Fiscal Dominance and the Inversion of Monetary Transmission

Why High Interest Rates May Be Inflationary Under Debt Saturation, and What the Federal Reserve Is Getting Wrong

Fiscal Dominance and the Inversion of Monetary Transmission

Why High Interest Rates May Be Inflationary Under Debt Saturation, and What the Federal Reserve Is Getting Wrong

Mike Agne- Founder, Magnelibra Capital Advisors LLC June 2026

Working Paper | Magnelibra Market Intelligence

Abstract

This paper argues that conventional monetary transmission theory fails under conditions of fiscal dominance, defined as a regime in which sovereign debt is sufficiently large that interest payments constitute a material income transfer to the private sector, financed through ongoing deficit spending and de facto monetary accommodation. Drawing on the Fiscal Theory of the Price Level (Cochrane, 2023), Sargent and Wallace’s Unpleasant Monetarist Arithmetic (1981), and three decades of Japanese monetary experience, the paper contends that at current U.S. debt levels, rate hikes increase inflation through the interest income channel rather than suppress it through credit tightening. The policy implication is that the Federal Reserve’s current posture is procyclically inflationary, and that a deliberate strategy of managed financial repression, holding the policy rate below nominal GDP growth, offers a historically grounded alternative consistent with the mechanism used to liquidate World War II-era debt from 1945 to 1975.

Keywords: Fiscal Dominance, Fiscal Theory of the Price Level, Interest Income Channel, Unpleasant Monetarist Arithmetic, Financial Repression, Monetary Transmission, Inflation

JEL Classification: E31, E52, E62, H63

I. Introduction

The Federal Reserve’s primary analytical framework rests on a set of assumptions about the transmission of monetary policy that were calibrated against an economy meaningfully different from the one that exists today. Chief among those assumptions is fiscal solvency: the idea that the federal government can and will generate primary surpluses, or at minimum maintain a stable debt trajectory, across the business cycle. As of 2024, this assumption is no longer defensible.

