Massive NFP Beat & Equities Rocket Higher

US Treasury Yields Smoked

This morning saw the monthly BLS Non-Farm Payrolls release, expectations called for another drop in payrolls by 7.5 million and an expected rise of the unemployment rate to 19.1% from the prior 14.7%.

Instead of all that bearish expectation the BLS reported that total non-farm payroll employment increased by 2.5 million in May and instead of a record 19.1% unemployment rate it actually fell to 13.3% !

Of course President Trump wasted no time on Twitter:

American’s have become accustomed to his Tweets, many hate it, many love it, but you give him the ammo, he will let it fire and this kind of ammo in our book is good for everyone, when payrolls rise and unemployment drops, that is a GOOD THING!

So, with that, the country has seemingly taken it upon itself to reopen and to reignite our economy, despite all the apparent ineptitude and resistance from many of our governors and mayors out there. OK, look we will not discount the severity of the Covid, but let’s be honest, the shutdown worked and the data states it worked.

For those that continue to be afraid, its alright, we get it, we respect everyone and it is their right to wear a mask, not go outside and do whatever they feel they need to do in order to get through this in their own way. That is not what we are implying, rather as our long time readers know, we base our decisions on sound logic and sound, clean data. The data is suggesting that its clearly safe to begin opening and if all this rioting doesn’t cause a massive spike, well then this should provide further evidence to our claim.

Let’s get to some of the market moves, as expected off of a massive beat like that, equities have soared and what is strange is that percentage wise, both the Nasdaq and the SP500 have had similar snap backs both rallying 48% from the lows, someone can fact check this but here are the charts:

The Nasdaq Futures where we also want to note how the .786 Fib. Retrace held and was the start of the reversal back up:

The US Bond market didn’t fare as well, but it is now well off its high yield mark set this morning up at 1.76%. The bond has rallied some 50 basis points off its Covid lows down at 1.25% and is clearly taking the bulk of the selling in the complex as the front end (shorter dated yields) are anchored by the Federal Reserve’s ZIRP, which has lead to a massive steepening in the yield curve:

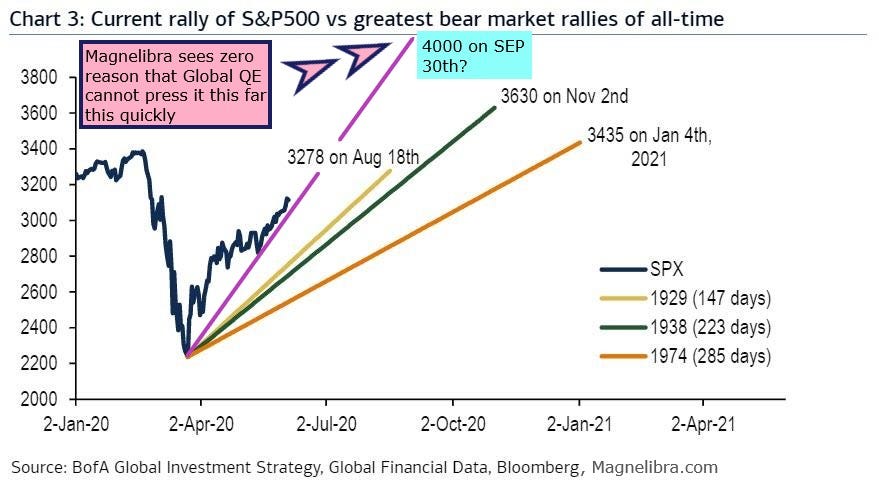

Finally, we will leave you with a decent chart of the prior SP500 rallies out of bear markets and we couldn’t help but add our own linear projection. What many over the last decade have failed to realize is that the general dynamics of nominal equity pricing comes from one single source, QE (Quantitative Easing).

QE is the single largest driver of all fundamental interest rate arbitrage and corporate arbitrage via SWAPs and most certainly via the alteration of corporate balance sheets by swapping equity for debt.

This dynamic cares not about corporate profits, cares not about earnings per share, cares not about general econ101 principles. For us, QE is at the core of all market valuation and nothing else truly matters. Some time in the future, the debt will matter, sometime in the future the Minsky moment is and always arrives, but rest assure, nobody and we mean nobody knows when that time will come. So here is our chart, our most bullish chart off of what we think is an unstoppable global coordinated QE effort, which was also solidified by the ECB’s commitment this week:

Call us crazy, but after seeing the SP500 run some 200 points this single week alone, we might be crazy but we certainly aren’t fools. Remember we are a mere 5 months off from a presidential election and for those of you that don’t think TRUMP knows full damn well that it’s the economy that will get him reelected and he has unlimited Fed QE bullets to throw at it, and he will.

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.