Export Controls Just Created Their Own Workaround

Sakana AI's new Fugu model openly targets the gap left by Anthropic's Mythos export control suspension. We connect that story to BofA's hawkish rate pivot, the Fed's quiet bill buying, and the widenin

Bank of America flipped its 2026 rate call this week. The desk that had argued for a hold through year end is now penciling in three quarter point hikes, September, October, and December, lifting the funds rate to a 4.25 to 4.50 range. The reasoning leans on June’s FOMC projections, where nine of nineteen officials saw at least one hike by year end, and on new Fed Chair Kevin Warsh’s first press conference, which landed more hawkish than the market had priced. BofA economist Aditya Bhave summed up the call in five words: “the data call for hikes.” Markets, for context, are still pricing something closer to one move by early 2027, roughly 41 basis points of tightening for the year against BofA’s 75.

We would push back on the premise before the policy. Hiking into a government carrying $39 trillion in debt and roughly $1.56 trillion in annual interest expense does not behave like the textbook tightening of 1994 or 2004. Every 25 basis point move on that stock of debt is closer to $39 billion in additional annual interest income transferred from the Treasury to the private holders of that debt: money market funds, banks, foreign central banks, retail savers parked in bills. That is not contraction. That is the transmission mechanism running in reverse of what a hiking cycle is supposed to accomplish, and it is the same interest income channel we laid out at length in our working paper on fiscal dominance. If BofA’s hawkish pivot plays out, it becomes a live test of that thesis rather than a rebuttal of it.

There is a second, quieter piece sitting underneath this. Since mid December the Fed has been buying Treasury bills in the secondary market through what it calls Reserve Management Purchases, roughly $40 billion a month, alongside reinvestment of maturing mortgage backed securities principal back into bills. The Fed insists this is not quantitative easing, it is balance sheet maintenance for an ample reserves regime. The balance sheet does not care what it is called. It is growing, week over week, by design. Combine a Fed that is structurally a buyer of government paper most months with a hiking cycle that pays more interest on that paper to whoever holds it, and the inflationary mechanics do not point in the direction BofA’s headline implies.

On the technology side, watch what just happened with Anthropic. The US government issued an export control directive in mid June ordering Anthropic to suspend all access to its Mythos 5 and Fable 5 models for any foreign national, anywhere, including the company’s own foreign employees, over a disputed jailbreak finding. Anthropic complied and disabled both models for every customer rather than attempt to segment by nationality. Within days, Sakana AI, the Tokyo lab known for evolutionary model merging, launched Fugu: a multi agent orchestration system sitting behind a single API that coordinates a pool of other frontier models, including instances of itself, to deliver what it calls “frontier capability without the risk of export controls.” Sakana’s own launch language names Fable and Mythos directly. The pitch is sovereignty: route around any single government’s leash on any single lab by orchestrating across many. Whether or not Fugu’s benchmarks hold up under scrutiny, the positioning is the real story. Export controls aimed at individual frontier models may simply accelerate a shift toward orchestration layers that nobody can export control, because no single model inside the system is doing the controlling.

