LULU

Indicative of the overall levels in the majority of equities

Ok, we get the average analysts optimism on Lululemon Athletica, with the obvious heavy tilt towards “overweight” as well as the recent price level upgrades near $385, but we have to be honest, if gyms are closed, if everyone is working from home, is there some pent up demand we are missing?

We know the fundamental backdrop, we know the uncertainty and this stock has had a few obvious runs from $150 up to $275 and now up to $365, but we are skeptical. Then the realization sets in, that this is more of just the same QE pumping without rationality for any other metric at play here.

In fact Lululemon Athletica may as well be a tech stock at this point for what does it really matter what industry it is in? Our point isn’t to pick on LULU we know the cult following is massive and we get it, although we have to admit, when we see steamy middle-agers coming from their hot yoga classes and hanging out in Starbucks, well let’s just say it’s not the most flattering look. Is that harsh? Well we just call them like we see them and to each their own.

We know this trend of relaxing comfortable athletics is here, however as we stated, we don’t care about fundamentals or economics, we care only the purpose of QE and what it does, QE doesn’t differentiate, it doesn’t segregate, it walks thru and gobbles up with leverage by the way, any available asset class that’s for sale and that is our real point.

We often here the old, “how high can this go,” to where we always poignantly answer, much higher than you could rationally think! As Chucky Prince famously said to FT some 13 years ago:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing,”

He also at the time told the Financial Times that the party would end at some point but there was so much liquidity it would not be disrupted by the turmoil in the US subprime mortgage market. He denied that Citigroup, one of the biggest providers of finance to private equity deals, was pulling back. (wink, wink)

See what we mean folks, this was July 2007 and we all know exactly what the hell was going on at that time, well at least a couple of us astute bond players knew better. In fact we laughed when none other than Ben Bernanke in 2006 told CNBCs Maria B. infamously now, when she asked about housing prices,

“ Its a pretty unlikely possibility that we’ve never had a decline in house prices on a nationwide basis, I don’t think its going to pull the economy from its full employment path.”

The world, well maybe just the financial markets are a stark contrast to even a decade ago and its not that we are looking at LULU for some short term topping bias, but rather pointing out its more of an output function of all this QE, nothing more.

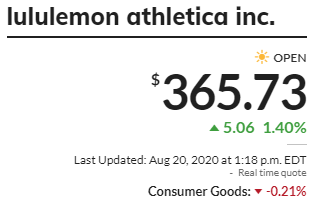

Here is LULU’s current price:

As far as the chart outlining our Fib. Extensions here you go:

Good luck traders and investors!

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.