King Elon, a $2 Trillion Crown, and a Dollar Nobody Wants to Talk About

SpaceX goes public. Markets chase the headline. The real story is what it costs in a currency the Fed is printing at $6 billion a week.

The SpaceX IPO landed on June 12 and by the close Elon Musk had crossed into territory no human being has ever occupied: a net worth above one trillion dollars. The financial press treated it as a coronation. Magnelibra is treating it as a math problem. A nearly $2 trn. dollar opening market cap on a company that has never traded a single public share and operates in a sector with no comparable valuation anchor is not an investment thesis. It is a liquidity event dressed in rocket exhaust. We will not include SpaceX in the MEGA9 tracker. Our standard requires at least six months of real live public trading data before any company earns a position in the model. SpaceX has zero days. That rule exists for exactly this situation.

The dollar is the part of this story everyone is too polite to say out loud. Musk is now worth more than one trillion dollars, denominated in a currency the Federal Reserve is printing at approximately $6 billion dollars per week to buy Treasury bills, with a balance sheet that has quietly climbed back to $6.77 trillion, well off the lows that were supposed to signal tightening. The Fed is not tightening. It is running what Magnelibra calls QE-lite, buying duration with newly created money while telling the public it is managing the balance sheet. The first trillionaire was not created by a rocket company. He was created by a printing press. The dollar has simply become cheap enough that a trillion of them is now a single man’s net worth.

Iran is the other headline. A peace framework is being floated and markets are reacting as though it is real. Magnelibra’s read is simpler. The Middle East has produced framework agreements, ceasefires, and diplomatic openings in a continuous cycle for decades. None of them have produced durable peace and there is no structural reason this one will be different. What they do produce reliably is volatility. Volatility is profitable for the right participants. Trump-era diplomacy in this region has historically followed the same pattern: loud announcement, market move, quiet reversal. We are not positioned around an Iran deal. We are positioned around energy fundamentals and the trend.

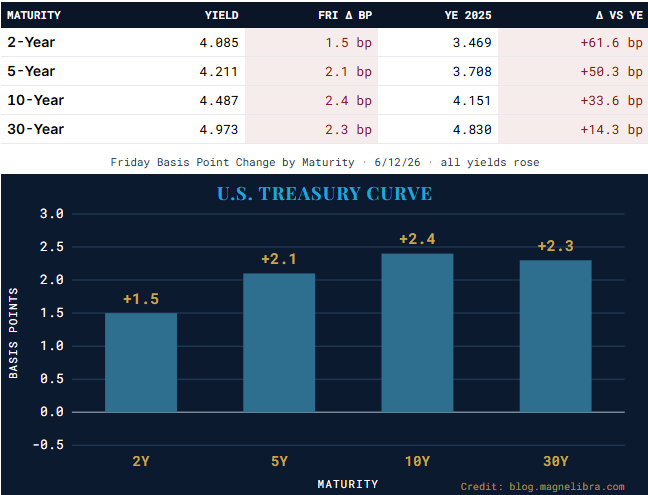

Equity indexes are pressing against the highs heading into a week with real catalysts. The S&P settled at 7,435, the Nasdaq at 29,662, and the Nikkei at 67,335, up 33.19% year to date. The SpaceX IPO euphoria has a real chance of driving the market into new high territory this week. Magnelibra expects that push to fail. The 10-year yield at 4.487% and the 30-year at 4.973% are not the environment in which equity multiples expand sustainably. The compression between record equity prices and elevated real rates is the tension that resolves, eventually, in the direction of rates.

The bond market is the tell. The 10-year yield chart is forming what looks like a stabilization pattern under the 4.610% resistance that has capped every yield spike since 2023. Four red arrows on that chart mark four failed attempts to break above that level. The fifth attempt is in progress. If yields fail at resistance again, the stage is set for a meaningful rally in bonds, exactly what the long ZB and now long ZN position in the Trend Program is built for. The FOMC minutes drop Wednesday. With the Fed actively buying Treasury bills at $6Bn per week, any talk of further rate hikes in those minutes would be a contradiction in plain English. We will read them. We do not expect them to change the structural picture.