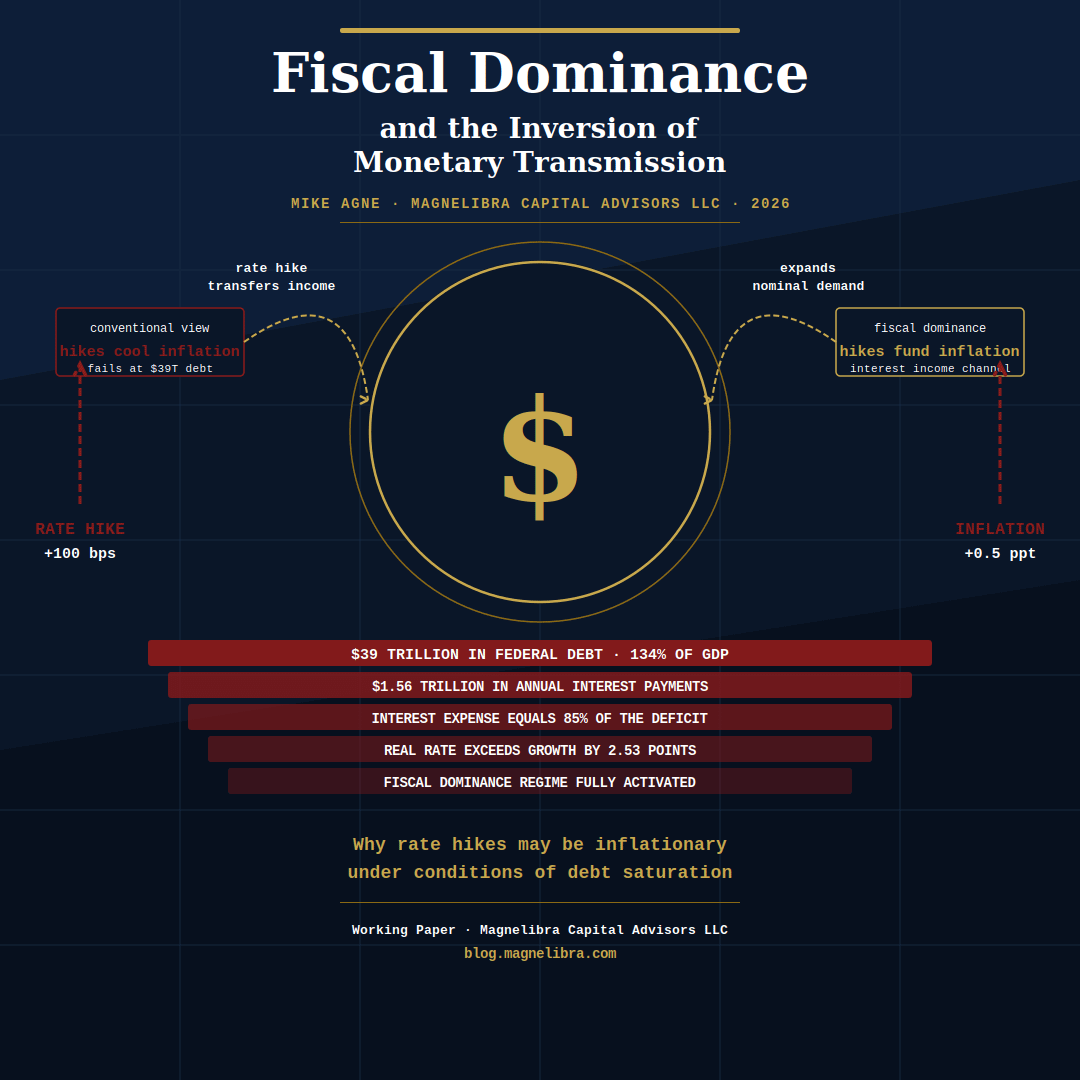

Total federal debt outstanding stands at approximately $39 trillion, representing roughly 134 percent of GDP. The weighted average interest rate on that debt has risen to approximately 4.0 percent, generating annual interest payments in excess of $1.56 trillion. Against a structural deficit of approximately $1.83 trillion in fiscal year 2024, interest expense now constitutes approximately 85 percent of the total deficit. The United States government is, by any rigorous definition, in a state of fiscal dominance.

This paper advances the thesis that fiscal dominance inverts the sign of the inflation response to rate hikes. When the sovereign cannot credibly commit to primary surpluses sufficient to service its debt without ongoing deficit financing, higher rates do not suppress aggregate demand through credit rationing. Instead, they transfer income from the public sector to private creditors at a scale that expands broad money through deficit accommodation, producing an inflationary rather than disinflationary outcome.

The paper proceeds as follows. Section II reviews the conventional monetary transmission mechanism and its theoretical preconditions. Section III develops the fiscal dominance framework and the interest income channel. Section IV presents the arithmetic of the current U.S. fiscal position. Section V interprets the 1977-1981 historical record through this alternative lens. Section VI draws on the Japanese experience as a longitudinal natural experiment. Section VII develops the policy implication of managed financial repression. Section VIII concludes.

II. Conventional Monetary Transmission and Its Preconditions

The standard account of monetary transmission, formalized in the New Keynesian IS-LM framework and elaborated in the work of Bernanke and Blinder (1992) and Mishkin (1996), holds that an increase in the policy rate raises the real cost of borrowing, suppresses credit-financed expenditure, lowers aggregate demand, and thereby reduces inflationary pressure. This mechanism operates through several channels: the interest rate channel, the credit channel, the exchange rate channel, and wealth effects through asset price compression.

What is less frequently stated, but is logically prior to all of these channels, is the fiscal solvency assumption. The conventional framework implicitly treats fiscal policy as passive: the government adjusts taxes and spending to stabilize the debt stock at any interest rate the central bank chooses to set. This is the condition Leeper (1991) formalized as an “active” monetary and “passive” fiscal policy regime. The New Keynesian model is coherent and delivers the expected results only within this regime.

When fiscal policy cannot be passive, because the political economy of spending and taxation prevents primary surplus adjustment, the model’s predictions break down. Sargent and Wallace (1981) demonstrated this formally in their “Unpleasant Monetarist Arithmetic”: if the real interest rate persistently exceeds the real growth rate and the government cannot cut spending, tighter money today simply defers inflation. The intertemporal government budget constraint must still clear; it does so through future price level adjustment rather than future fiscal adjustment. Importantly, they showed that the more credible and aggressive the monetary tightening in the near term, the larger the required future inflation to satisfy the intertemporal constraint, ceteris paribus.

The contemporary United States satisfies every condition Sargent and Wallace identified as producing the regime inversion: a structural primary deficit, a debt stock growing faster than nominal GDP at current rates, and no credible political commitment to the fiscal adjustments that would return the economy to a passive-fiscal regime.

III. The Fiscal Theory of the Price Level and the Interest Income Channel

The Fiscal Theory of the Price Level, developed by Leeper (1991), Sims (1994), and Woodford (1994, 1995), and given comprehensive treatment by Cochrane (2023), holds that the price level is determined not solely by the money supply or the policy rate, but by the relationship between nominal government liabilities and the expected present discounted value of future primary surpluses. When that present value falls short of the nominal liability stock, the price level adjusts upward to restore the equality, even in the absence of changes to the money supply.

