Netflix Earnings and the Apple Problem: Why the Options Crowd May Be Offside

Intuitive Surgical looks spring-loaded, Netflix looks vulnerable, and Apple is quietly winning the room. The Magnelibra straddle read on both prints.

What You Are Reading

Two earnings prints land tonight after the bell. This note pairs the Magnelibra options straddle breakeven analysis for each name with the tape, the positioning read, and where the crowd sits going in. It is educational and hypothetical. Nothing here is a recommendation to buy or sell.

I. Intuitive Surgical: The Oversold Setup

Intuitive Surgical walks into tonight’s print down roughly a third on the year, trading near the bottom of its 52-week range and below its 200-day average. The Street consensus is $2.50 in EPS on $2.81 billion of revenue, a 14 percent earnings gain and a 16 percent revenue gain year over year. The company has beaten estimates in each of the last four quarters, and it carries a positive earnings surprise prediction into the report.

The bull case is straightforward and it aligns with the tape. The selloff has been driven by fear of a da Vinci 5 transition lull and an order air pocket, not by any break in the underlying procedure engine. Procedure growth guidance sits at 13 to 15 percent, first quarter came in at 17, and Japan’s June reimbursement expansion plus tariff relief on gross margin are live upside levers. When a durable compounder gets sold this hard into a quarter it has historically beaten, the risk skews toward a relief pop on any in-line-to-better result and, more importantly, a constructive outlook.

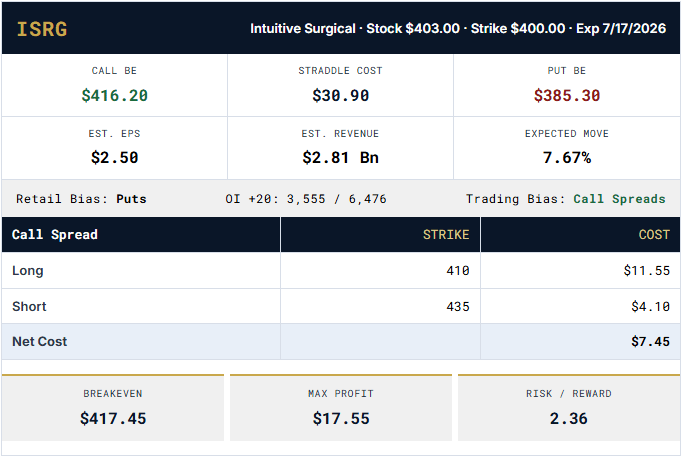

ISRG weekly. Price has retraced the entire 2024 to 2025 advance and sits in the marked Call Spread Zone near 400 to 420, back at the rising long-term moving average that guided the prior leg higher. The 7.67 percent implied move frames the night: a defended 400 strike is the line that matters.

Options Straddle Breakeven · ISRG

The Magnelibra read: the straddle prices a 7.67 percent move, with call breakeven at 416.20 and put breakeven at 385.30. Open interest tilts to the put side in raw count, which is the tell. That is not a directional bet against the stock so much as long holders paying for downside insurance into the event, classic behavior in a name that has already been punished and whose base is nervous about the transition. Heavy protective put positioning into a beaten-down quality name is often a contrarian positive: the downside is pre-hedged, so a clean number releases the coiled spring.

The 410 / 435 call spread expresses the pop thesis with defined risk: $7.45 net cost, breakeven at 417.45, max profit $17.55, a 2.36 reward-to-risk. It needs the relief rally the setup argues for without requiring a return to the old highs. The structure caps the pain if the order-air-pocket fear proves real and the outlook disappoints.

Where the Crowd Sits · ISRG

Sell-side price targets were cut across the board into the print (RBC to 600, TD Cowen to 520, BTIG to 512, Mizuho to 500), yet the ratings stayed at Buy and Outperform. That combination, lower targets but intact conviction, is the signature of analysts de-risking their numbers while refusing to abandon the thesis. Goldman published a note arguing the crowd is wrong on the name. Insider selling of roughly $3.1M over three months is a mild offset. Retail chatter skews cautious, which is the fuel for a squeeze if the number clears.

Net: A stock the market has already sold, a quarter it usually beats, and a base that has bought its own insurance. The asymmetry favors the upside surprise.

II. Netflix: Sold, But Not Yet Bought

Netflix comes in beaten down but for a different reason, and with a different resolution. The stock is off roughly 40 percent over the past year and more than 20 percent year to date, having hit an 18-month low in June. Consensus is $0.79 in EPS on $12.57 billion of revenue, about 14 percent top-line growth. The company no longer discloses subscriber counts, so the tape will trade off revenue, operating margin, ad-tier progress, and forward guidance rather than a headline number.

The problem is not the model, it is the mood. Engagement is the overhang: total time spent watching Netflix grew under 2 percent last year, and reports of steep season-over-season viewership drop-offs have fed a narrative that the content slate is thinning even as spend stays elevated. Management’s answer is the ad tier (past 250 million monthly active users, targeting a doubling to roughly $3 billion in 2026) and a raised free cash flow outlook near $12.5 billion. The bull case is a genuine valuation dislocation. The bear case is that engagement softness and first-half-weighted content amortization compress margins while the crowd waits for a catalyst that this quarter may not deliver.

