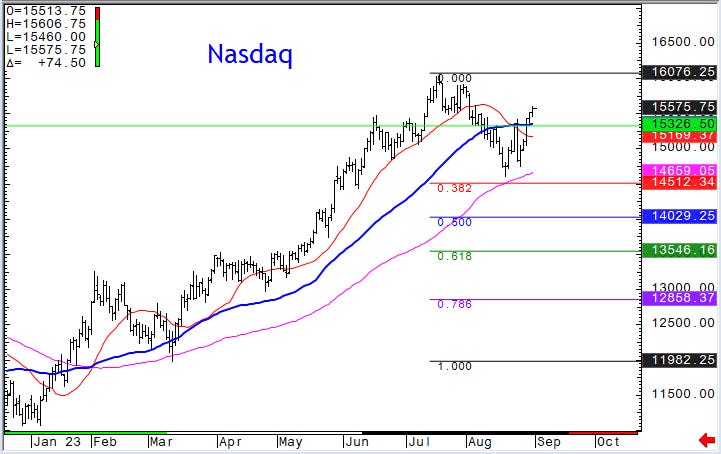

Nasdaq > 15500 Ball in Bulls Court Now

Just a quick post here of our trackers and a current Nasdaq futures chart. The shorts should be capitulating now into month end as the Nasdaq has now retaken the the 15500 level and bulls are hoping the same buyside algo that pushed from March lows is now in play. No doubt the PBOC injections and lower rates are spilling over to fund this new found risk capital being put to work here in US markets. Anyway here is the Nasdaq futures currently:

We will be back later with more, and this mornings Headline PCE number was on the screws at 3.3% YoY. We don’t think this number is as important as the upcoming payroll report tomorrow, so will see what happens. A close back below 15500 for the bears and maintain above for the bulls right now. Month end buying could be the factor here, so we would rather see how tomorrow closes out before saying this current downtrend is over.

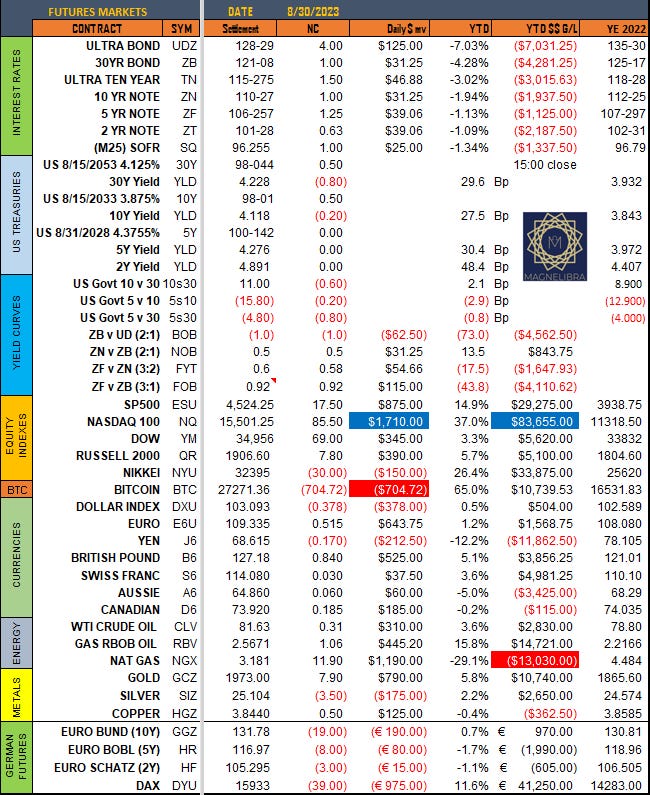

As far as the trackers and settlements from yesterday:

