Making Sense of the Fed Pivot

We have digested a lot of commentary over the last few days in regards to the FOMCs recent dovish stance. We also follow a lot of data points globally both in market pricing as well as analytical commentary from various regions. One thing we are certain is that Powell DID NOT WANT to flip flop like that. We saw it on his face, we saw it in his tentative voice and he knows what it meant to the markets. So with all of this insight we can only conclude one logical stance and that is the FOMC cannot control the other global economies despite their best efforts. Even worse he knows that if other economies are deteriorating, that it is only a matter of time before contagion spreads. The recent action out of the BOJ and the PBOC tells us Asia is a Potemkin Village, without continued central bank QE and liquidity injections it all falls apart.

As we have stated time and time again, we are very critical of the FOMC and the Federal Reserve Board (FRB) in general because we are Austrian Economists at heart, but they did get the rate hikes correct. They were late to the game, however and we would have started raising in a much quicker fashion some time in early or mid 2021, given the $6T in total stimulus, but that’s just us.

We would figure that their PHDs and AI models would have given them the correct forward path for CPI given such a dramatic increase in M2, which were direct payments with zero friction none the less!

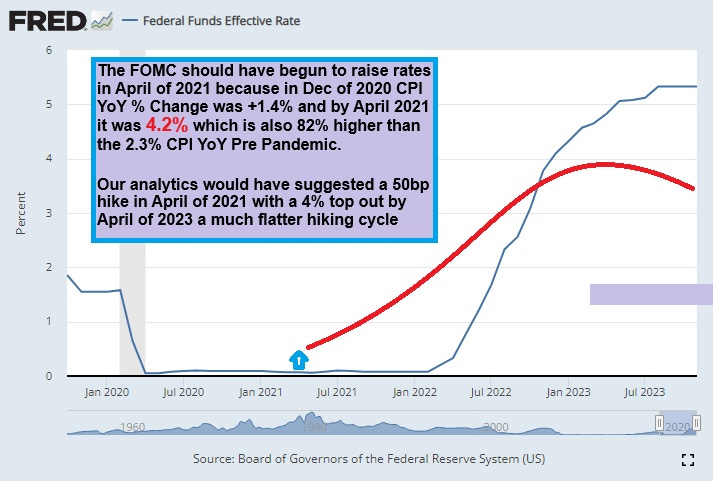

We find it very difficult to believe the FRB didn’t understand the dramatic jump in CPI in April of 2021 with a 4.2% print. The underlying fiscal and monetary stimulus coupled with constant generative AI overlay analytic models should have easily told the FRB that this was not “Transitory” inflation, but a more structural inflation that would need a stricter monetary policy. We would have gone with a rate hike expectation shown below in red:

Furthermore anyone involved with the markets at this point, either Equities, Bonds, Real Estate or Mortgages, knew the massive amounts of liquidity were leading to speculative fervor which was a direct result from monetary and fiscal policies. The lines were out the door at LVMH and high end dealerships, certainly not a sign of economic stress by any means!

Another stamp of validation for rate hikes at the time was the equity market acceleration higher, look at the SPX chart here at this point in time:

When we review the FRB minutes from the June 2021 meeting it confirms what we had already known, and the FRB knew it too, growth and inflation were heating up. Here is a quote from their June 2021 minutes,

The staff’s near-term outlook for inflation was revised up markedly, but the staff continued to expect the rise in inflation this year to be transitory. The 12-month change in total and core PCE prices had moved well above 2 percent in April, and incoming CPI data suggested that PCE price inflation would remain high in May - Fed Minutes June 2021

There is the FRBs favorite word again “transitory.” Now we can only come to the most logical conclusion as to why the FRB failed to recognize this kind of inflation. They did so on purpose, they ignored it!

Think of where all the money eventually flows when disbursed to the broader economy, its sent to main street, main street spends it and it ends up locked up in long duration, i.e. equity and home values. The FRB knew that the longer rates stayed low, the more capital would flow into risk assets and the greater the duration of that capital would then become.

Equities and Real Estate are long duration assets and what do we mean by long duration?

They are not readily bought and sold on a daily basis to generate liquidity. They are held for long periods of time and sold off incrementally to generate cash flow as in the equities or home equity is tapped at certain points in the future for liquidity.

They knew exactly where this was going. Just as they knew that they would sterilize all of this home equity and truly extend duration as higher rates would encumber and disincentivize anyone looking to extract equity from their home to refinance. This is exactly what has transpired today.

What this has led to is an absolute destruction of main street balance sheets due to higher rate debt and higher real costs for goods and services. Now we arent talking aboit the top 10%, who are immune from everyday inflation.

This disposable income destruction operates at a lag effect but it also distorts the housing market, because it reduces the available supply and keeps prices elevated. In reality once rates come down, we should see ample supply again and god forbid if unemployment ticks up, this may accelerate faster than the FRB can anticipate. In fact we are assured they will not cut rates until things are already accelerating lower in regards to GDP.

So all of this combined, with the new found FOMC doves will make 2024 a very challenging and volatile year, dependent upon the data, inflation and employment which will once again be the key data points!