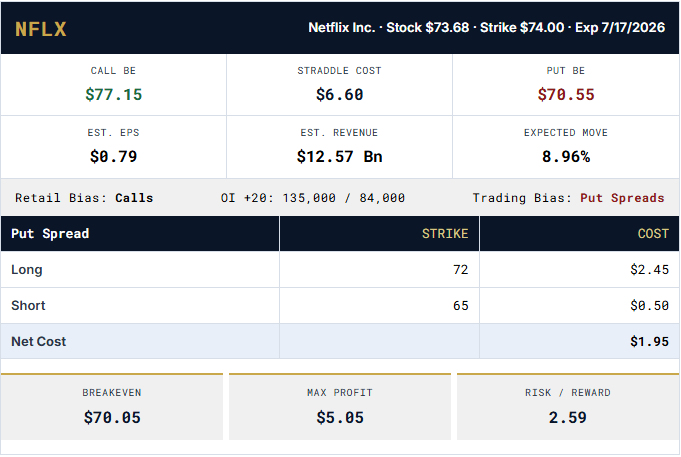

NFLX weekly with the Fibonacci retracement of the entire 2022 to 2025 advance. Price has sliced through the 0.5 level at 75.14 and sits mid-channel with no clean bounce yet established. The 0.618 at 61.23 is the next structural shelf below; 89.05 is the first real resistance above. The 8.96 percent implied move is wide enough to reach either.

Options Straddle Breakeven · NFLX

The Magnelibra read: the straddle prices an 8.96 percent move, call breakeven 77.15, put breakeven 70.55. Here the open interest tilts the other way, toward calls (135,000 versus 84,000 on the +20 strikes), and retail bias reads Calls. That is the mirror image of ISRG. Where Intuitive’s base is buying protection into weakness, Netflix’s crowd is reaching for upside into a downtrend that has not yet turned. Retail calls stacked against an unbroken downtrend is the more dangerous posture: it is hope positioning, and it tends to get punished when a beaten stock delivers an in-line print with no forward catalyst.

The 72 / 65 put spread is the defined-risk expression of the cautious view: $1.95 net cost, breakeven 70.05, max profit $5.05, a 2.59 reward-to-risk. It profits if the no-bounce tape resolves lower on soft engagement commentary or guidance, and it caps the loss if the dislocation-value bulls are right and the stock gaps up.

The Content Question: Apple Is Winning the Room

The editorial overlay worth stating plainly: the competitive pressure on Netflix is real and it is showing up where it matters, in prestige and in mindshare. At the 2026 Emmys, Apple TV+ landed three nominations each in both Outstanding Drama and Outstanding Comedy on the strength of Pluribus, Slow Horses, Your Friends and Neighbors, Shrinking, and the summer breakout Widow’s Bay. (Widow’s Bay, is one of our favs of the year!) Netflix, despite a far deeper catalog and 111 total nominations, managed one apiece in the marquee series categories. Apple’s Severance drove a reported 126 percent surge in new subscribers, the kind of single-title gravity Netflix has struggled to manufacture lately.

The strategic contrast is stark. Apple chose quality over volume, gave A-list creators budget and freedom, and built a prestige identity that now pulls hardware buyers into the ecosystem. Netflix chose scale, and is now visibly pivoting toward cheaper filler, licensed library content, and live programming to defend engagement, while leaning on advertising to defend the model. One of those strategies is accreting brand equity. The other is defending a lead. That does not make Netflix a short into a single print, the cash generation is formidable and the ad ramp is real, but it does explain why the stock has found sellers and not yet found buyers, and why the burden of proof tonight sits with management.

Apple, for its part, is doing the opposite of struggling. The stock has been among the strongest large-caps of the year, trading up through its bull-bear pivot near 290 and pressing new highs, with the content business now a genuine ecosystem asset rather than a cost center. The read-through is not that Netflix breaks tonight, it is that the secular content narrative has quietly shifted, and a beaten stock carrying a hopeful call-heavy crowd is the wrong side of that shift to be long into an event.

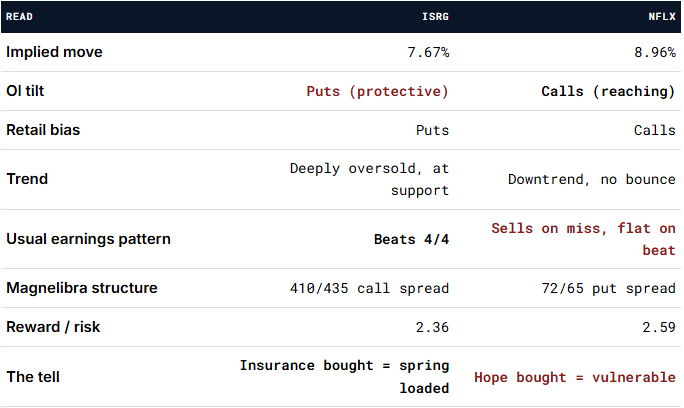

III. The Two Setups, Side by Side

The pairing is almost a matched set. Intuitive is the beaten quality name whose own holders have pre-hedged the downside, setting up a relief move on any decent number and outlook, the pop you flagged. Netflix is the beaten name whose crowd is leaning the wrong way, long calls into a tape that has sold off and not recovered, against a competitor that is visibly winning the content war. One setup rewards the contrarian long. The other rewards patience and a defined-risk fade. Both trade tonight.