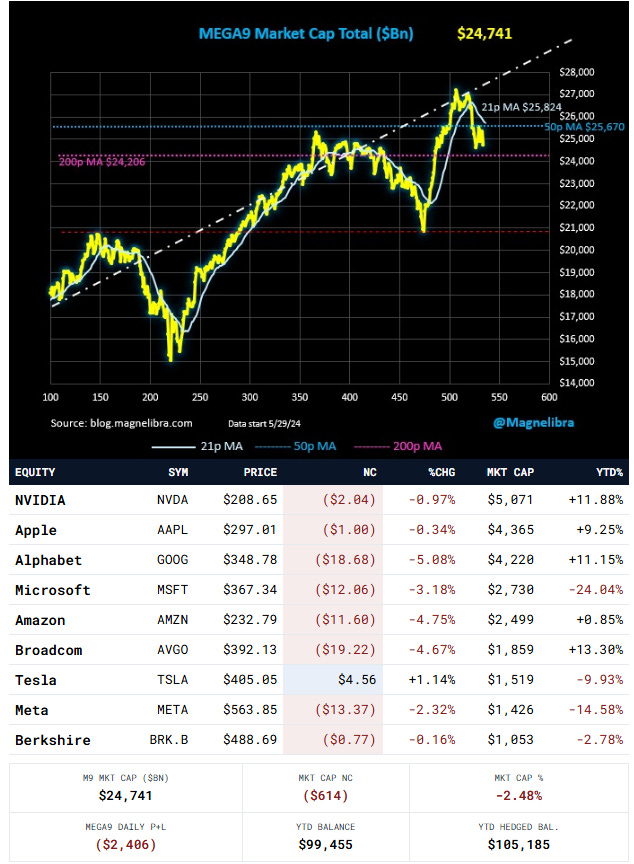

That story sits on top of a capex structure that is starting to look strained on its own terms. The major hyperscalers, Microsoft, Amazon, Alphabet, and Meta, are on track to spend somewhere between $650 and $725 billion combined on AI infrastructure this year, against free cash flow that is compressing across the board: Amazon’s trailing free cash flow down roughly 95 percent, Alphabet’s down 47 percent in a single quarter. A meaningful share of that demand is circular. Nvidia commits $100 billion to OpenAI, which spends it on Nvidia chips. Oracle signs $300 billion with OpenAI for data centers it fills with Nvidia silicon. Nvidia takes a stake in CoreWeave and commits billions to buy CoreWeave’s unsold capacity, capacity built on Nvidia GPUs. Microsoft owns roughly 27 percent of OpenAI and is its primary cloud landlord, recycling Azure revenue into the same chips it sells compute against. Two cash burning customers, OpenAI and Anthropic, now underwrite something like 1.05 trillion of a roughly $2.1 trillion revenue backlog sitting on the books of the four largest cloud providers. None of that is illegal or even unusual for an infrastructure buildout. It is, however, the same shape as the financing daisy chains that defined the back half of the 2000 cycle, and it is showing up exactly where you would expect it to: in the names that built the last three years of index returns.

That shows up directly in our own tracker. Microsoft sits at negative 24.04 percent year to date inside the MEGA9 basket, Meta at negative 14.58, Tesla at negative 9.93, Amazon barely positive at 0.85. These are not the speculative small caps taking the hit. These are four of the largest single commitments inside the basket. Microsoft’s own quarterly capex actually came down even as the OpenAI exclusivity arrangement that anchored its AI narrative came apart, and the market punished both the pullback and the unwind in the same week. Meta raised its 2026 capex guide to a $25 to $145 billion range and lost roughly 10 percent of its market value on the print. Nvidia, Apple, Alphabet, and Broadcom are still carrying the basket positive, up 11.88, 9.25, 11.15, and 13.30 percent respectively, but the dispersion opening up inside what traded as a single momentum block for three years is the real story of this stretch. The market is starting to price hyperscaler capex the way it should have from the start: as a bet with a payback period, not a multiple expansion story.

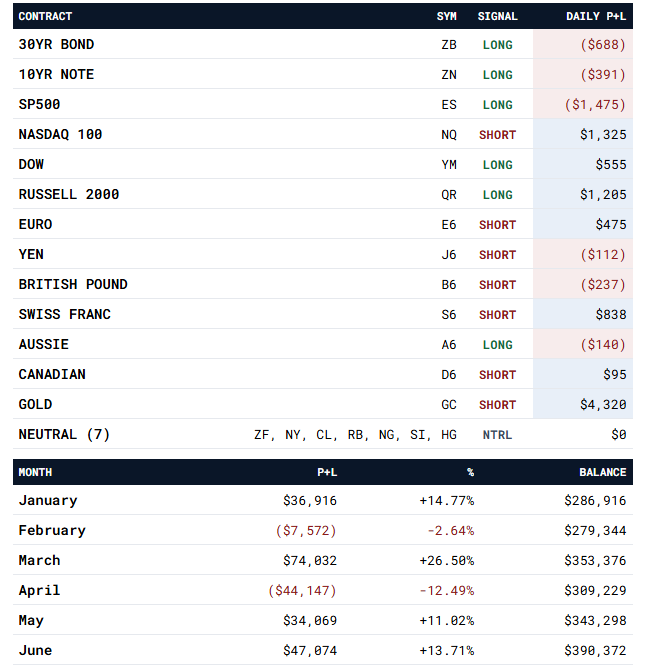

Systematic trend following across financial and commodity futures. Start value $250,000. Daily result $5,769.00 (+1.50%). Year to date, the program is up $140,372, a 56.15% return.

