Higher High Equities & Vix = Rare

Settles for August 28th 2020 + Tech Charts

Generally Magnelibra will reference the very well known Vol Smash incorporated at the end of any near down day in the equities (rare) by which a systematic program simultaneously sells Vix in order to generate equity buying. However this weekend we read a piece explaining why the Vix continues to rise in correlation with a rising Nasdaq and SP500 market.

The BearTrapReport blog noted that:

“On Wednesday and Thursday, the VIX was more than 5% higher each day, with the S&P 500 up both of those days.” How rare is this? Very.

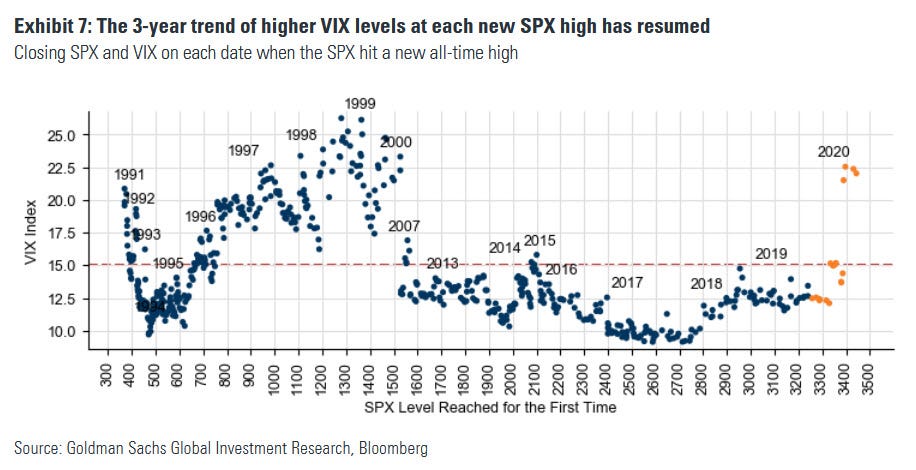

According to Larry MacDonald, there were just ten days in the last decade with the S&P up 1% with the VIX closing higher. Furthermore, this is especially rare with the market at all-time highs, and as Goldman showed, the last time the VIX was this high at an all time market high was in March 2000, just before the dot com crash:

Citadel sited that single name Tech call and call spread buying has led hedgers to reaching for Nasdaq volatility causing this uptick in vol to be well induced from all this extended over reach in buying these single name techies.

