GFBP Position Tracker & Market Update 6 18 20

Options Expiration Strangling Equities

Overall the markets continue to trade within a range here as the heavily anticipated options expiration in the equities is upon us. As we noted in our past notes, the .618 level in the SP500 which sits near the 3113/3115 area in the SEP future continues to magnet pricing.

After an overnight battle which saw Asia initially get the beat down to then front run the EU open to taking things back up. Then saw some profit takers hit things into early NY session which ended up seeing most of the selling rebutted with a constant effort ending the day at 3098.00 -9.00

One of the things we noted today was the positive news out of the Mortgage Application area where Joel Kan of the Mortgage Bankers Association had this to say, "Purchase applications increased to the highest level in over 11 years and for the ninth consecutive week. The housing market continues to experience the release of unrealized pent-up demand from earlier this spring, as well as a gradual improvement in consumer confidence,"

This is certainly good news for main street America, but we also read a bit about the ongoing Covid Forbearance some consumers have opted to go for which allowed them to take a few months off from paying.

We know things like this on the forefront seem good, but there are unintended consequences, such as accruing principal and interest payments. Also we want to note the fact that borrowers that opt for this, won’t find it very easy to refinance to a lower rate as their mortgage will not be current.

So on the forefront, yes something needed to be done, but in reality, we don’t think the solutions that have been enacted are the best options for the consumer base. This consumer finance link provides a nice overview of this forbearance and the associated risks, Covid Forbearance Risks

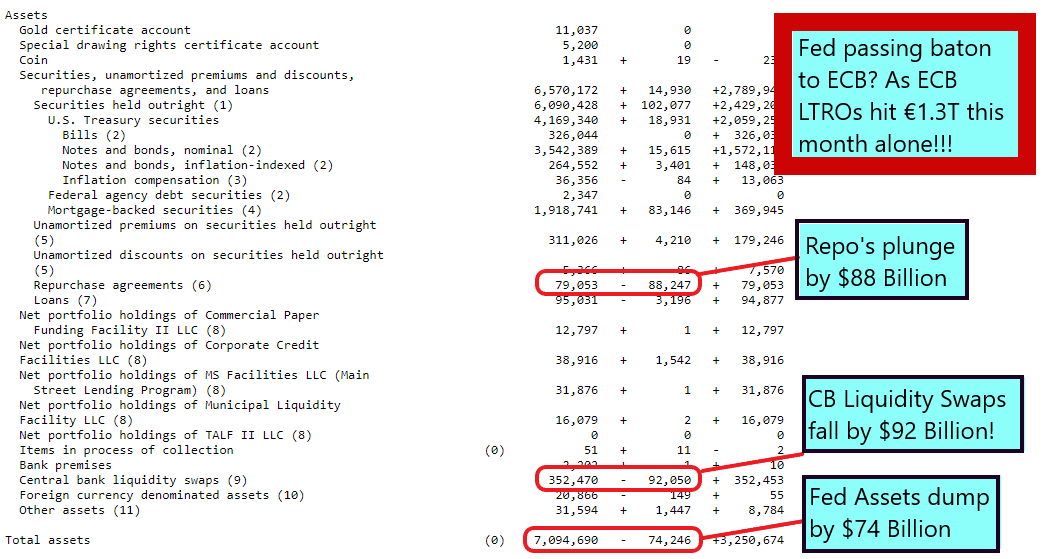

Another item we noted today was the Federal Reserve’s Assets fell by $74 billion the largest weekly drop in over a decade!

The central bank liquidity swaps which fell a massive $92 billion and rounding out the losses was the $88 billion plunge in Repos. Our graphic here highlights all the reductions:

We can’t help but think once again the Federal Reserve continues to play coordinated asset boosting debt printing, baton passing with the other global central banks in particular, we can see here that the ECB has gone full tilt overdrive with their LTRO program which is a staggering €1.3 Trillion, but who’s counting?