Hypothetical equal weight basket of the nine largest mega cap equities, started at $100,000 dollars. Total basket market cap stands at $24.741 trillion, down 2.48% on the day, slipping back below its 21 and 50 period moving averages of 25.824 trillion and 25.670 trillion while holding above the 200 period average at 24.206 trillion. The hedge overlay, short QQQ calls or long puts depending on the signal against the basket, is carrying a $5,730 dollar year to date advantage over the unhedged tracker, a 5.76 percentage point spread.

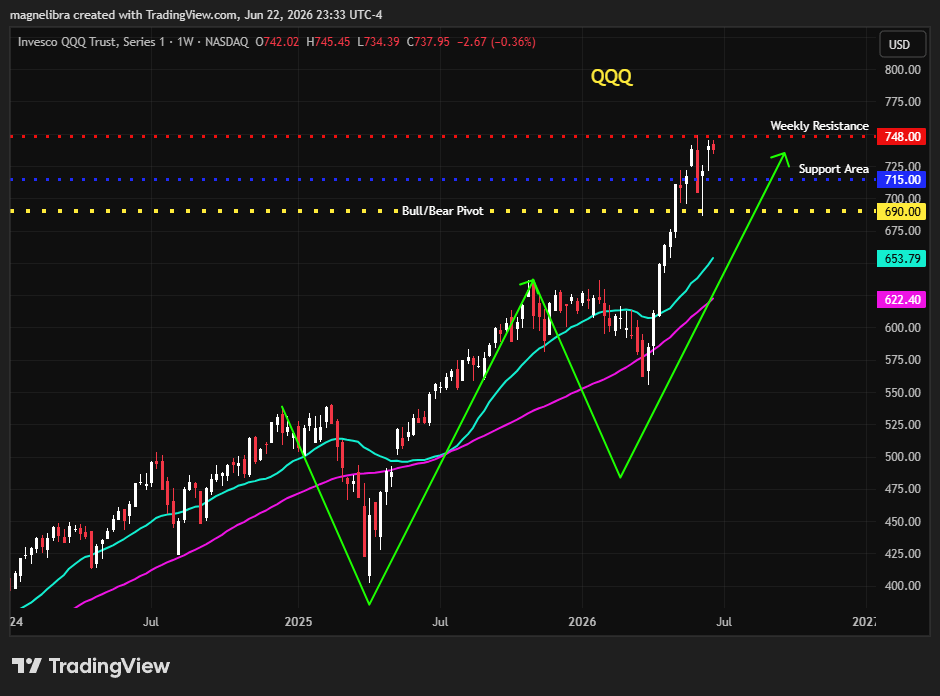

QQQ closed today at 737.95, just below the 748 weekly resistance line that has capped every rally since mid May. Support sits at 715, with the broader bull/bear pivot down at 690. We are working a buy on the 725 put at 3.00 to widen the existing hedge, with the short call side of the structure priced near 6.50 against the 26 June expiry.

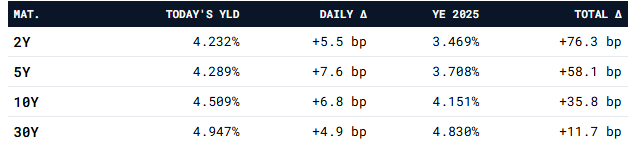

Daily yield change reflects today's settle against yesterday's close. Total change is measured against the December 31, 2025 close. Yields rose across the curve today, two through thirty year, with the front end moving the least on the day and the belly moving the most.