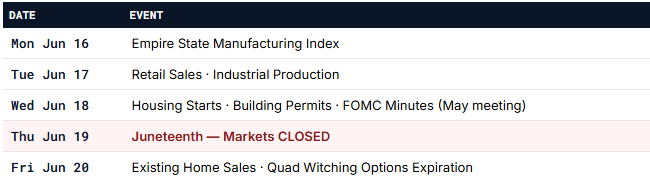

Week Ahead · June 16–20, 2026

Key events · Thursday markets closed for Juneteenth · Quad witching Friday

Three items stand out. FOMC minutes Wednesday: the Fed has been purchasing Treasury bills at approximately $6 billion per week while holding rates steady. Any language in those minutes suggesting further rate hikes is a direct contradiction of active balance sheet expansion. Watch the bond market reaction, not the headline. Thursday June 19 is Juneteenth: US markets are closed. Friday is quad witching options expiration, which adds intraday volatility and positioning flows to an already headline-heavy week. Plan around the Thursday closure.

I · Futures Market Trend Program

Hypothetical systematic trend-following · 22 markets · $250,000 start · not advisory

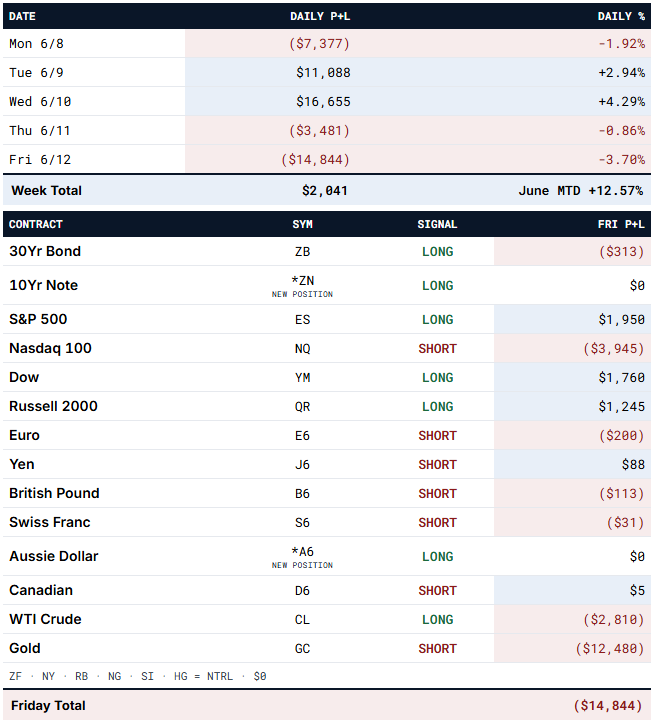

The week finished positive despite a difficult Friday. Gold rallied sharply and the short GC position gave back $12,480, the single largest loss on the book. Short NQ cost another $3,945 as tech bounced. The long equity basket (ES, YM, QR) contributed $4,955 to offset. Two new positions entered Friday: ZN (10-year note) flipped to LONG on a sentiment change, adding a second long duration position alongside ZB. A6 (Australian Dollar) flipped to LONG. Note: Nikkei rolled to September (NYU). All currency contracts rolled to September. Copper rolled to September.

YTD: $136,439, +54.58%. June MTD: $43,141, +12.57%.

II · MEGA9 Tracker

SpaceX IPO · Not Included · Policy Note

SpaceX (SPCE) went public June 12, 2026 at a near $2 trillion opening market cap, which would place it among the largest companies on earth by any measure. Despite its size, SpaceX is not included in the MEGA9 tracker. Magnelibra’s standard requires a minimum of 6 months of real, live public trading data before any company is eligible for inclusion. SpaceX has zero days of public history. A $2 trillion valuation with no public trading record is a liquidity event, not a data set. We will revisit eligibility in December 2026.

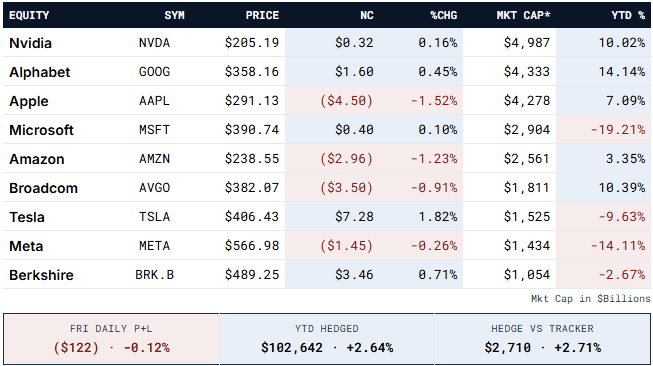

Equal-weight $100,000 · 9 largest US companies · Friday 6/12/26 settle

Total market cap $24,886 billion, below the 50-period MA at $25,345 and well below the 21-period MA at $26,247. The cap structure is compressing. Five names gained Friday, four declined. Microsoft extended its YTD loss to -19.21%, the worst in the basket. The 5 QQQ 720 calls expired, generating $680 in realized premium for the week, YTD options P+L $2,710. This week the hedge targets the 740 call at $5 or better. Resistance sits at 735 on the weekly chart. Daily P+L ($122), -0.12%.

