FOMC Update

GFBP Tracker Position Update

We added a Nasdaq hedge to the GFBP Tracker for our subscribers which we touch upon later in the note.

Considering the recent inflation data (today’s PPI -0.3% exp -0.1% mom) we would suspect the FOMC to deliver their expected “SKIP.” We will await the pressor for any actual changes to their dot plots or trajectories but given the recent global central bank pauses then hikes, we suspect a new central bank theme has emerged. We touched upon this change a few updates ago and the long standing precedent of one cycle giving away to reversing the prior hike/cut cycle is over.

We believe this is the proper way as data dependency and dynamic adjusting is a proper way to view monetary policy only if central banks are trusted in their ability to actually set a firm policy and not waiver.

Right now there is too much complacency in the global investment community relying upon continued QE, continued expansion of the money supply and liquidity. Magnelibra has a proprietary liquidity tool that we developed and right now that excess liquidity is sitting right at $1.7T. If we see the RRP start to fall below or get closer to that number then we will see how the US equity markets react, we saw the RRP drop $50Bn yesterday to $2,074Bn. Today’s number is not out yet…Actually it is $2,109 so RRP rose $35Bn!

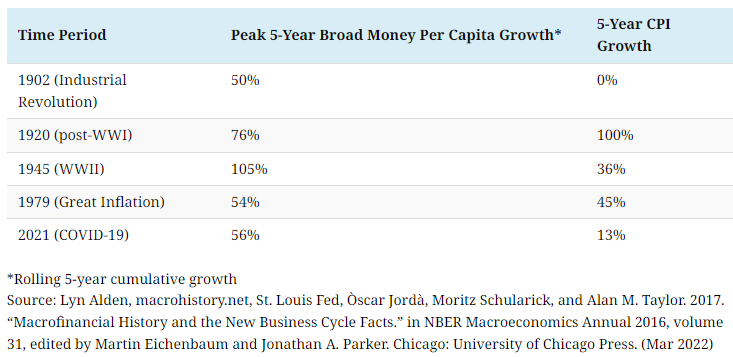

We saw this chart from Lyn Alden and you can see how excessive broad money growth increases CPI considerably. In fact if we used the 1979 CPI calculation we are certain that we would be more than double the stated 13% CPI below:

This isn’t 1979 however and we know this because we are certain we won’t see J Powell holding a stogie while answering to congress!

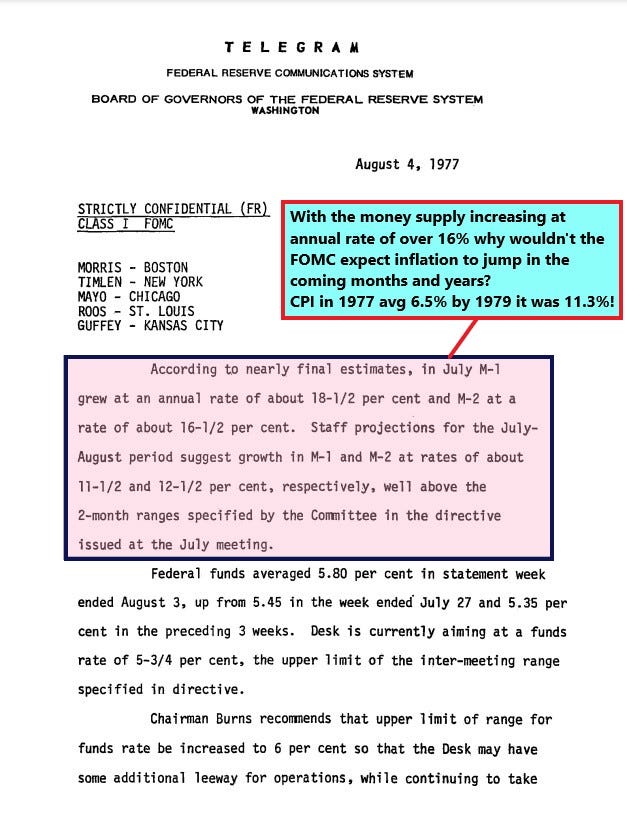

He looks tired doesn’t he, well can you imagine dealing with 500 basis point Federal Funds rate ranges! This is what they had to deal with and Burns dropped the ball as this now released telegram from the FRB 1977 shows, M2 exploding and Burns keeping rates nearly 1100 basis points below M2 growth! (M2 16.5% - 6% Fed Funds)

