FOMC Week

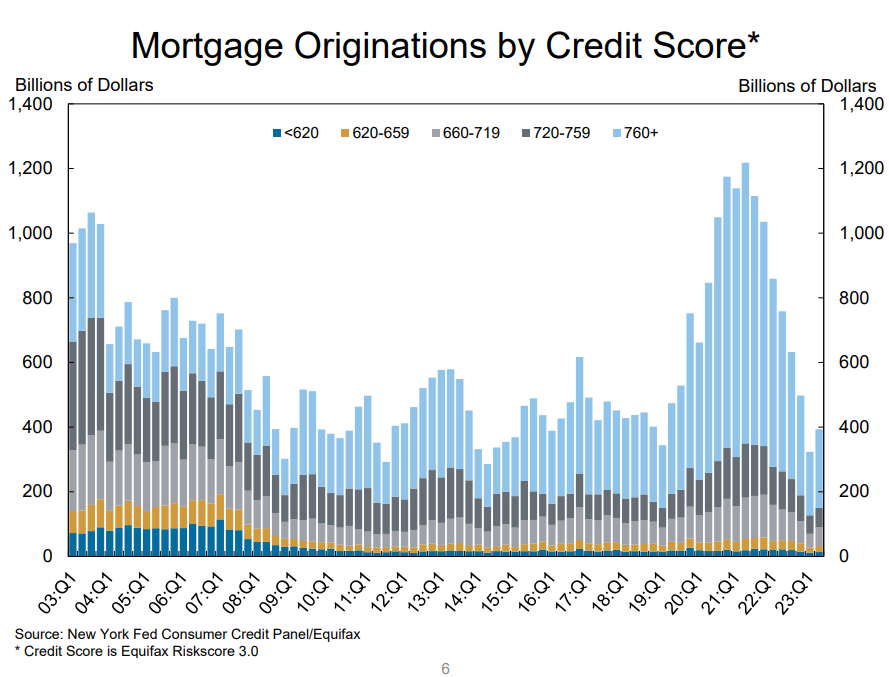

High Quality Mortgage Origination

All investor eyes will be on the FOMC this week as well as the Apple earnings report on Thursday. As far as the FOMC, the consensus is for the Federal Funds rate to stay in its 5.25/5.50 range. We feel that that the FRB will continue to refrain from raising rates any further despite the uptick in the ISM data that we have seen. We view most of the data the FRB refers to are lagging indicators and that a slowdown in Q4 is the consensus estimate and this is why the FRB will be in a more wait and see mode.

The real problems lie down the road if inflation does remain sticky and the economy does indeed take a turn for the worst. The FRB knows the history and they know the investing world always expects them to cut rates in order to solve slowdowns, but they DO NOT have this flexibility now.

There is far too much debt, far too much spending and any reduction in rates will send asset prices initially rocketing higher further exacerbating the already tight housing supply and lack of affordability and continued pricing pressures across goods and services. We know they FRB will make the mistake of reducing rates once we get our first few Negative Non Farm Payrolls and that will usher in the major blow off top to the collapse in all asset prices as the economy falls into a hard landing.

The right thing for the FRB is to do nothing, leave rates > than 5% and let the economy adjust as it will no matter how bad things get. We also know geopolitically the world is very unstable and that disruptions on a global scale are outside the control of any central bank and that also poses a very big problem for the FRB.

We also wanted to share this chart from the quarterly NY FED banking report. What it tells us is that housing prices can remain elevated despite the massive increase in rates. This is because the majority of the loans post covid went to high quality score borrowers who most likely not only locked in their own residence but bought investment properties with ultra low rates as well. So this would suggest the higher rates will not dampen pricing as many believe because the supply of homes will remain low and duration of the mortgages are now extended and locked in sterilized by the higher rates (meaning no incentive to liquidate or refi). This is important and the FRB will most likely be looking at this to suggest it can stay higher for longer:

Now this situation could change should we get an economy with increased layoffs and joblessness, but we are not there now.