YTD tracker $99,932, effectively flat. Hedged balance $102,642, +2.64%.

III · Treasury · Yield Curve

Yields rose Friday but the weekly structure is stabilizing · 10Y resistance at 4.610% · ZB and ZN both LONG

Friday saw yields tick higher across the curve, bear steepening with the 10-year up 2.4 bp to 4.487% and the 30-year up 2.3 bp to 4.973%, holding just below the 5.000% level. But zoom out. The 10-year yield chart is the most important chart in the market right now. Four consecutive failures at the 4.610% resistance level dating back to 2023 have defined the yield ceiling. The fifth test is approaching. If that resistance holds again, the next move is a rally in bonds. Magnelibra holds both ZB and ZN (10-year, new long added Friday), both positioned for that outcome. The Fed buying $6 billion per week in T-bills while rates sit at current levels is not tightening. The FOMC minutes Wednesday will be read carefully for any contradiction between the rate language and the balance sheet reality.

IV · Equity Index Futures

Friday broad rally · SpaceX IPO euphoria · Nikkei leads YTD at +33.19% · Note: Nikkei rolled to Sept (NYU)

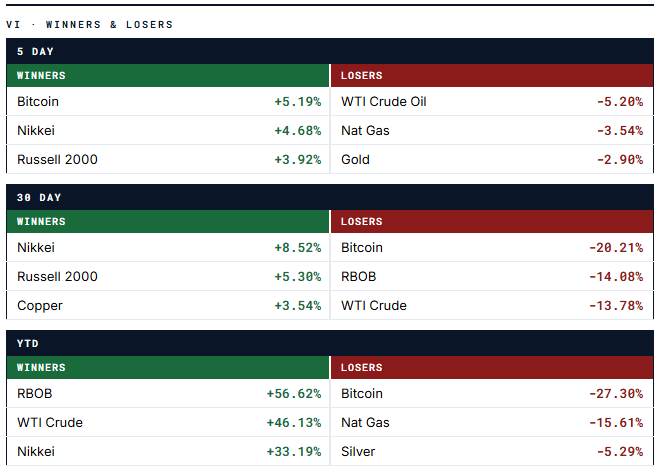

All five indexes closed higher Friday. The Nikkei led with 890 points and now sits at 67,335, up 33.19% year to date, the strongest index in the MEGA9 universe by a wide margin. The S&P is pressing toward the 7,650 weekly resistance with support at 7,275. Nasdaq futures tested the 30,850 weekly resistance and settled at 29,662. The SpaceX IPO euphoria is real and the momentum could push indexes to new highs this week. Magnelibra expects that push to be a selling opportunity, not a confirmation of a new leg. Elevated rates and a compressing MEGA9 market cap do not support multiple expansion at these levels.

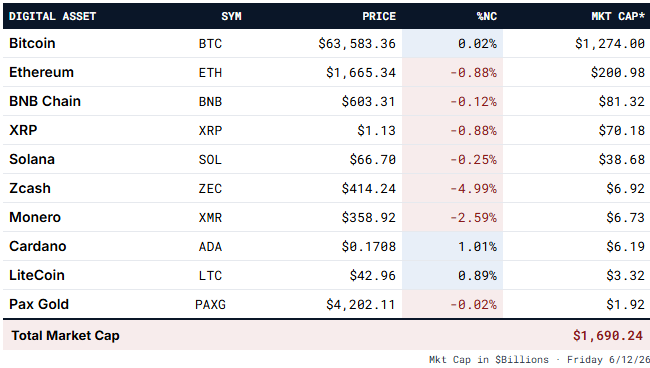

V · Dollar, Bitcoin & Commodities

DXY 99.489 · +2.00% YTD Bitcoin $63,583 · -27.30% YTD

The dollar nobody wants to discuss · QE-lite at $6Bn/week · Gold and oil at key support

The Dollar Index sits at 99.489, holding just below 100 but up 2.00% year to date. Here is the number that matters more: the Federal Reserve balance sheet has risen back to $6.77 trillion, purchasing approximately $6 billion in Treasury bills per week. This is not a neutral policy. It is money creation with a different label. The first trillionaire was not built by a rocket. He was built by a currency cheap enough that a trillion units is one man’s net worth. Gold pulled back sharply this week and sits near $4,283 on the weekly chart, testing the 4,025 weekly support with the 4,450 resistance above. Silver and crude oil are at similar technical inflection points. At major support levels, two-way action should be expected. These are not one-directional trades at current prices. Bitcoin sits at $63,583, -27.30% year to date. The weekly chart shows price between 67,500 resistance and 52,800 support.