By the way the lowest rate on this stuff is -1%, so yeah being a well connected bank offers you the luxury of being paid to take on debt, how does that negative WACC work again? as the FT noted,

“ The banks are due to use about €760bn of the ultra-cheap loans to repay earlier ECB loans that are about to mature. But they are expected to use much of the remaining €549bn to buy bonds issued by their own governments — earning them an instant profit on the “carry trade” between the negative rate from the ECB and the higher yield on government bonds.

Did you get that part about “INSTANT PROFIT!”

So yeah when you say earnings and traditional economics matter, well not so much, not when you have non-zero sum players dictating allocation of devalued currency.

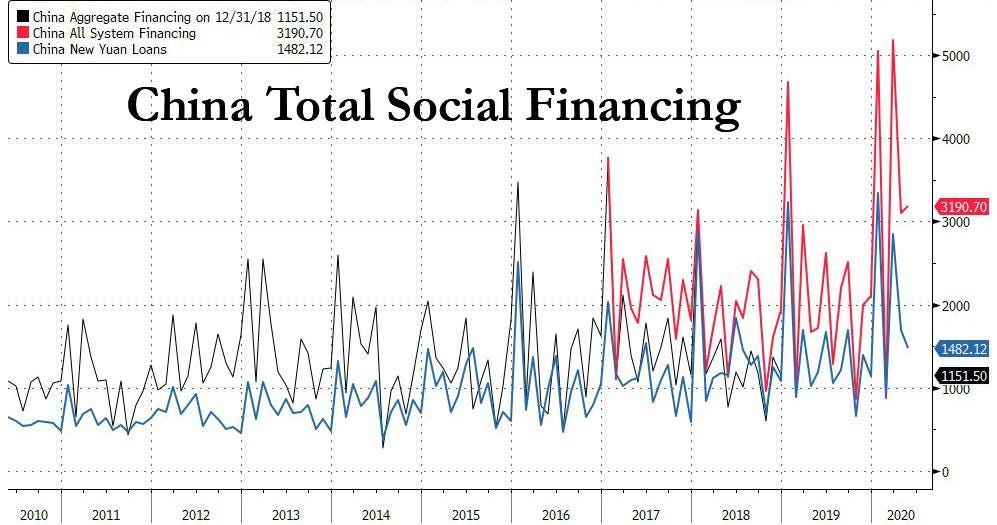

Speaking of currency, how bout that PBOC? Which announced late today they are going to unleash about 30% of GDP in total social financing this year which amounts to $4.2 trillion up from $2.8 trillion last year.

So with all this new debt funny money sloshing around, why would anyone expect risk assets to care about Covid, geopolitical or any other risk? They don’t and they won’t!