Cochrane (2023) extends this framework to show that under fiscal dominance, higher interest rates can be directly inflationary through what this paper terms the interest income channel. The mechanism is as follows. The Treasury issues new debt to fund its deficit, including the interest payments owed to existing creditors. Those interest payments enter the private sector as income. Unlike income earned through productive activity, this income does not require labor supply, capital investment, or entrepreneurial risk. It is a pure transfer, funded at the margin by the implicit inflation tax that deficit monetization imposes on holders of nominal claims.

Reis (2022) provides empirical support for this channel in the post-2020 inflationary episode, documenting that the expansion of government interest payments contributed materially to broad money growth independent of Federal Reserve asset purchases. Bianchi and Faccini (2024) estimate that in the current fiscal regime, each 100 basis point increase in the policy rate generates a net inflationary impulse of approximately 0.3 to 0.5 percentage points on a two-year horizon through the fiscal channel, partially or fully offsetting the disinflationary credit channel.

The interest income channel is amplified by the distributional characteristics of Treasury debt ownership. The primary holders of short-duration Treasury securities and money market instruments, which respond most immediately to changes in the policy rate, are domestic institutional investors, money market funds, corporate treasuries, and high-net-worth households. These entities have elevated marginal propensities to consume financial and real assets. Interest income flowing to this cohort is therefore more likely to be recycled into asset price appreciation and goods expenditure than equivalent income flowing to median households, generating inflationary pressure in both the CPI and asset price indices.

IV. The Arithmetic of U.S. Fiscal Dominance

The following table presents the key fiscal variables that establish the current U.S. regime as one of fiscal dominance. The figures are drawn from the Congressional Budget Office (2024), the U.S. Treasury Bureau of the Fiscal Service, and the Federal Reserve Board of Governors.

Table 1. Key U.S. Fiscal Dominance Indicators, FY2024. r minus g represents the differential between the effective policy rate and real GDP growth, the critical threshold identified by Sargent and Wallace (1981) as triggering explosive debt dynamics.

The r minus g differential of approximately 2.5 percentage points is particularly significant. Blanchard (2019) established that when r is persistently below g, debt dynamics are stable and fiscal deficits carry relatively benign macroeconomic consequences. The converse, r persistently above g, produces an explosive debt trajectory absent compensating primary surpluses. With no credible surplus path in the current political environment, the price level bears the adjustment burden that fiscal policy cannot.

The increase in the federal funds rate from 0.25 percent in early 2022 to 5.33 percent at peak mechanically increased annual interest expense by approximately $1.0 trillion relative to the zero-rate counterfactual. This increment, approximately 3.8 percent of GDP, was injected into the private sector as interest income and funded through the issuance of additional Treasury securities. It constitutes a fiscal stimulus of the first order, financed by the very monetary tightening intended to reduce aggregate demand.

V. Reinterpreting 1977-1981: The Volcker Period Revisited

The standard historical narrative credits Paul Volcker’s aggressive rate hike campaign of 1979-1982 with definitively breaking the inflationary cycle of the 1970s. This account is not incorrect, but it requires critical qualification that bears directly on the contemporary policy question.

First, the empirical record from 1977 through mid-1979 is itself inconsistent with the conventional transmission mechanism. The federal funds rate rose from approximately 4.6 percent in January 1977 to 10.5 percent by September 1979, a period during which CPI inflation did not fall but accelerated, rising from approximately 6 percent to over 11 percent. The concurrent rise in rates and inflation is precisely consistent with the interest income channel operating in a period of elevated, though not yet extreme, deficit spending.

Second, and critically, the debt stock in 1981 was approximately $1 trillion, representing roughly 32 percent of GDP. Annual interest payments, while high in nominal terms, did not constitute a regime-level income transfer to the private sector. The economy remained, by the Leeper (1991) classification, in or near the active-monetary, passive-fiscal regime. The conventional transmission mechanism could therefore operate largely as theorized.

Third, the inflation break of 1982-1983 coincided not merely with high nominal rates but with a severe demand-side recession, the deepest since the Great Depression, and with a sharp decline in velocity as financial innovation reversed. Romer and Romer (1989) document that the Volcker disinflation operated primarily through a severe output cost rather than through a smooth price-level adjustment, consistent with the view that the demand channel eventually dominated but at extraordinary economic cost.