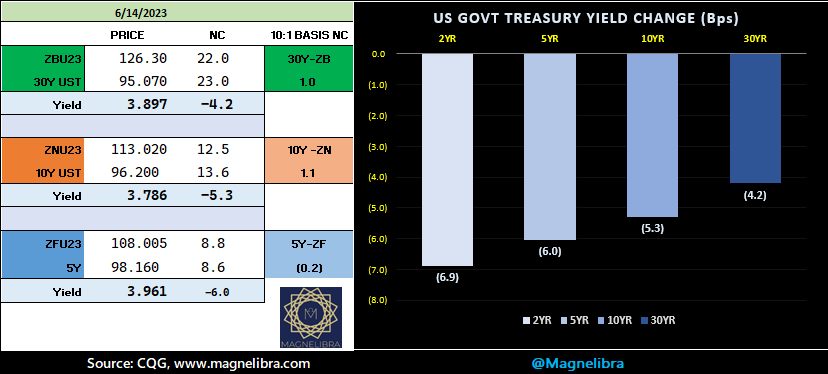

As far as the market today, early bond players have scooped up yesterday’s weakness a little and steepening the curve a bit:

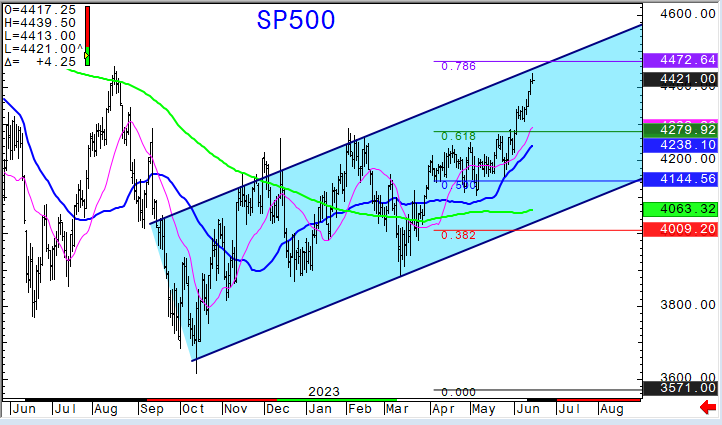

Equities are a bit muted but one look at this SP chart and we can say, this is probably not a good place to set longs into an FOMC meeting!

***GFBP TRACKER UPDATE***

With this chart in mind you will see the addition of +2 Nasdaq Week 3 15100 puts paying 115 to hedge some of the long equity exposure in the GFBP Model Tracker. We are keeping the rest of the tracker positions as of the update yesterday.

As far as that SP chart we suspect that major players use days like FOMC to exit positions and force some people both up and down, so we expect volatility. Longer term as many long time readers know we will be looking for any hint of a rate pause, not just a skip because its rate cuts that will bring equities down eventually!

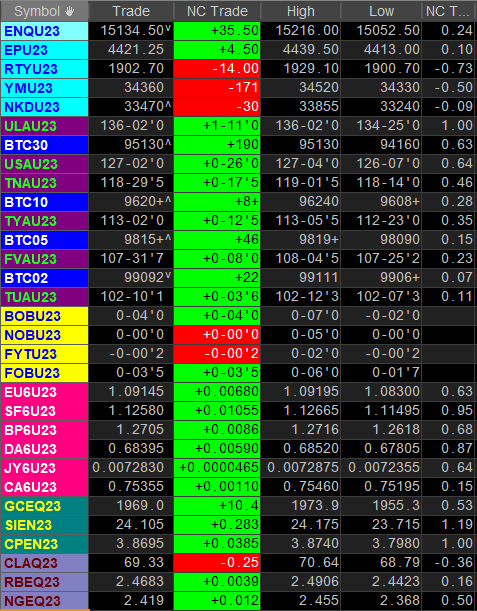

Ok here is the overall markets we follow pre FOMC, good luck today:

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023