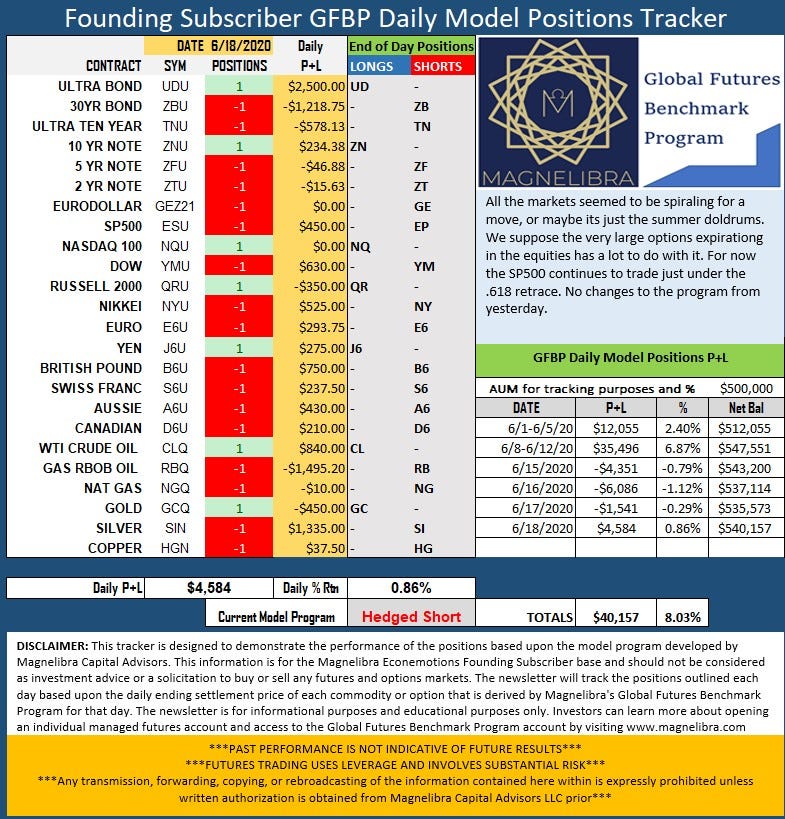

OK here is the GFBP position at close for 6/18/20 the RBOB was the major thorn in the side again but we will continue to monitor things here as the futures are ripe for some movement. The breakout will lean us into a momentum trade and we aren’t going to anticipate which way or what markets will be the determining factor, tomorrow may provide more clues, but for now Hedged Short continues:

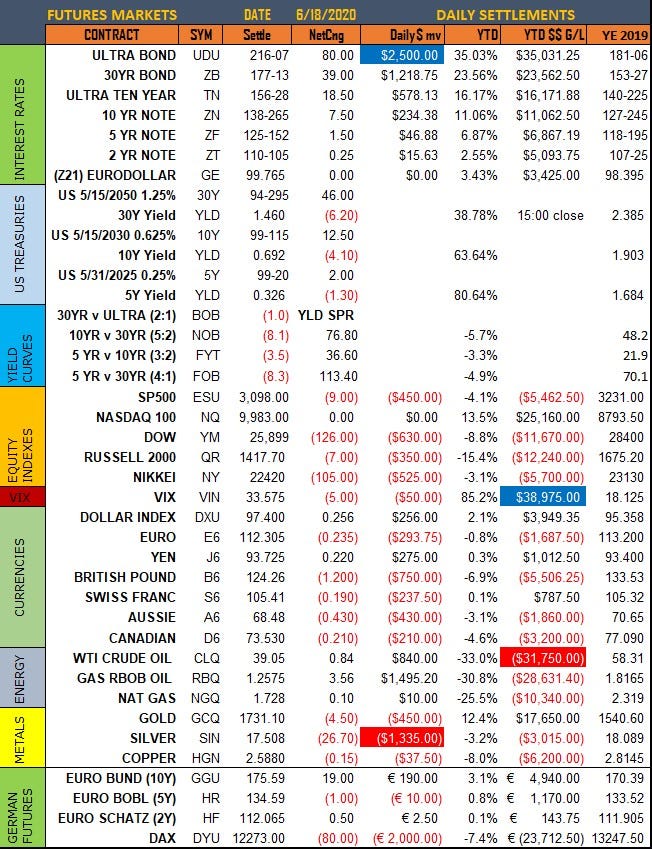

Here are the daily settlements of the markets we cover, take a look at the rare US Treasury Curve FLATTENING. It hasn’t happened often lately, but today was an exception as the 5-yr gained just 1.5 ticks while the 30-yr Bond rallied up over 39 ticks leading the FOB to fall 8.3 ticks:

Once again we hope you are enjoying a free look into our tracker, its only going to be free for a limited time. Monthly subscribers get all of the free content plus access to daily settles but the Founding Subscriber will continue to enjoy our Magnelibra Global Futures Benchmark Positions Tracker. We like educating, we like writing and researching but as you all know everyone’s time is worth something, we hope you understand. We hope you choose to stay the course with us as we look to broaden you understanding and your knowledge of how a professional futures manager looks at things.

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.