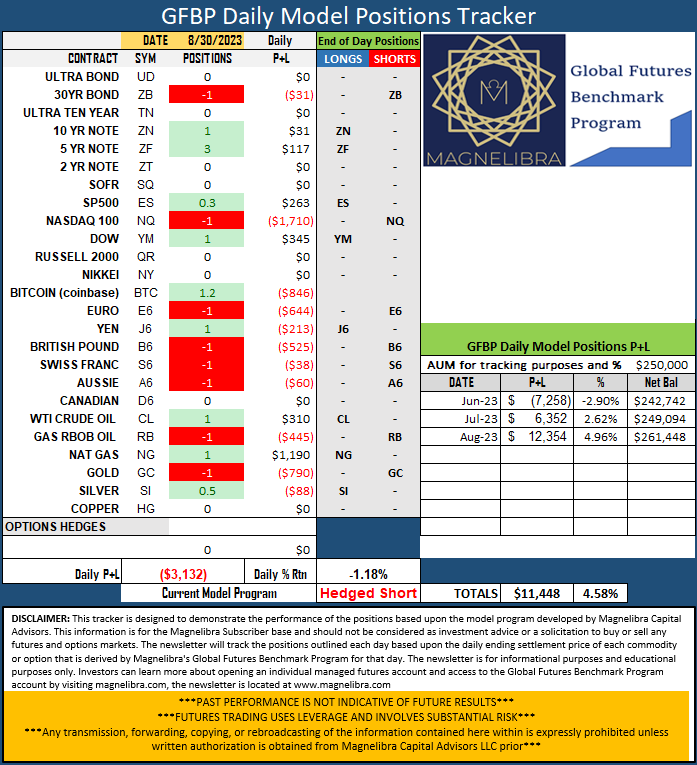

Here is the GFBP with no changes:

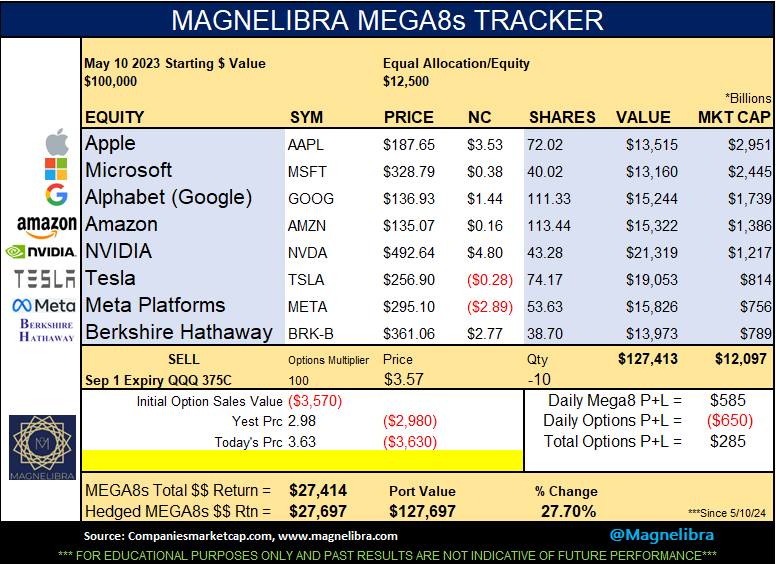

The MEGA8s continue to forge ahead:

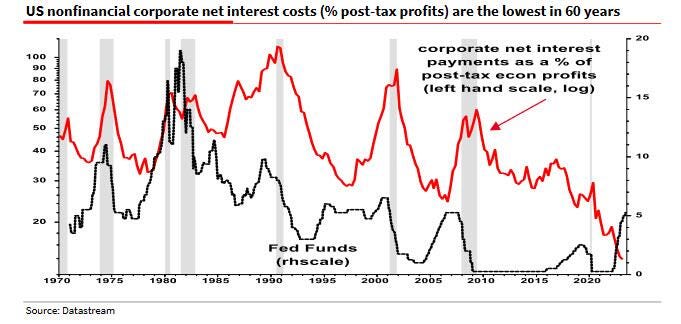

Speaking of MEGA8s, we keep seeing this Albert Edwards chart being tossed around, and we commented on it a few letters back. What it shows is that corporate net interest payments as a % of profits has plunged. This shouldn’t really be surprise considering all the tech MEGA8s that issued debt issued it at longer durations and at super low ZIRP style levels. However that decade is over and any durations post 2020 shorter than 4 years is about to reset and we suspect as the next year rolls on, this red line in the chart will begin its ascent higher once again…Its just too early in the rollover period for most corps, but 2024-2026 will be very different! This does however add to the validation of why the MEGA8s have taken the spotlight and the majority of all the equity gains!

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.