Good afternoon, Magnelibra followers and welcome to another edition of the Magnelibra Markets Podcast. Today’s episode #50 is entitled “Equity Markets and Risk Are Liquidating”

Quick Disclaimer: The following podcast is for educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and may not be appropriate for all listeners.

We hope you listened to last weeks podcast and have been an avid follower of our work, especially when you have days like Friday and today. We want to be your source of intelligence and we abhor main stream media talking heads, all they do is sensationalize and drag out narratives. Here at Magnelibra we have decades of active and professional trading experience to improve your mindset and relay all the things we have come to know by being in the trenches of every major market move over the last 25 years.

Let’s first hit the Nasdaq futures chart, which is off its lows, but as we noted last week, below 19000 would most likely see 17100 and we love using this meme because its always just so appropriate for days like today:

Here is the chart we hit the lows around 17350 but the damage is done, rallies will now be sold against the 50p VWMA up at 18800. The market has some back and filling to do, so patience is warranted here:

So what have we come to know, well we know the Bank of Japan has been forced into a very uncomfortable pocket by which they will be raising rates while every other central bank will be cutting them. This by far is a much more sinister act for global markets than any recession moniker. This requires decades of malfeasance and manipulation to meet their final reckoning. We suspect we will continue to see the reversal of both the Yen and the Nikkei, meaning the Yen should appreciate while the Nikkei continues to fall. Now don’t get us wrong, we would never recommend selling equities on a day like today. Well unless you have to absolutely do so, which if you do, well then you haven’t been listening to us…Rather we know we will get some decent rallies to sell into as the VIX spike gets worked off and time does what time always does, “works oversold/overbought off.”

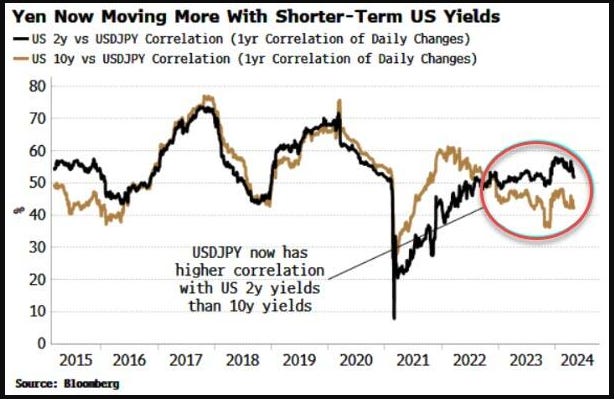

So with that and without getting into the Dollar/Yen carry trade, because there are plenty of sources you can read about that but to simplify this for our readers let’s look at the chart posted back on May 2nd this year from Bloomberg. What it shows is that the USD/¥ was becoming more correlated to shorter end yields like the US Govt 2Y:

This was in obvious anticipation of the diverging central bank upcoming moves by which the FOMC was undoubtedly readying to change course and start cutting rates, while the Bank of Japan in order to stem the slide in the ¥ and remove decades of rate control would have to begin raising their rates to a more appropriate level.

