FOMC 75BP and More to Come

Inflation is Enemy #1

We have a lot to cover and we want to first admit how wrong we were to even think the FED was going to waffle to market sentiments for mercy! Ok we are humble enough to admit that even we felt the FED would cave a little, at least give us the 75bp but put a little more emphasis on time lag and future data. They did at least toss that verbiage in the statement, stating:

In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. -FOMC Statement 11/2/2022

So at least we got that part right and who knows, it seems for now Powell & Co. are dead set on hiking at a pace never seen before, and just to put this into perspective we conjured up this chart for you:

Basically the SP500 right now is down a standard bear market 20%, we have to admit, we do expect a further 32% decline given the veracity and the obvious intent on jacking rates up so that they can continue to provide a health stealth bailout, a preemptive monetary gift to all those Tri Party Repo counterparties. In fact here is how the RevRepo will look now, some $235.4 Million per day:

Let’s add the $378 million a day for Excess Reserves and you can see we are talking about some serious free money getting handed out. Our take is this $500 to $600 million is used to backstop the onslaught of MBS and C&I fails and write downs to come. We know housing is next, we know 7% interest rates have a 12 mos lag and we would expect massive layoffs out of the industry as well as heavy supply to sit on the market. In fact we saw this headline today:

Now we know bear markets are just the beginning of a larger correction process. In fact when we look back to 2008/2009 we can see how the buy and hope mentality works until it doesn’t. As the SP500 initially dropped 20% then spent 2 months grinding higher, to only see it lose 53% over the next 9 months:

We know now that valuations are a function of supply/demand for monetization, meaning everyone can’t sell at the same time and depending on the liquidity of things, well, that makes it all that much worse. In fact we would suspect today’s algorithm dominated markets will exacerbate moves like this even more so. Everything now is driven by balance sheet, access to LOCredits, etc. because this entire system is built on leverage. So let’s go back to what changed the market direction post decision and why the markets reversed their initial higher move off the FOMC decision and it came in the QnA session:

*POWELL: IF WE OVERTIGHTEN, WE CAN SUPPORT ECONOMIC ACTIVITY

*POWELL: IF WE UNDERTIGHTEN, RISK IS INFLATION ENTRENCHED

Basically in a nutshell he is clearly stating we will overtighten and will reduce inflation because even for them 8% CPI is not something they want becoming main stream and accepted. Inflation is as much as a mindset as it is a DC phenomenon. Remember only Washington can create inflation, they print money, they are responsible for inflating, period.

Ok so now we know the FED will continue for the next few months what does it all mean?

Equities will continue to see heavy offers on any buy programs that come in and will continue to see downside probes.

Yield curve will invert at the US Govt 10Y /Fed Funds level and this will murder a lot of over levered naked swimmers as the tide of free carry turns negative. Here is what it will look like after December 2022 if US Govt 10Y yields stays near 4%:

RevRepo (investment banks and large funds) will continue to be supported via IOER and RRP operations and this will alleviate some of the future economic chaos that is coming.

With financial disruption comes global instability and we already know this is the case given Ukraine and now North Korea stepping things up.

We know the buy and hope crowd has been conditioned for many decades, but that is over, once the inflation genie is out of the bottle, the central bank knows it has to flatten it at ALL COSTS or risk it becoming accepted at that higher rate. If an economy starts to accept a higher inflation rate then the central bank becomes impotent in squashing those expectations. Which is why we think Powell & Co. have become so hawkish, certainly not by choice or nature, but by force. A great chart from Zhedge clearly outlines the expectations of the buy and hope crowd each and every time over the last few meetings, to only be squashed:

As far as breaking down further equity wise, seems like Tech is done, and the rotation out has clearly taken a toll and this proxy of ours path of least resistance is lower as the 4 year channel support has now been broken:

The SP500 vs Nasdaq futures chart is confirming this continued rotation as well:

Looking back at the FOMC decision time, the markets did initially take the decision in stride as both equities and bonds started trading higher, but the QnA all but destroyed that, here was the action in the Nasdaq Future jumping nearly 200 points then proceeding to lose 500 points from the highs:

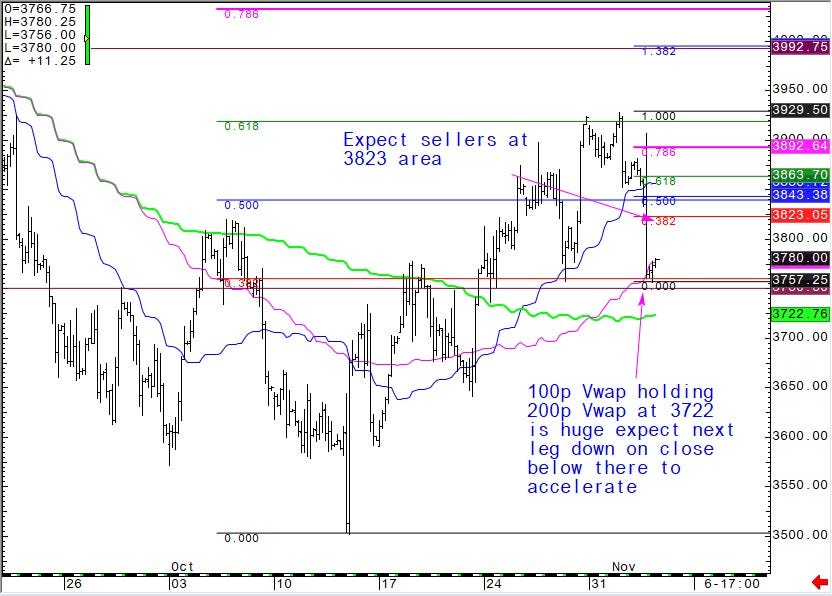

As far as now, technically charts are heavy and we feel rallies will be sold into. In the SP futures we have 3823/3863/3929 upside keys with below 3750 bringing the pain and a close below 3722 should take out that 3550 area:

In the Nasdaq futures 10919 is huge and 11278 will see selling:

As far as the U.S. bond market it held up pretty well overall considering but we would suspect this move was already built in, but it seems for now its in a sideways basing pattern, awaiting the next CPI for its directional bias.

Ok this was long, sorry but important, we hope you learned something today, till next time..

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Econemotions covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2022