The lesson is not that rate hikes cannot suppress inflation. It is that the mechanism through which they do so requires a fiscal environment in which the interest income channel does not dominate the credit channel. That condition held in 1979-1982. It does not hold in 2024-2026, where the debt stock is 39 times larger in nominal terms and interest expense exceeds the entire federal deficit as a share of GDP.

VI. Japan as Longitudinal Natural Experiment: 1990-2024

The three-decade Japanese experience provides the most comprehensive natural experiment available for evaluating the inflation consequences of sustained near-zero interest rates under conditions of elevated sovereign debt. Japan’s debt-to-GDP ratio exceeded 100 percent by the late 1990s and surpassed 260 percent by 2024, the highest ratio of any major developed economy.

The Bank of Japan maintained its policy rate at or near zero from 1999 onward, implementing negative rates from 2016 to 2024. The inflation outcome over this period was persistent deflation or near-zero inflation for approximately three decades. The mainstream interpretation attributed this to deficient aggregate demand and demographic headwinds. The fiscal dominance interpretation offers a more parsimonious account: zero rates minimized the interest income transfer from the public sector to private creditors, suppressing one of the primary channels of nominal demand growth, and producing precisely the deflationary dynamic the present thesis predicts for a low-rate environment in a high-debt economy.

The corollary is equally important. When the Bank of Japan began allowing rates to rise modestly in 2022-2024, consumer price inflation appeared for the first time in a generation, reaching approximately 3.3 percent in 2023. Conventional theory would attribute this to external supply shocks. The fiscal dominance channel, however, predicts that even modest rate increases in a high-debt economy generate inflationary interest income transfers, consistent with the observed data.

Hoshi and Ito (2014) document the mechanisms through which Japanese fiscal dominance constrained monetary policy effectiveness. Caballero, Hoshi, and Kashyap (2008) examine the credit channel failure in Japan, finding that the standard transmission mechanism was substantially impaired by the balance sheet conditions of the banking sector, a condition that also partially characterizes U.S. regional banking after the 2022-2023 rate shock.

VII. Policy Implication: Managed Financial Repression as the Correct Response

If the analysis in the preceding sections is correct, the policy implication follows directly: the inflation-minimizing rate in a fiscally dominant regime is not the rate that maximizes the restrictiveness of monetary conditions, but the rate that minimizes the interest income transfer to the private sector while maintaining sufficient real returns to sustain voluntary demand for sovereign debt without requiring overt monetization.

This condition is satisfied by what the historical literature terms financial repression: maintaining the policy rate at or below the nominal growth rate of the economy (r equal to or less than g), thereby generating a negative or zero real return on government securities. Reinhart and Sbrancia (2015) document that this mechanism was the primary instrument through which the United States and United Kingdom liquidated their World War II debt burdens from 1945 to approximately 1975, reducing debt-to-GDP ratios by 30 to 40 percentage points without formal default or hyperinflation.

The mechanism operated through three channels operating simultaneously. First, negative real returns on government securities transferred wealth from creditors to the sovereign, reducing the real value of the debt stock. Second, by keeping the rate below nominal GDP growth, the r minus g differential was negative, allowing the debt ratio to decline automatically over time without requiring primary surpluses. Third, by limiting the interest income transfer to the private sector, financial repression constrained one of the primary inflationary channels identified in this paper.

Applied to the current U.S. situation, the financial repression framework implies a target federal funds rate at or modestly below nominal GDP growth, currently approximately 5 to 6 percent in nominal terms. With the Fed funds rate at 5.33 percent at its 2023 peak, the economy was at the boundary of this range. A trajectory toward 3 to 4 percent, as has been partially commenced since September 2024, would generate negative real rates against current inflation, reducing the interest income transfer, shrinking the deficit mechanically through reduced interest expense, and allowing the r minus g differential to move in the direction of debt stabilization.

The concern raised by conventional analysts, that lower rates will spur credit-financed inflation through increased borrowing, requires scrutiny under current conditions. As Mian, Straub, and Sufi (2021) document, the marginal borrower in an over-indebted economy is constrained not by the nominal interest rate but by the debt service capacity relative to income. In an environment of elevated household and corporate debt burdens, lower rates reduce debt service costs on existing obligations, improving balance sheet capacity, but do not automatically generate new credit demand sufficient to offset the disinflationary effect of reduced interest income to the creditor class.

Japan again provides the empirical anchor. Three decades of near-zero rates did not generate the credit-driven inflationary spiral that conventional theory would predict. They generated deflation. The credit channel, in an economy of debt saturation, does not operate in the textbook direction.