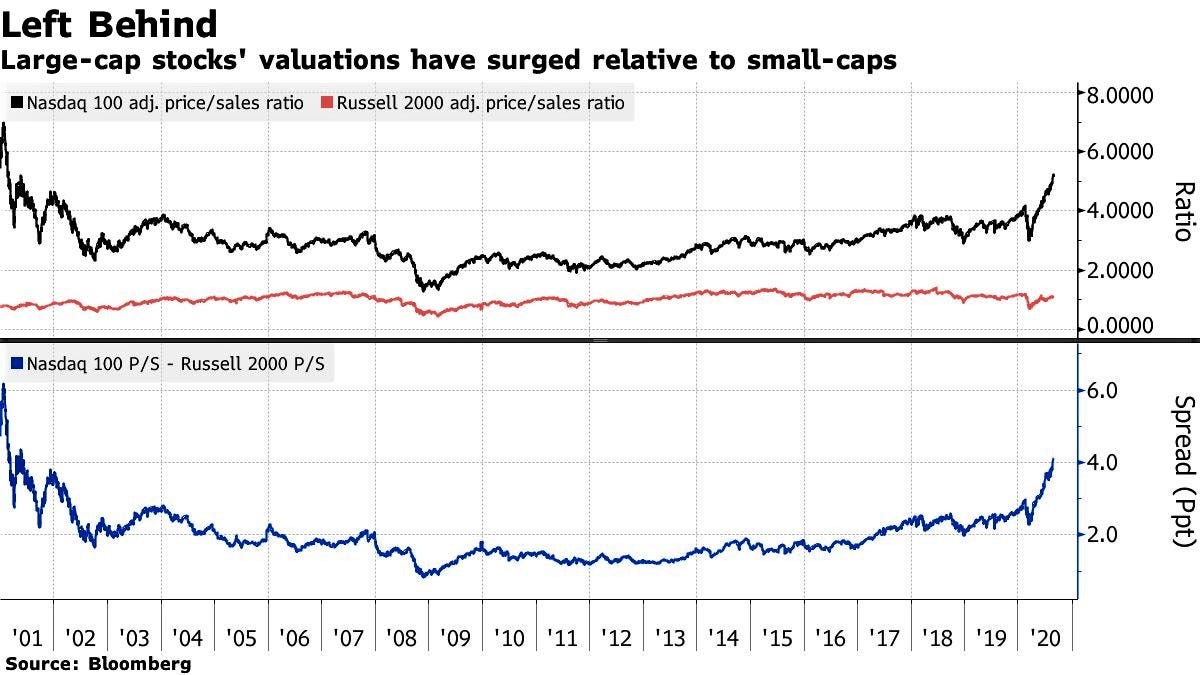

The Nasdaq has been the clear winner as Tech Large Caps have certainly ripped the doors off of small caps Russell2k:

So we are certainly in a situation where extensions are leading to rare inverse moves that continue to take many by surprise. However, in a time when Central Banks are hell bent on providing by any means necessary via as much liquidity as possible then these distortions can go on for a lot longer than many suspect.

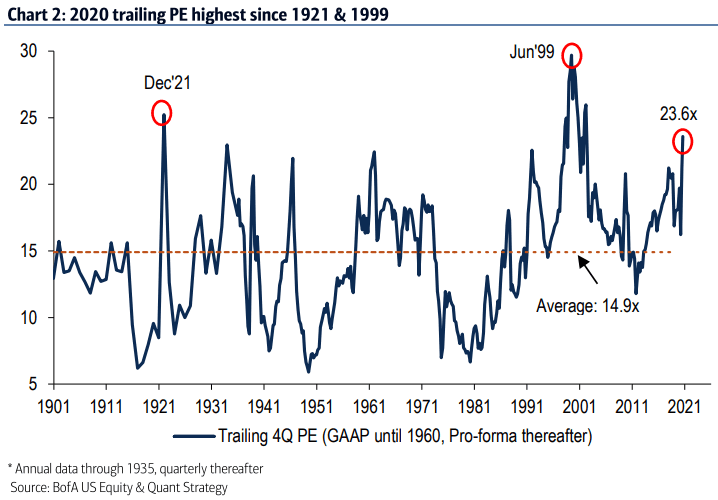

Many look at fundamentals like this such as trailing PE and yes we are marking above historical norms, but don’t be mistaken, there’s plenty of distortion left:

