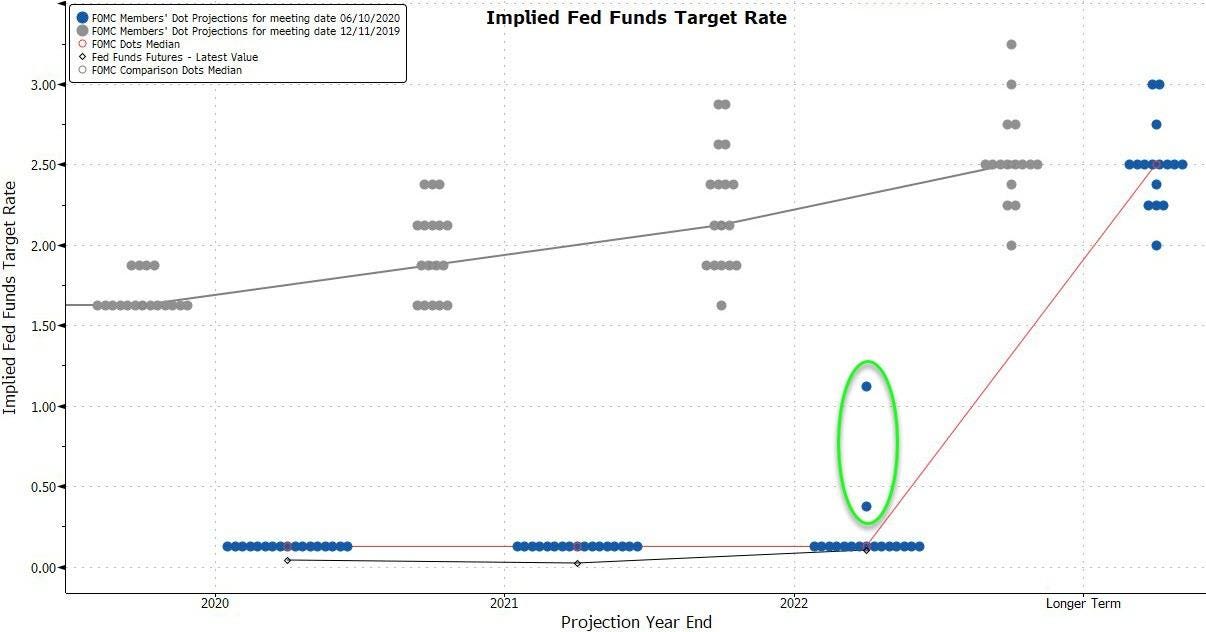

FOMC Plans on Long Term Low Rates

Daily Settlements and Comment

For the first time in our history of following the Federal Reserve we have to say today’s remarks, today’s dot plot was a real life tried and true honest assessment of where interest rates should be over the next few years. For the first time the FED has admitted that rates over the next 2 years will be pegged to the zero bound, now all this follows the clear monetary printing admission that Powell did on 60 Minutes.

This Dot Plot proves our point on transparency and honesty, look at the 2019 predictions in gray, see how far from reality they were:

What has gotten into the FED?

Why the blatant transparency now?

We suppose the FED is dead serious on their “ALL IN” mantra and we get it now, we get that all the tools in the toolkit are being wielded with such expediency and perhaps in some regard trepidation, but for all intents and purposes this is not the old FED. This seems like a FED that is working not autonomously but rather at the discretion of the US Treasury and that is certainly a very new thing.

Whether or not the US Treasury is indeed now in full control, we are certainly in uncharted territory and whether or not all these new monetary facilities will work as intended is still yet to be determined. One thing we are certain is that the Nasdaq has definitely gotten the risk on message, the other indexes, well not so much.

Just when the FED was earning some street cred on honesty, Powell dropped this little nugget of falsehood during the Q&A which @HedgeyeDDale captured in his tweet:

QE and monetary policy are indeed the number one cause of inequality and if you disagree, well think about this, who owns all the assets? That’s right the top 20% own all the assets. Yea they can print money hand it out to the commoner, they can spend it, pay their bills, buy something, but in the end it ultimately ends up in the bank. In the end it ultimately goes to the rentiers. It is how the system was designed, so when Powell says things like this, he is lying, he knows the truth, he is the arbiter of monetary policy and he knows exactly where it flows!