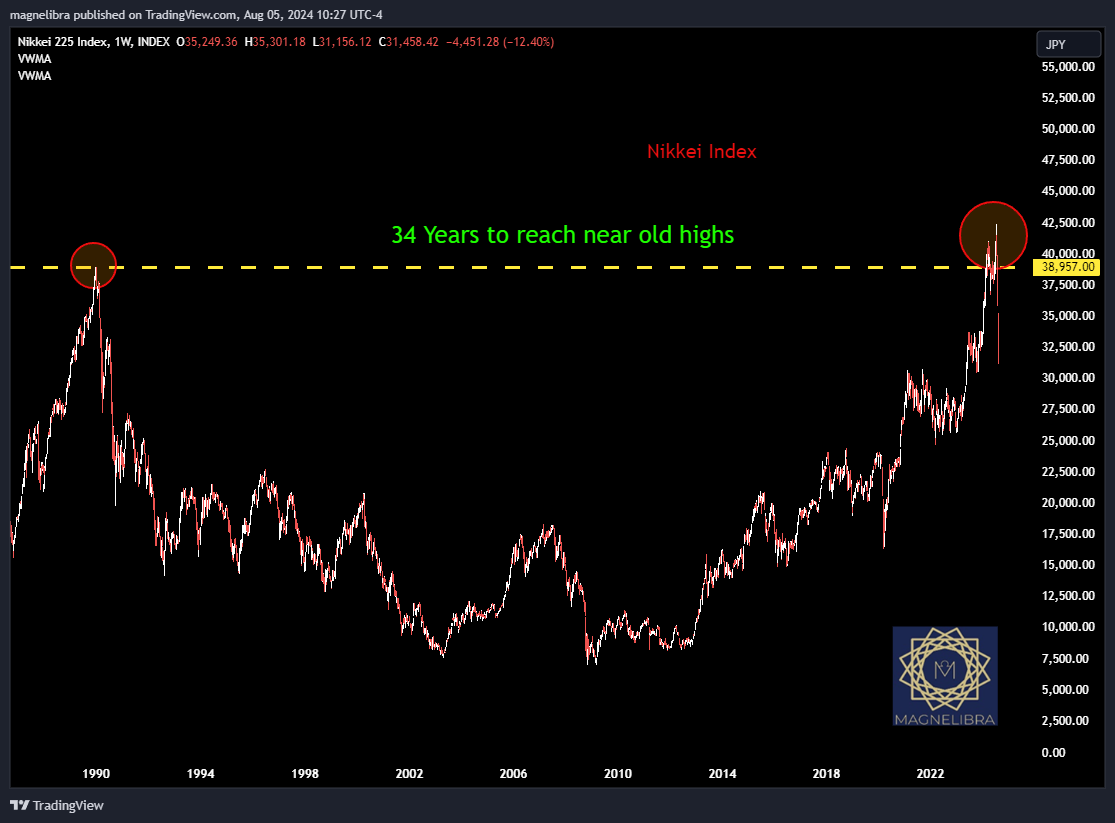

With this in mind its no wonder the Nikkei is under pressure knowing the speculation of this scenario is now becoming much more clearer and thus the Nikkei was destroyed last night dropping 12.4% and down 26% from their ATHs:

Long time Magnelibra followers should be very familiar with our Nikkei chart and we hope this is all making much more sense to you now. As far as the Yen, well here is the futures chart:

The futures have obviously rebounded and are now up 12.5% off the lows. So the Yen strength combined with the US govt yields are all pointing to the same asset class rotation out of equities and into US govt treasuries.