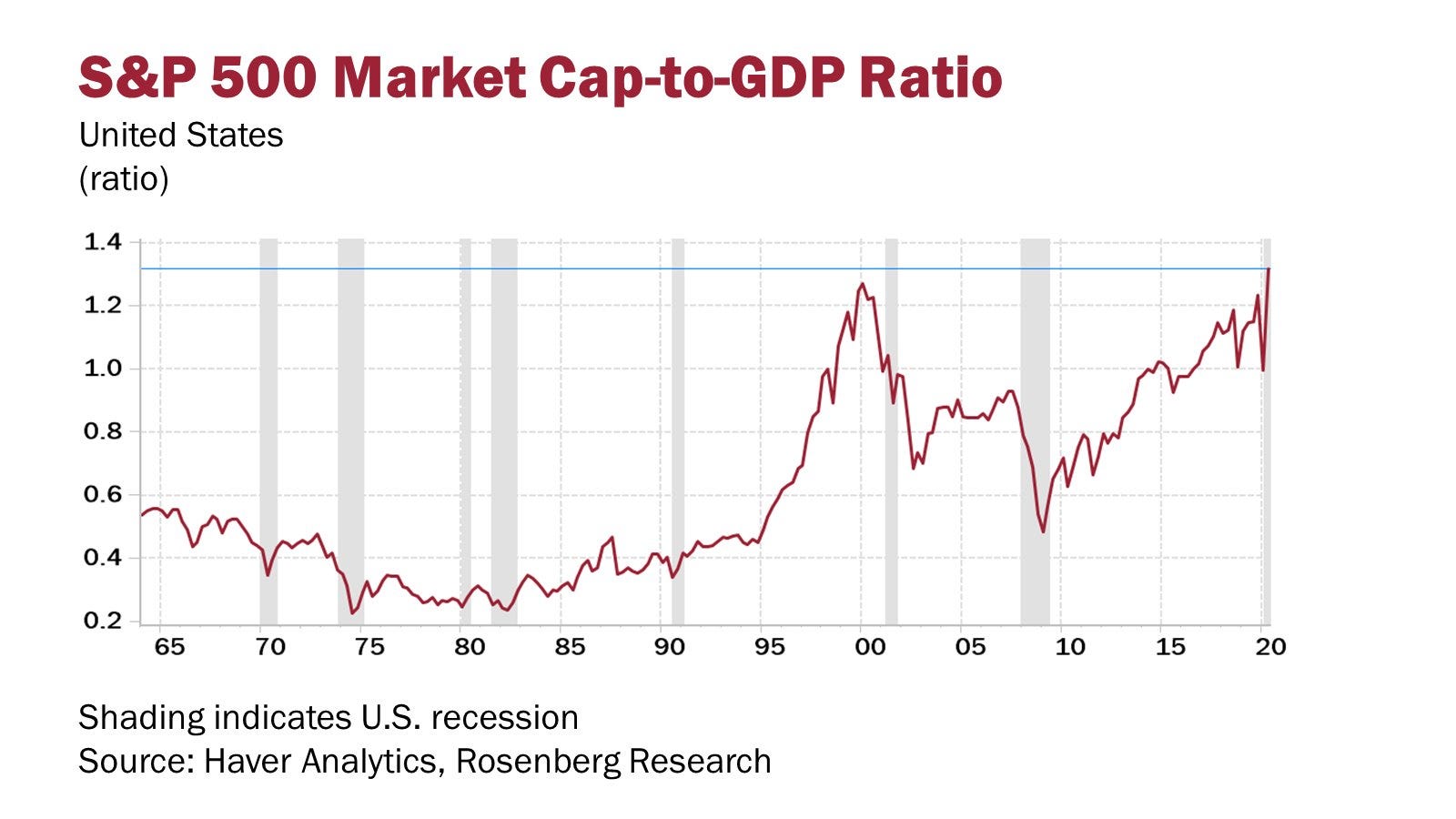

Putting this all together, it should come as no surprise that the SP500 Market Cap vs GDP Ratio chart is up where it is:

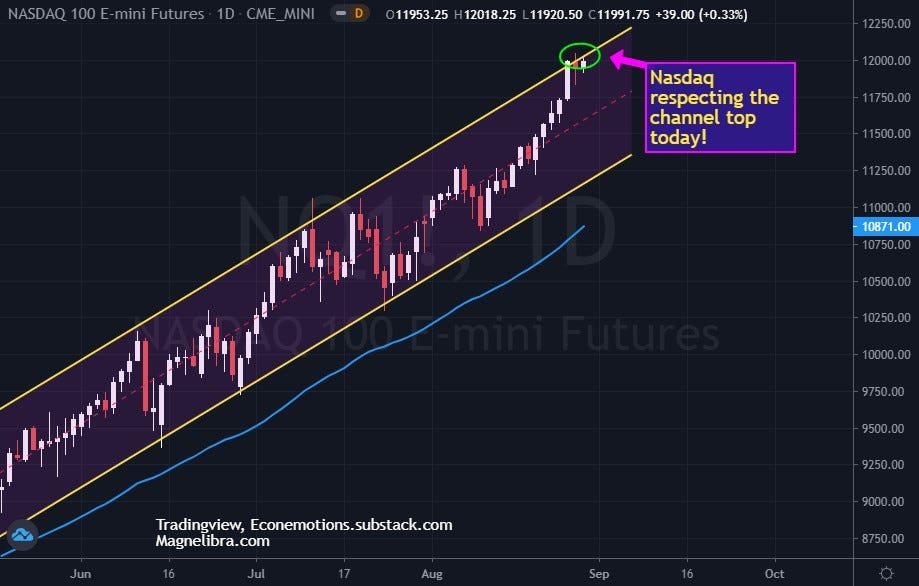

OK, to the technical side of our markets, first up Nasdaq at the top of our 5 month channel, risk vs reward anyone?

