Equities Slammed and Buyers Step In at Key Fib

Senate Passes $1.7T Spending Pig

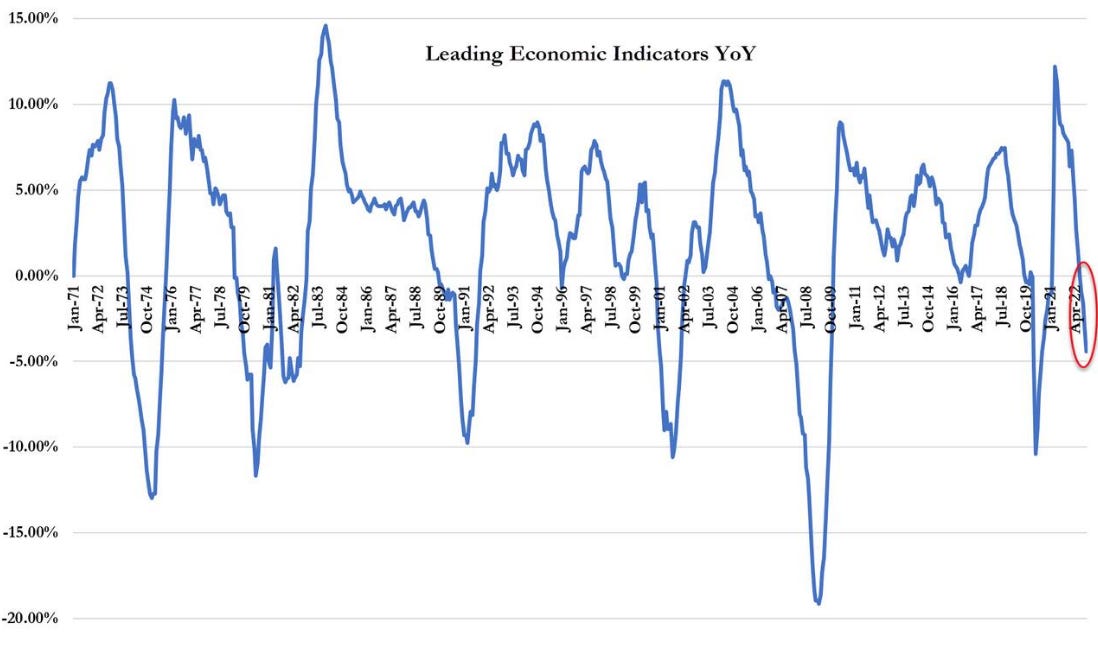

This morning had two economic data points which didn’t help the equity bulls whatsoever. Final Q3 GDP came in at 3.2% vs exp. 2.9% which seems a bit inflationary, but as you know we don’t view inflation as the main theme for 2023. We also had and what we believe is a more important number, which was the Leading Economic Indicators or LEI. This Conference Board indicator fell more than double the -0.5% expected to a massive -1.0%. The LEI peaked last year and is now down -4.42% off its peak:

We know consumer sentiment is key to both inflation and the overall veracity of the economy and this is not good, not in any sense and we believe this is predicting a major slowdown come next year.

Ok so the damage to equities was right out of the gate after the 8:30am economic numbers. As you can see the SP500 did drop below that JPM whale strike at 3835 (short calls) and fell to 3788.50 on the lows, but as we mentioned yesterday, we would suspect buyers down there given this short call position is most likely yield enhancement and nothing structural in sentiment. Anyway the SP500 is now back up above our 3810 terminal base bull case line, where a close below there would put pressure back to new lows. Here is the 10 min chart with the breakdown:

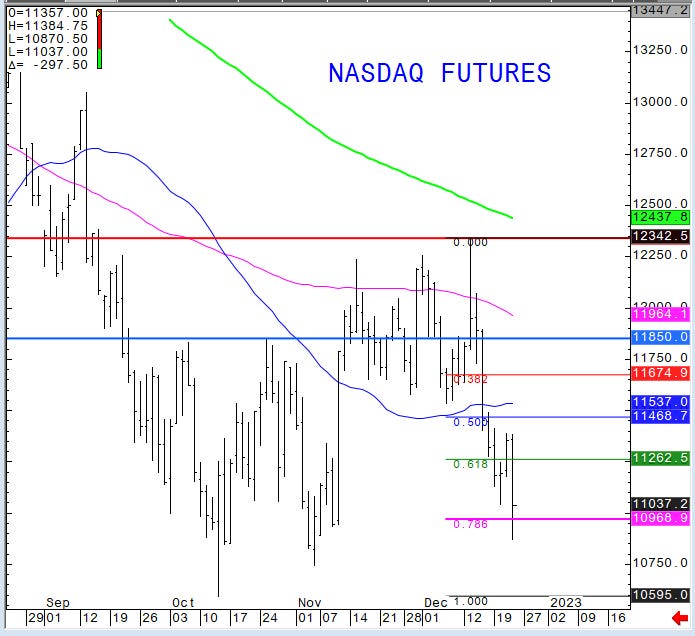

As far as the Nasdaq we liked the 0.786 level for technical measures and good target/reversal support and so did others apparently as we are now back above that 10968 area which is key. Bulls would not want to see a close below that level today:

Now we don’t want to speculate, but the Senate was trying to garner enough support this morning to pass that pig of a spending bill (as the markets were tumbling) and then this afternoon the Senate finally passed the spending bill:

We don’t want to say the early down move was pressure but once passed and around 12:30 today the markets did do an about face from the lows!

As we scan the markets overall, it is a sea of red with the longer end of the US bond market holding onto gains as the yield curve flattens a bit:

Today’s move is yet to be determined but we do know that trend following CTAs will kick in if we do get a close down below some of the key levels we discussed, most notably in the SP500 that level is 3810/3790 and in the Nasdaq 10930/10880 from our perspective. This would be the catalyst to drive these markets technically lower. It also didn’t help that David Tepper was on CNBC this morning with a few bearish quotes,

"Don't ignore what these guys (Central bankers) are saying, I don't think they will let a deep recession happen in some sense. It doesn't necessarily bare well for earnings and the outlook. It's going to be just difficult for things to go up right now because of these banks and because what they are saying." -David Tepper on CNBC founder of Appaloosa

He also went on to say,

“I’m gonna lean short. I’ll be short bonds,” I’m an optimist but I would lean short on the equity markets because so many Central banks are telling me what they’re going to do.” -@SquawkCNBC

All in all we like some of his opinion and agree but for different reasons, he is thinks the FED will continue to tighten and thus he feels valuations will be hurt, where we think they are done but a major recession will wreak the same havoc. So a little bit for everyone in the overvalued camp looking for justification!

Ok that’s is…

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Econemotions covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2022