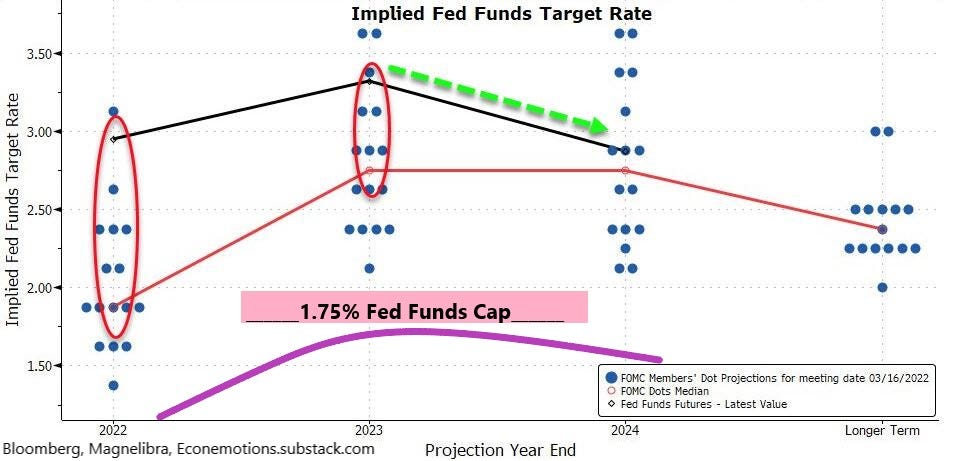

We know the structural issues that have taken hold in the supply chain, will eventually be alleviated and that some of the excesses by those with debt driven expansion will find it difficult to continue such speculative fervor as debt costs have and will continue to rise. Everyone expects 7 more rate hikes, if they are 25bp at a crack, this is 175 bp from here for FED FUNDs or 2.50%.

The market knows it and all the algo driven AI bots have already found the discount to asset prices and have promptly shoved Equity assets down to their equilibrium pricing accordingly. However are they being too optimistic in regards to the FEDs ability to get to 2.50%?

Yes we think so and we would rather think that the FED will probably get to 1.75% or 2.00% at best as $9Trn in balance sheet is a formidable force for interest growth and we don’t want interest costs interfering with longer term price stability. We showed our analysis in this chart prior and we will stick to this call for now:

Once we see pricing integration no longer being allowed to pass on to the general consumer, the general equilibrium of prices will start to trend down. We could see the FED by the end of this year after a few rate hikes moving to a more wait and see approach. This is why we feel the discounted markets especially the Nasdaq are in the early stages of a bear market rally.

Please do not confuse what we are saying for the longer term, the equity markets will start to run into problems again if the start to over shoot and we definitely think that once Fed Funds rises above the US 10Yr rate if and when, then we will move our focus to a more a bearish outlook. For now, bear market rally seems likely to continue.

Alright onto the charts, speaking of the Nasdaq this technical bounce will run into 12889 at some point and that will give us a much better indication of money moving back in or using it to reset shorts:

Our MAANGMT proxy for the Nasdaq does look technically ripe for a continuation of this bear reversal:

With this in mind let’s look at Netflix where 2017 pricing seems to be attracting buyers as well:

Lastly we wanted to touch on the Crude market as pricing has been a bit sticky here near $110 but we noticed the trend channel that has allowed us to keep a good eye on this uptrend continues to give it resistance. Basically $98.00-$114.00 has seen the core of the support/resistance for the last 3 months:

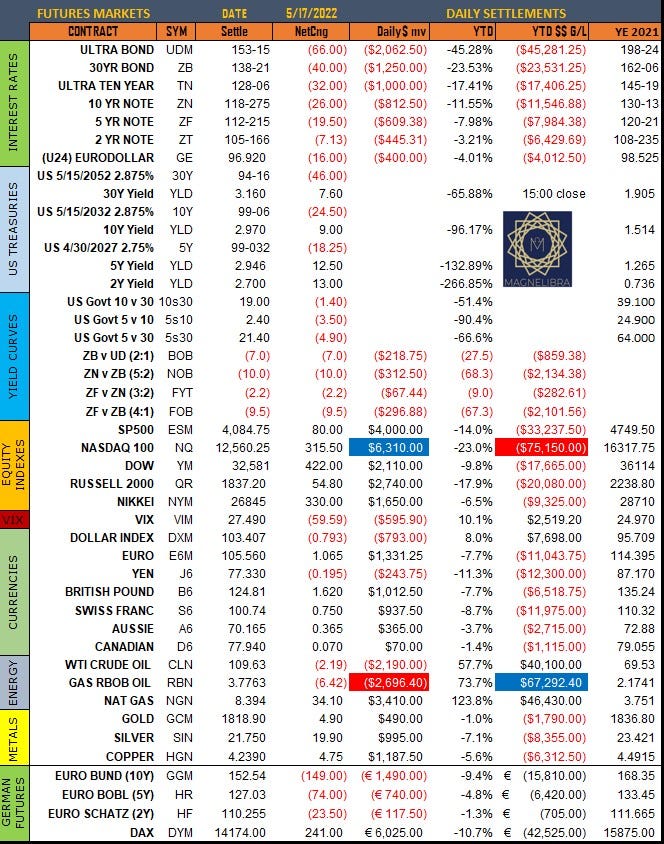

Ok that is it, we leave you with the settles from today’s action for the markets we follow:

Till next time…

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Econemotions covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2022