SP500 just playing catch up with NQ:

US Govt 10Y Yields:

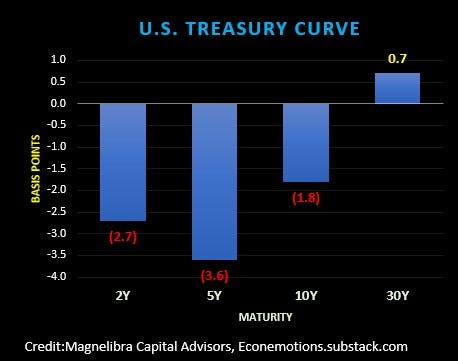

Speaking of US Treasuries, the FED gave the green light to inflation so a bout of bear steepening continues as Friday’s curve changes show the front end with a big out-performance vs the long end:

Euro clearly benefiting right now:

Gold also sees the inflation devaluation writing on the wall:

For Magnelibra the writing has been on the wall for awhile, that is the FED and the global central banks have covered the pandemic panic and then some. If we can reopen things here and if America can get its act together and stem some of the angst then maybe just maybe we can continue on the path to recovery, not just in equities but across all our industries and get everyone back to normal!

We had a great conversation with a few potential investors on Friday, and the one constantly mentioned question was “how high can the markets go?” Well you know our answer to that, “As high as it takes to have sellers show up.” Are we there yet? Well the answer is to be determined and rather we would like to rely on our knowledge of rates, QE and the monetary mechanism and with $14Bln a day in QE still, you know where we stand!

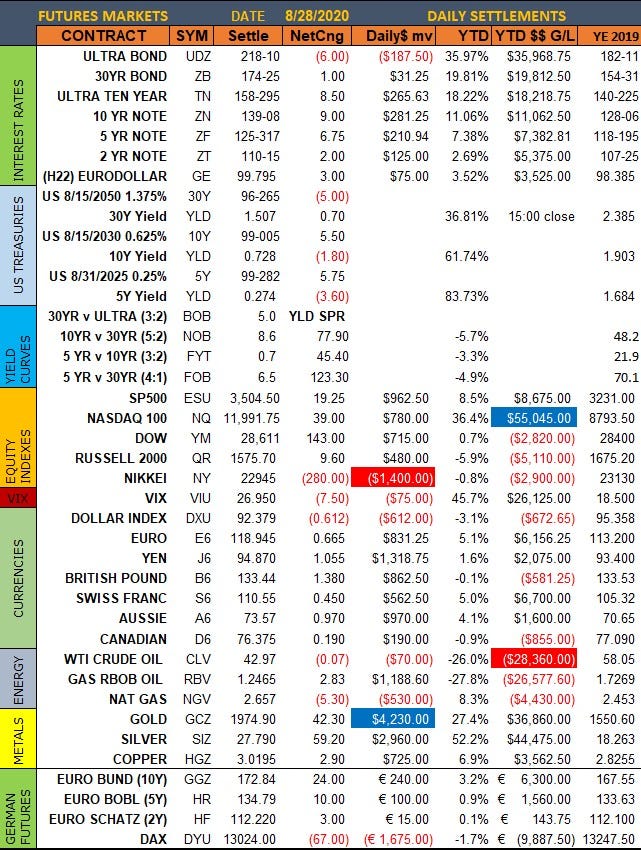

Here are the settlements for Friday August 28th 2020:

If you want to become a paid content subscriber or even a full Founding Member and have access to Magnelibra’s proprietary “Global Futures Benchmark Program Positions Tracker,” (a unique global macro program that is a proxy to the systematic approach Magnelibra Capital Advisors the Commodity Trading Advisor uses for its individually managed accounts), then feel free to hit the subscribe button below.

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.