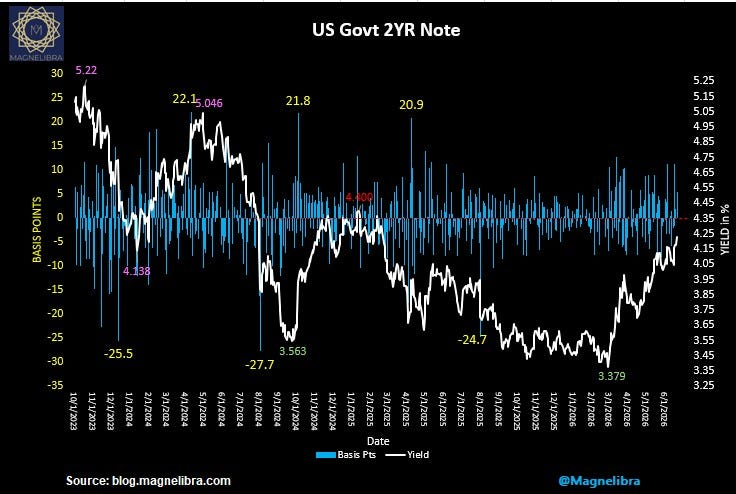

The two year note, the maturity most sensitive to Fed policy, has backed up from a 3.379 low in February to 4.232 today, an 85.3 basis point move that has erased most of last year's easing on its own. That repricing is the bond market doing BofA's work for it before the Fed has hiked a single time.

Look at the 2Y rally, maybe higher rates are helping to offset speculative fervor by giving the private sector more risk free interest income via the US Govt to Private Sector interest transfers?

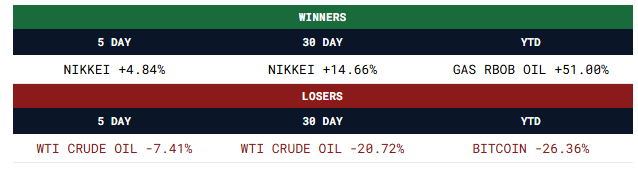

Nasdaq futures shed 66.25 points to 30,653.50, down 1.19 percent today. The contract closed at 30,355.50 on the weekly chart, holding 29,800 support with 31,000 weekly resistance still overhead. Nikkei remains the standout, up 44.80 percent year to date against a Nasdaq up 18.39 and an S&P up 7.84.

The dollar index closed the week at 101.037, up 0.27 percent, clearing the 99.500 bull/bear pivot for the first time since the spring reversal. Bitcoin bounced 734.34 to 63,969.97 on the weekly print but remains pinned under the 70,583 resistance shelf and the 75,651 Strategy Inc average cost basis, with 52,800 the next support level of consequence.

Strategy Inc. spent $335 Million today to lower the BTC dollar cost avg. price by a meager $5!

Nikkei leads on both the 5 day and 30 day windows, up 4.84 and 14.66 percent. WTI crude is the worst performer on both short windows, down 7.41 percent this week and 20.72 percent over the month, even after rallying sharply off its spring low. Bitcoin remains the standout laggard year to date, down 26.36 percent against a basket where most other majors are positive.

Monero led the top 10 digital asset basket today, up 8.29 percent, while Solana added 5.40 and Bitcoin itself gained 2.27 percent to 64,399.69. Zcash was the lone decliner of consequence, off 0.59 percent. The basket’s total market cap stands at 1.716 trillion, up 36.21 billion on the day.