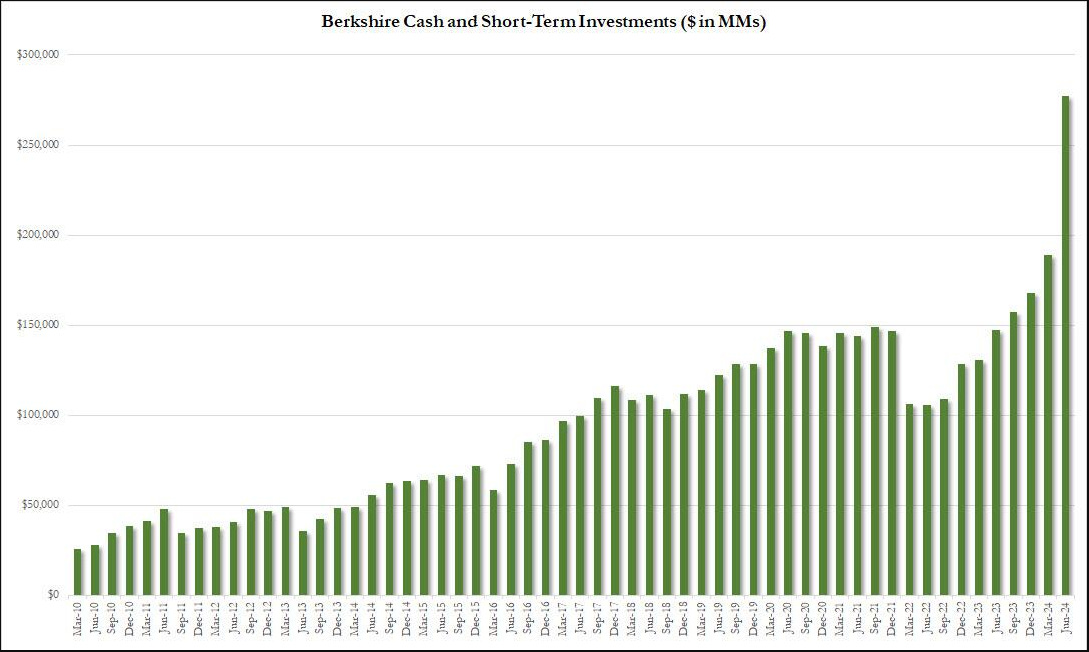

We know the big dogs have been selling for the last quarter right into the retails FOMO hands and Buffets latest filing confirms this as Berkshire’s cash horde is now at a record $277 Billion:

Obviously the US treasury market and all the convexity players are running yields lower here now and the US govt 10Y yields chart is now back into our forecast trend channel:

This recent free fall in yields has now pushed the US Govt 10Y/ Fed Funds spread near record wides, which will be narrowed by multiple interest rate cuts in the coming months with an expected 50bp cut in September and possible even a 75bp cut, which from our purview would be much more warranted. If we get a negative NFP print next month we will expect the 75bp cut to be the base case.

For those investors who didn’t park cash in 4.5% yielding 10s well, you missed the boat, as we are clearly headed back to ZIRP given our atrocious propensity to spend especially as the global economies are all turning south fast.

When we talk about rotations out of equities and into bonds, we must also note that there is an intramarket rotation as well that we have been noting. This is the liquidation of the Nasdaq longs vs SP500 shorts. You guys have seen us post this chart and we believe this rotation to the broader market out of the MEGA8s will continue for quite some time:

Finally let’s just say that in times like this, you have to stay focused on the bigger picture and the broader macro theme. The covid stimulus money has all but been transferred from the US govt, to the consumers, and now in the hands of the global elite. This will always be the progression, accelerated by overindebted plundering govts which cause brief nominal price inflation spikes to be followed by devastating deceleration in global economies or recession. This is the boom bust cycle and the FOMC QE can only mask it for so long. Plain and simple the world is on very unstable ground right now both fiscally and geopolitically and it is in that very uncertainty that investors should be derisking their portfolios till the next round of growth and global upswing is noted. Speculating and going long is not warranted by any methodology known to us right now. There will be much more adequate times ahead for sure, now is not one of those times.

We have warned also about the speculative fervor in Bitcoin and you guys know we love the technology at its decentralized core. However when we get too many regular normies and talking media heads calling for a US reserve of Bitcoin, well, let’s just say 25 years of playing the markets tell us something is wrong, even if we love it there are times where we know nominal pricing doesn’t match the landscape, and well, this is one of those times:

Bitcoin failed at the top as it has done so over the last 4 years, better pricing lies ahead between our $21k and $31k levels. Would it be a shock for Bitcoin to fall from $73k to $28k, umm no it wouldn’t in fact a 61% drawdown is historically very appropriate for Bitcoin. We also want to note that we believe the price is dependent upon the adoption rate of users, just as much as the energy cost to produce them and if the price of Bitcoin becomes too high, the network itself may prove to be too costly to use even as a reserve. What if greater adoption and wide spread usage actually lowers the overall cost of the system instead of creates an ever increasing nominal value via conversion from Bitcoin to fiat? We just aren’t certain we know the real value of the network and whether or not if the price can be solely determined merely by its capped supply or not. Time will tell, but for now, we continue to believe lower pricing is ahead not just for Bitcoin but for all risk assets. So plan accordingly!

OK that is it, we just wanted to get this out there to you guys today. Don’t listen to MSM, they are there as click bait and narrative nothing more. Think for yourself, take what we present, contemplate and formulate an opinion then research so more. That is our goal, to continue to make you think outside the box, to think very differently from what you may have been taught previously. Till next time…