Global Oil Demand Goes Mad Max

The last thing the world needs is an oil supply shock!

Mad Max debuted in 1980 and it starred Mel Gibson in his first major film role. Max Max takes place in a dystopian future where society has broken down and Oil becomes the most sought after commodity. This film isn’t for everyone, but we enjoyed it and at the time of its release, despite its $400k cost, it ended up grossing well into the hundreds of millions. Perhaps it might be time for a re-release of this original at the box offices, considering the quagmire that we the world now finds itself in given the new assault on Iran.

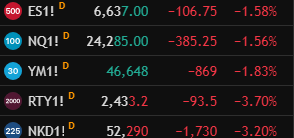

As of this post tonight on Sunday night’s open Crude Oil futures are up nearly 20%:

The equity markets are taking it on the chin led by the Russel2k down -3.7%:

We here at Magnelibra have to always quantify scenarios, base case to worst case and with that, our worst case considers a prolonged war without diplomatic resolutions. American hegemony is and will always be consistently tested due to the nature of being the big dog on the block. However, sometimes the big dogs arrogance sometimes gets the best of them and things do not go as planned. This not going as planned, is our worst case scenario.

As long as the capacity to destroy the very foundation of the worlds capacity of extraction, production and distribution of global oil supplies, then the overall supply disruption will force global oil prices higher and higher and this oil shock given the post covid global money supply glut, could push prices far higher than many might fail to perceive.

With pretty much zero checks and balance on electronic pricing models via our global exchanges, there are risks of prices going wherever they want to, even if it means negative (below zero, like it did in April of 2020) or well above $250 a barrel. Even if all the quants and Ai systems believe the odds to be astronomical, this does not change the probability of being greater than zero that this can happen.

Last week already saw a terrible jobs number in fact it was a massive 6 sigma miss and now we have Oil about to go parabolic, combined with massive losses on this decades GFC catalyst also known as Private Credit, well then you have the economic fundamental backdrop that all points to the same direction:

CAPITAL PRESERVATION AND RISK OFF

We know the Trump Administration has run every scenario and we also know the arrogance of Trump and our hegemony is now a weakness in regards to effectively gauging real risk, because even if the overall odds of the United States ability to manage a successful campaign comes with a 99.9% confidence level, doesn’t mean that 0.1% failure rate could grow over time and start compounding the longer this skirmish goes on.

If the U.S. decides to go full scale and start bringing in ground troops, our base case for Oil will then rise to $200 per barrel and the economy will be thrown into the arms of a full fledged recession as prices across the board initially increase but with demand collapsing prices will then have to fall and the equilibrium of all things moves toward deflation and a global collapse of confidence.

This is a very real danger and its one that we need to absolutely and accurately quantify every step of the way.

On the quantum level we know reality and matter are an output of the probabilities that exist at any given point in time. This is important to understand because we have to acknowledge that our world is chaotic and dynamic and ever changing. This uncertainty is compounded with the sheer fundamental flaw of man and its propensity for “control.”

However, this doesn’t change the fact that this propensity for change means that every decision shapes the future, good, bad or indifferent and that is why we need an acute process that can establish a base level by which we then deviate from and this deviation can form many different path ways, and every choice changes the future outcomes probability.

Yes, we know it’s a lot to comprehend but on the base layer, it’s quite simple, every decision either moves the entire system toward a more favorable overall outcome or a more unfavorable outcome.

For example the worst case scenario:

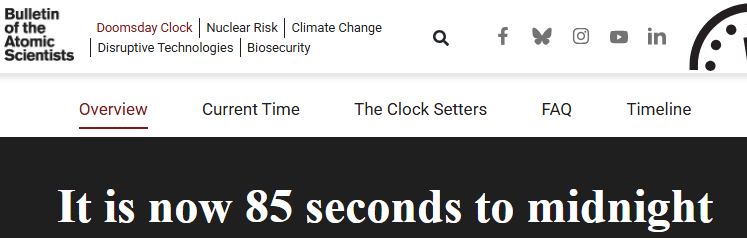

U.S. attacks Iran → Iran attacks local U.S. bases and allies → US escalates presence in the Mid. East. → Iran requests China and Russia its allies to step up → Dooms Day Clock moves to 10 seconds to midnight from its current 85 seconds → Use of Nuclear weapons from any one of the players becomes inevitable.

Now let’s look at the best case scenario:

U.S. attacks Iran → Iran attacks local U.S. bases and allies → U.S. and Iran deescalate and move toward a diplomatic brokered peace detail and security framework for the next 25 years.

You see every step of the process comes with a probabilistic outcome to assess, the outcome for humanity changes with every major decision and this is why its important to stress diplomacy over forced bending of the knee!

We suspect the coalition NATO forces will have to start escalating the situation and try to assert itself in the SouthEast section of Iran to try and gain control of the straight of Hormuz. This means an increase in bombing in those sectors and then the escalation of airborne and ground troops to secure offensive and control positions in this region.

If this does happen, well then our worst case scenario starts to take shape and its something we will have to monitor very, very closely.

We hope we have outlined what to expect here now and we hope you are picking up what we are putting down. As we have many times over the last year, everything is cycling and those that have been lulled to sleep by a never ending monetary central bank spigot are in for a very rude awakening.

WHY YOU SHOULD SUBSCRIBE:

So that you can become the most well informed member of your inner circles. So that everyone can look at you and wonder in sheer amazement as to,

“how in the hell does this guy know so much!”

Decades of artificially low interest rates and monetarist policy have concentrated wealth in financial assets held by a relatively small share of the population, leaving most participants outside this ecosystem. This imbalance is structural rather than cyclical. Corrective forces, whether regulatory, structural, or societal, are not a matter of probability but of timing.

Looking ahead, the coming decade is likely to be defined by meaningful disruption. The monetary framework that supported the last cycle’s growth is inherently fragile. In this environment, assets such as gold and silver are positioned to respond quickly as markets reprice systemic risk.

The impact will not be evenly distributed. A small group of investors will recognize these signals early and adjust accordingly, while many others will not. The following analysis lays out the key indicators, the most probable scenarios, and the reasoning behind our positioning, connecting these elements to reveal patterns that often go unnoticed and providing a framework for thinking critically about what comes next.

***DAILY SUBSCRIBER ONLY SECTION***