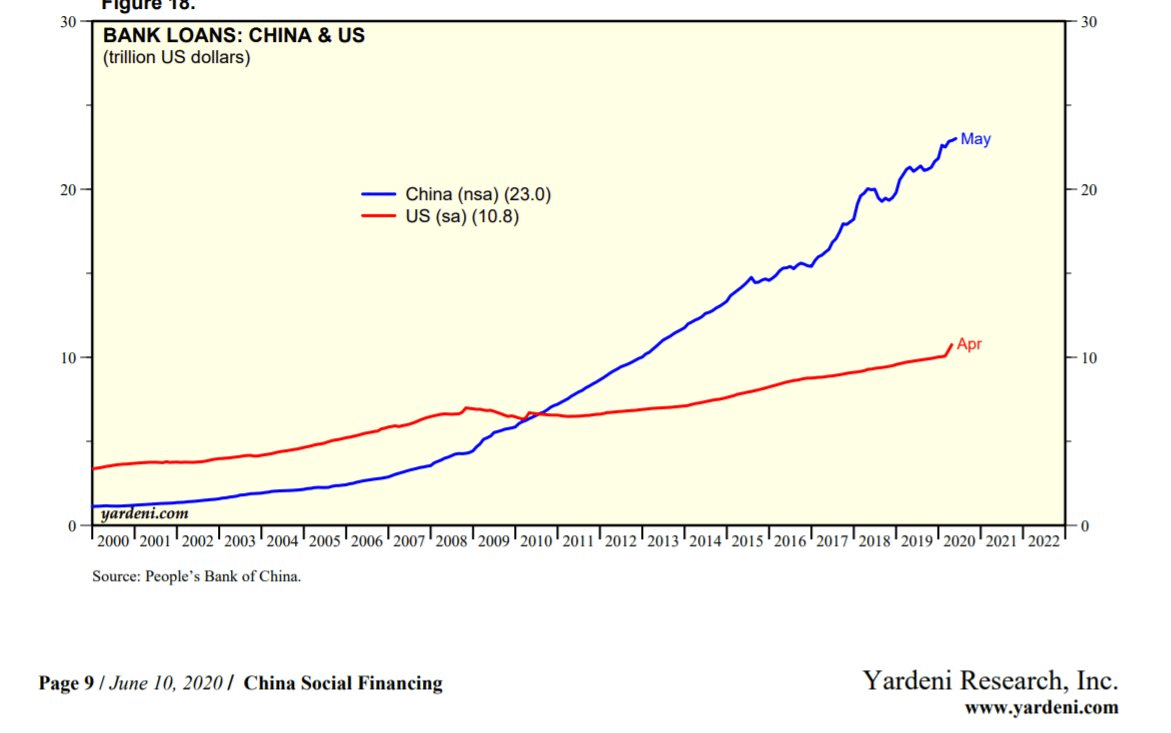

Speaking of flows, and for all those in the camp that the US Dollar is going to fail because of all this printing, well #China and their banks have been in credit overdrive and nothing expands money faster than credit and loans, check this excellent graphic from Yardeni Research out and for those that think China can sell its treasuries, well yea, good luck with that:

OK so how did the markets react? The equities rallied, but they fizzled into the close and have continued lower in early Asia session. Will the FED day change the equity mojo? It seems that way for now, but European and NY session could easily change all that:

The June SP500 .786 level was the 3135 area and that would be our first support down here and that is a very important level for bulls to sustain, will they? We are about to find out.

The Nasdaq is also taking a rare dip lower here:

The US Dollar weakened a bit today as the foreign currencies have been on a decent run here as the Euro and Suisse march up into the 114 and 106 handles respectively. Gold and Silver not much of a reaction but this news of long term ZIRP should put a decent floor in the complex. Finally bonds have come to life here the last few days and after a quick rise in US 30Y yields up to 1.76% they are now back below the 1.50% level. If stocks do turn and roll, we would expect US Treasuries to be a big beneficiary.

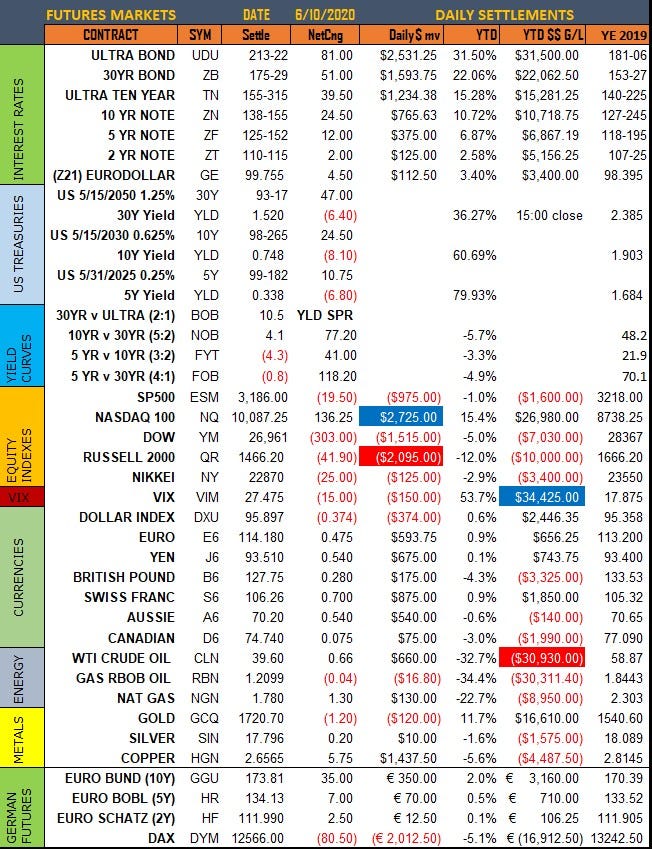

So on to the settlements picture of the markets Magnelibra follows and we thank you for following our letter and we hope we provoke you to think outside the box and induce you to look deeper into your own trading and investing:

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.