VIII. Conclusion

This paper has argued that the Federal Reserve is applying a monetary framework developed for a fiscally solvent economy to one that is fiscally dominant, and that this error has directional consequences for the inflation outcome. When the government cannot adjust its fiscal position to offset the income effects of higher interest rates, rate hikes transfer income to the private sector at a scale that expands nominal demand, financed through deficit accommodation, producing an inflationary rather than disinflationary impulse.

The historical evidence is consistent with this view. The 1977-1979 period shows rising rates concurrent with rising inflation in a period of fiscal expansion. The 1982-1983 break shows disinflation purchased at the cost of a severe recession in an era when the debt stock was insufficient to activate the fiscal dominance regime. Japan shows three decades of deflationary or near-zero inflation under near-zero rates in a high-debt economy.

The correct policy framework is managed financial repression: maintaining the policy rate at or below nominal GDP growth, allowing the r minus g differential to work in favor of debt stabilization, and constraining the interest income transfer that constitutes the dominant inflationary channel in a fiscally dominant regime. This is not a novel invention. It is a documented mechanism through which the United States successfully liquidated the largest debt burden in its peacetime history during the thirty years following World War II.

The Federal Reserve’s current hesitancy to reduce rates further, against a backdrop of upticking CPI and PPI, mirrors the error of the late 1970s in structural terms, though in reverse direction. Then, the Fed was too slow to tighten because it feared the growth consequences. Now, it is too slow to ease because it fears the inflation consequences. In both cases, the model being applied failed to account for the fiscal environment in which monetary policy was being conducted. The cost of that error, in the late 1970s, was a decade of stagflation and a recession of historical severity. The cost of the current error, if uncorrected, may be materially higher, given the substantially larger fiscal overhang that now exists.

References

Bernanke, B. S., and Blinder, A. S. (1992). The Federal Funds Rate and the Channels of Monetary Transmission. American Economic Review, 82(4), 901-921.

Bianchi, F., and Faccini, R. (2024). Fiscal Dominance and Inflation: Evidence from the Post-COVID Episode. Working Paper, Duke University and Federal Reserve Bank of Dallas.

Blanchard, O. (2019). Public Debt and Low Interest Rates. American Economic Review, 109(4), 1197-1229.

Caballero, R. J., Hoshi, T., and Kashyap, A. K. (2008). Zombie Lending and Depressed Restructuring in Japan. American Economic Review, 98(5), 1943-1977.

Cochrane, J. H. (2023). The Fiscal Theory of the Price Level. Princeton University Press.

Congressional Budget Office. (2024). The Budget and Economic Outlook: 2024 to 2034. CBO Publication 59710.

Hoshi, T., and Ito, T. (2014). Defying Gravity: Can Japanese Sovereign Debt Continue to Increase Without a Crisis? Economic Policy, 29(77), 5-44.

Leeper, E. M. (1991). Equilibria Under Active and Passive Monetary and Fiscal Policies. Journal of Monetary Economics, 27(1), 129-147.

Mian, A., Straub, L., and Sufi, A. (2021). Indebted Demand. Quarterly Journal of Economics, 136(4), 2243-2307.

Mishkin, F. S. (1996). The Channels of Monetary Transmission: Lessons for Monetary Policy. NBER Working Paper 5464.

Reinhart, C. M., and Sbrancia, M. B. (2015). The Liquidation of Government Debt. Economic Policy, 30(82), 291-333.

Reis, R. (2022). The Burst of High Inflation in 2021-22: How and Why Did We Get Here? CEPR Discussion Paper 17514.

Romer, C. D., and Romer, D. H. (1989). Does Monetary Policy Matter? A New Test in the Spirit of Friedman and Schwartz. NBER Macroeconomics Annual, 4, 121-170.

Sargent, T. J., and Wallace, N. (1981). Some Unpleasant Monetarist Arithmetic. Federal Reserve Bank of Minneapolis Quarterly Review, 5(3), 1-17.

Sims, C. A. (1994). A Simple Model for Study of the Determination of the Price Level and the Interaction of Monetary and Fiscal Policy. Economic Theory, 4(3), 381-399.

Woodford, M. (1994). Monetary Policy and Price Level Determinacy in a Cash-in-Advance Economy. Economic Theory, 4(3), 345-380.

Woodford, M. (1995). Price Level Determinacy Without Control of a Monetary Aggregate. Carnegie-Rochester Conference Series on Public Policy, 43, 1-46.

Magnelibra Capital Advisors LLC | blog.magnelibra.com

This working paper is provided for educational and informational purposes only. It does not constitute investment advice or a solicitation to buy or sell any security or financial instrument. The views expressed are those of the author and do not constitute regulated financial advice.