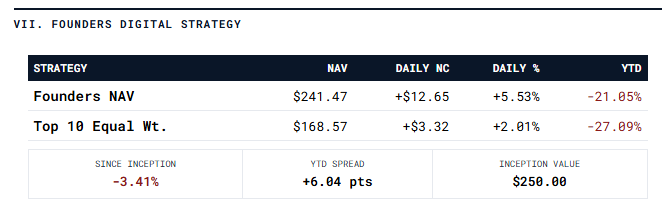

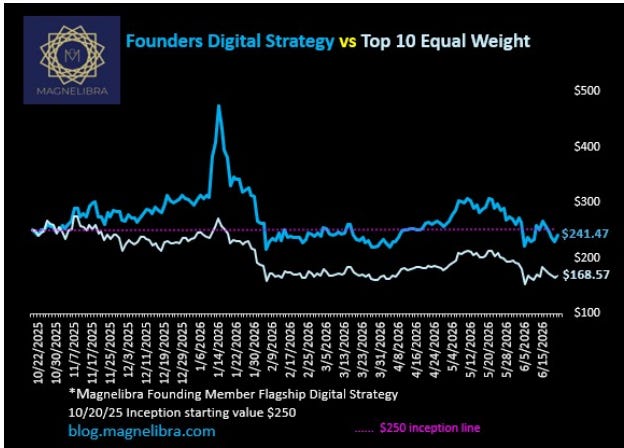

The Founders strategy continues to outperform the passive equal weight basket by a wide margin on a since inception basis, the gap holding above 30 points for most of the past month.

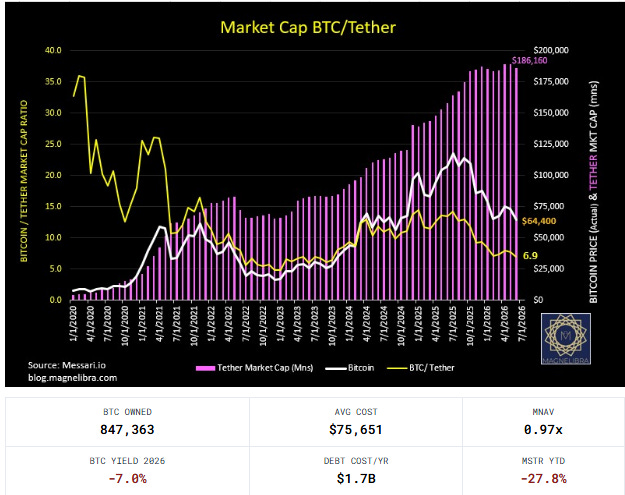

The Bitcoin to Tether market cap ratio has compressed to 6.9, down from a 2025 peak above 23. Tether's own market cap has climbed to 186.16 billion even as Bitcoin's price has stalled, a sign that stablecoin issuance is outpacing the asset it is most commonly used to trade.

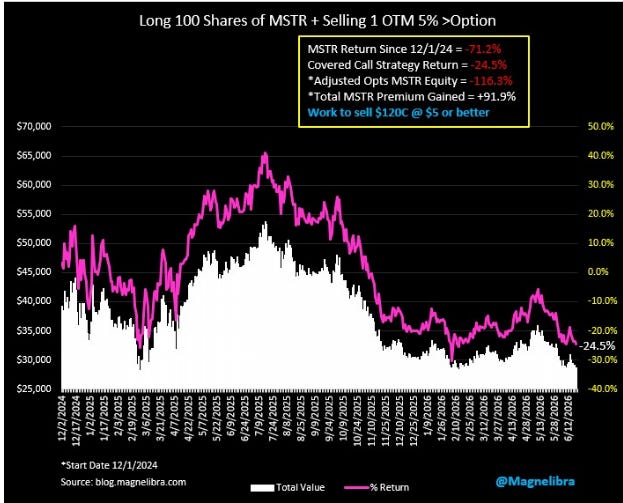

Strategy Inc's covered call overlay, long 100 shares against one out of the money call sold monthly, is sitting at a negative 24.5 percent return since the December 1, 2024 start date, versus negative 71.2 percent for the unhedged shares. Total premium collected since inception now stands at 91.9 percent of the original position value. We are working to sell the 120 strike call for this weeks expiry at 5.00 or better against the position. Selling MSTR down near the $107 area might not be the best idea, so we are expecting the market to test this and hold at first.

Markets have spent five years treating every Fed decision as a binary switch between easing and tightening. The interest income channel does not care which switch is flipped. A government this large, financing itself this short, transmits monetary policy through its own balance sheet as much as through bank lending. Watch the mechanism, not the label on the policy.