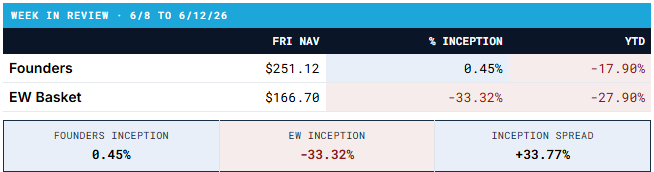

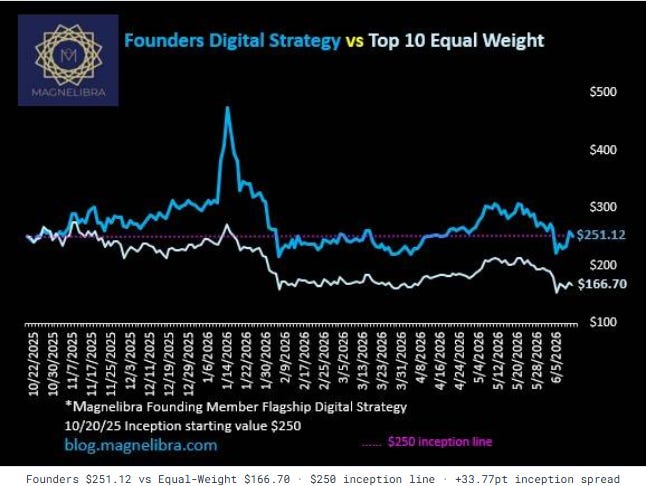

VII · Founders Digital Strategy & Bitcoin

◆ Magnelibra Founders Digital Strategy ◆

Flagship hypothetical digital-assets basket tracked via daily NAV. Founder Tier Perks: discretionary year-end rewards such as Visa gift cards as a thank-you for your support.

Monero · The Privacy Thesis

Monero (XMR) at $358.92 remains one of the most undervalued assets in the digital basket relative to its utility. Privacy in financial transactions is not a feature. It is a fundamental property of sound money. Every government surveillance expansion, every CBDC proposal, every KYC mandate makes the Monero thesis stronger, not weaker. The market periodically punishes XMR for the regulatory pressure on privacy coins. Magnelibra’s view is the opposite: the more aggressively governments pursue financial surveillance, the more valuable censorship-resistant, untraceable value transfer becomes. Privacy is not a trend. It is permanently undervalued at current prices, and it is a core holding in the Founders Digital Strategy basket.

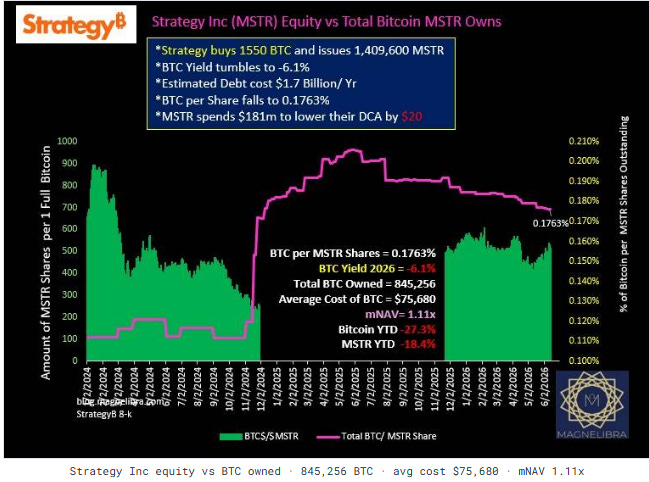

Strategy Inc (MSTR) · 6/12 $135 call expired OTM · new call Monday

The 6/12 $135 covered call expired worthless, adding to the cumulative premium captured of +90.3%. The strategy is down 22.2% year to date versus -67.4% for unhedged MSTR since the December 1, 2024 inception. mNAV has ticked up to 1.11x as Bitcoin held near $63,583. Strategy continues to hold 845,256 BTC at an average cost of $75,680. The covered call mechanic for this week will target approximately 5% out of the money from Monday’s open. If MSTR opens near $125, the $133 call is the target. The premium capture continues to significantly outperform buy-and-hold MSTR.