Final Stretch of 2023

Tracker updates for Subs

As we come into the final stretch of the year, we wanted to touch on a few of the trends and themes that have transpired in the markets this year. First, we hope that everyone had a wonderful Thanksgiving, enjoyed their time with family or friends. We ourselves took a little break from writing in order to gather our thoughts and contemplate on what the final month might look like for the overall markets. With this in mind let’s hit on a couple of themes that we have seen transpire over this year.

Higher for longer

Banking stress due to higher rates

Inflation, of course inflation

Quantitative Tightening and Reverse Repo

AI Mania

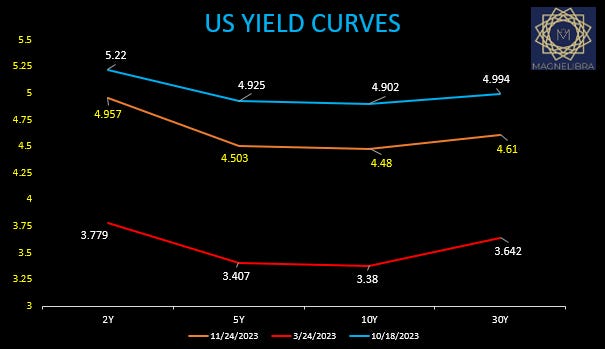

So the global bond markets hopes for a reversal of staunch rate hiking policies out of the Federal Reserve were dashed with each and every FRB meeting this year. Even when the banking stress hit in full stride early on with SVB the market quickly learned the FRB had other ideas in mind. As you can see from our US Rates chart here, the low in yields that came during that March banking stress period are well below today’s rates:

The US govt 2Y has a range of 144 basis points from the March lows to the October highs. We can use these for our parameters going into 2024. During times of stress in the markets we could expect the US Govt 2Y to move toward 4% but remain sticky near the 5% area as long as the FRB continues this higher for longer rhetoric. Honestly we believe they need some longer duration coupons to be above the 4.50% area for 10s and bonds and time will alleviate things and has become one of the FRBs best weapons. That weapon is the uncanny ability to buy “time” decades of it in fact.

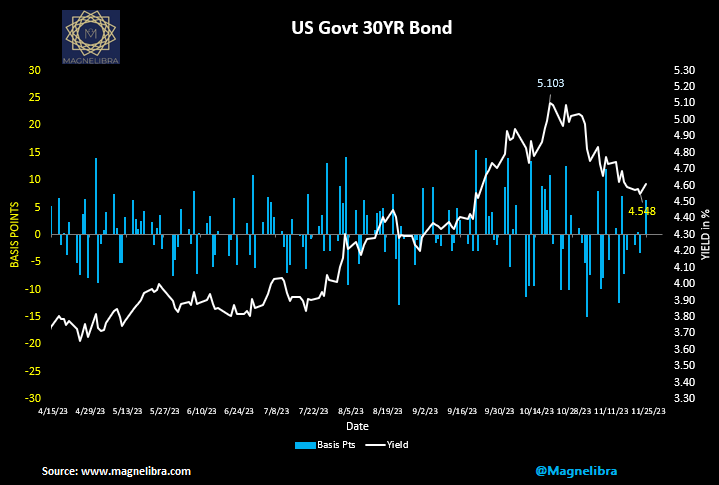

Yes we have had QE and ZIRP for far too long and this has led to the massive dislocations in economic signaling, creating far too much credit and capital well above the needs of an increasing economic upward trajectory. So we are on board with the Higher for Longer theme because we know the truth, there is far too much credit and capital in the markets and equity and Real Estate prices continue to remain sticky on the high end. For now the US bond market has taken back 55 basis points in the long end, dropping from 5.103% down to 4.548% and perhaps we have hit a floor here for now:

These higher rates are destroying the banking sectors ability to extend credit as their balance sheets have become encumbered with securities that are deeply underwater, but held in two forms, Held to Maturity (HTM) and Available for Sale (AFS). Wolfstreet.com posted this chart showing the cumulative unrealized losses held at the commercial banks:

This situation will be alleviated with time, but for now, this is very problematic and its why the FRB created the BTFP program, so that banks can access funding when needed and swap these underwater securities for par with the FRB. This program has been tapped for $113.6 Billion as of the latest H.4 report. We suspect this program will be ongoing and renewed once the expiration date is reached. The banking stress will not be alleviated by these programs but rather prolonged and the FRB cannot extend the higher for longer without the collateral damage to the banking sector.