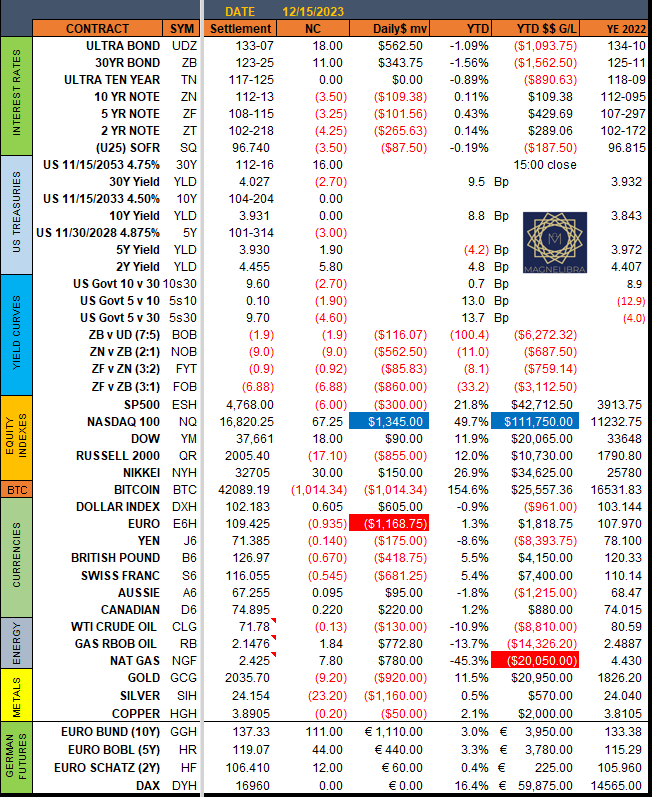

Ok onto our trackers and settlements, Friday we saw the US yield curve flatten with the long end outperforming, we saw the Nasdaq gain vs the other indices and the dollar was stronger with the metals down slightly. We rolled the energy sector to February from January Nat gas is Feb:

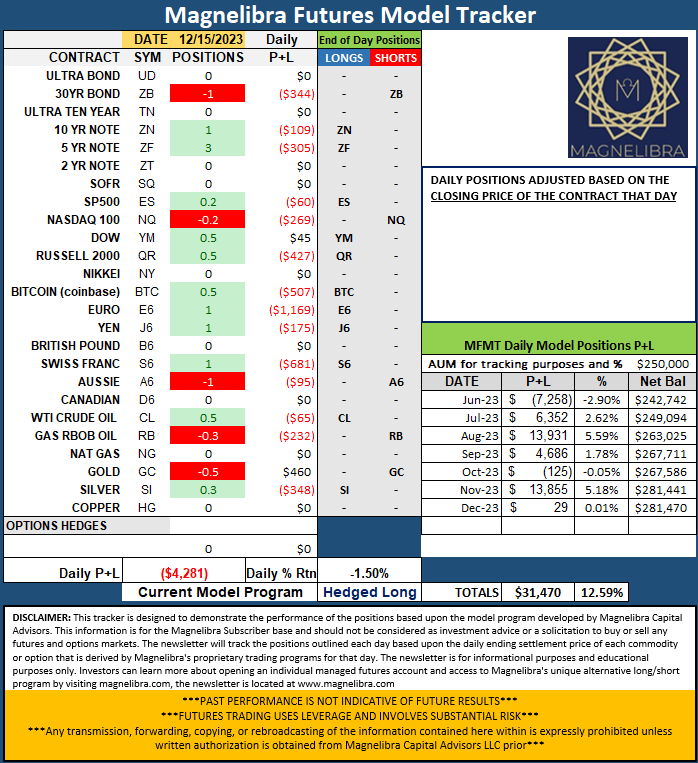

As far as the Magnelibra Futures Model Tracker, no changes on the positioning:

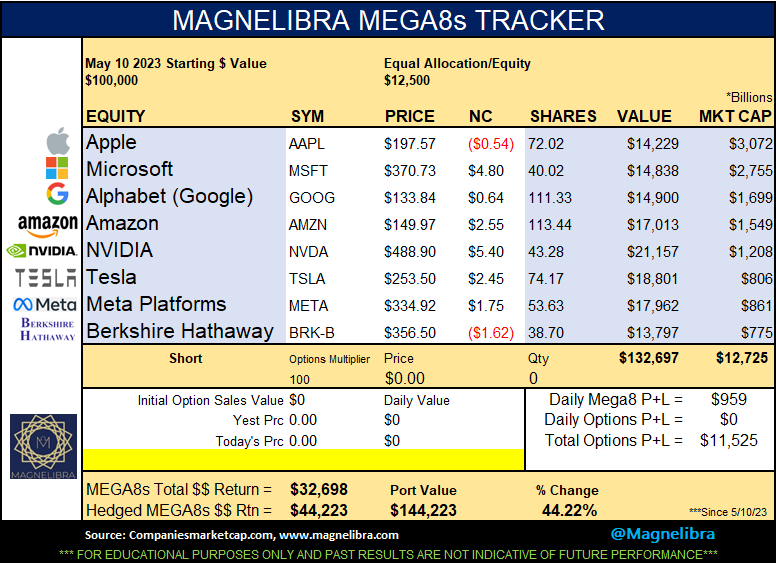

When we look at the MEGA8s tracker we see that Nvidia continues to press toward that $500 resistance again and as a group they did make a new all time Market Cap high, we will not hedge this group into year end:

Here is the current look at the Market Cap and Fridays new high:

Ok that’s it for now, we look forward to bringing you our 2024 outlook as well as our annual “Its a Wonderful Central Bank Life,” 2023 addition. Anyway we hope you enjoyed this post, if you did, give us a like, a share or if you are financially able, try to support our work. We truly appreciate all of our subscribers, we hope we provide a unique insight to markets, to monetary policy and to trading/investing and we look to continue this journey with you.