ONE AND THE SAME

The obvious highlight of last week was the long anticipated rate hike out of the FED. The move was highly anticipated and certainly priced into the Fed Funds markets and the FED did not disappoint. They raised the target range ceiling to 1.25%. We aren't truly in agreement with the move as we feel the data does not support their decision. That is unless they are targeting asset prices and feel that they need to stem the tide of appreciation and speculation. The FED has long said that they do not target asset prices but rather opt to maintain their dual mandate of price stability and maximum employment. We do know one thing is certain, that each rate hike raises the subsidy to the banking sector and considering a 1.25% cap, this means an extra $30 billion a year to those banking institutions. We find it very curious as to why the FED is still using IOER. We have yet to hear a plausible answer and we can't fathom a reason why they would reduce their balance sheet while still paying this subsidy. If there are any persons out there privy to such an answer, we would love to hear it. The fact of the matter is and for us, we view this hawkish FED tone as nothing more than misdirection. They aren't really changing the landscape that much as their overseas cohorts are still heavily printing to the tune of around $200 billion a month. This is absolutely ludicrous and we aren't really sure why the media doesn't question the FED's motives just a little bit more. As we have written many times the central banks work in coordination and for the FED to hike rates and to contemplate a reduced balance sheet is nothing more than trying to regain credibility. For us its mere conjecture, a theory based loosely upon reality and more so on the hope that nobody notices the wizard behind the curtain. We laugh at the distortions all of this crazy central banking has created and it has made us look at the entire financial landscape as if anything and everything is possible. Meaning arguments can be made for asset prices to continue to sky rocket and arguments can be made for them to collapse. So how does one position themselves given these uncertainties? Well, that's the Trillion dollar question.

Given this central bank manipulation it has forced us to contemplate the quantity theory of money lately or this equation M x V= P x T. The Fed thinks that It can control such variables to neutralize any undetermined negative out come. We beg to differ and we feel that no matter what level of aggregate monetary base the FED creates, it will not be able to shift the left side of the equation. Meaning if the FED increases M2 it will not necessarily spill over into an increase in nominal GDP. What if the equation does not take into consideration the fact that an increase in M2 might not equal out to an increase in nominal GDP? What if the money created just sits in the coffers of the already ultra wealthy to await a better optimal investment environment? What if the financial game is no longer zero sum? Has the FED not contemplated such a scenario?

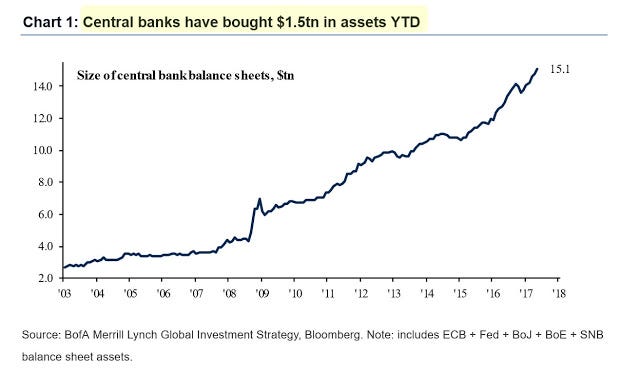

As we have written many times in the past, the fact that central banks are now in the business of printing money just to buy assets means they are nothing more than counterfeiters. Is it us or does nobody realize how difficult it is too play a game against an entity that has unlimited financial resources? Doesn't anybody realize that if an entity such as a central bank is allowed to print and buy private assets that it erases competition and distorts financial price discovery. For all intents and purposes, the central banks not only control the pricing mechanism, but actually they become the market itself. We feel even the great investors of our time have had a hard time figuring this fact out. They are slowly realizing the devastating mechanics of QE and central banking in general. The tipping point was 2008 and as Bernanke was fully aware, either quadruple the balance sheet or risk a depression. What he didn't say was that once that seal was broken, there would be no way back. The markets and the central banks are now effectively one and the same. To highlight this point, we have this chart from BofA:

In a mere 5 months central banks have bought $1.5 Trillion in assets. Does this sound like an environment by which the FED should be hiking rates? Or is there an ulterior motive? If so what is that motive? To make the US more attractive for capital? To pay higher subsidies to the banks to shore up balance sheets? Rest assure these are the types of questions investors should be contemplating and we hate to say it, but there aren't easy answers, this we are certain.

Too see a little bit of the distortions that we speak of, let's take for instance a topic in which we just wrote about a few weeks back. We were dumbfounded about the risks some entities were willing to take in order to expand their presence in the grocery store space. All around Chicago land grocery stores were springing up, old ones were being renovated and we wondered how in such a tight margined business is all of this possible. Then we figured that too much money is being made by the larger and bigger players and growth via acquisition is leading to a systemic overhaul across the entire industry. Artificially low interest rates, leads to cheaper debt issuance and higher asset prices leads to generally a more stable collateral base. Of course none of this would be possible without the central banks manipulation. We just couldn't imagine the thought process behind issuing debt to open more stores just to make availability more accessible if you will.

One thing we do understand is that the two tiered economy, one in which we describe simply as those that can afford to eat out and those that cannot is having a profound effect upon the food distribution business. It is becoming apparent that with this never ending disparity of income and gutting of the middle class, there seems to be a tremendous battle going on for both the top tier and the bottom tier customers. On the hunt for the bottom rungs we have Walmart being peppered by the German imports of Aldi and Lidl. The upper echelon and niche businesses of Trader Joe's and Whole Foods are fighting for the more affluent buying crowd. Now enter with this week's news that Amazon is about to pay $13.4 billion for Whole Foods and now the whole industry is going to see major disruptions. As if the likes of Kroger and Albertsons weren't already nervous. Who would of thought Amazon would buy Whole Foods at a crazy multiple over their prevailing price? Well private equity might have their own say, but we would say it’s a very smart move to capture the ongoing consumer shift to a more convenient access point to the things they need most. If we were the big guns of the consumer grocery store chains, we would be very nervous of Amazon's intentions. They plan on streamlining the experience to the point by which they know your habits almost better than you do. Hey we don't blame them for trying to make your life easier, but we do continue to question their overall EXTENSION into your personal shopping experience. We would like to think the antitrust part of the government might have some say so, yet we feel governments are no match for the corporations, so just adjust and be done with it.

We figured Amazon is going to be able to tap into a more stable wealthier customer base and streamline their experience. Obviously this will all tie in well with their current Amazon Prime customer base and now this gives them an even larger direct distribution space. As far as streamlining, rest assure automation is at hand and a more unique buyer specific experience will be at the fore front. So imagine instead of wasting time to go out to shop for food, Amazon will deliver it free to your doorstep in less than 2 hours. We don't think it will take very long for Amazon to reap the rewards of this purchase, but one thing is certain, the grocery business will never be the same.

With another eventful week behind us and summer in full swing, let's check the charts to see if we can ascertain some trends at least. Considering the hawkish FED and their rhetoric to raise and even shrink a balance sheet, (which we know full well they cannot do, not at least without a corresponding expansion of balance sheet via some other central bank) we figured the US curves would continue to weaken. The US 2s10 yield curve which continues to compress lower, is still above its 2016 lows:

The US 5s30 has broken a key trend line and is now below 105 bp, currently 99 bp.

As far as the US 30 Year its yields are hovering at 2.78%

Moving over to equity land Goldman Sachs analysts put out a bearish piece on the coveted FAANG stocks last week which lead to a tech selloff which saw the broader SP500 benefit:

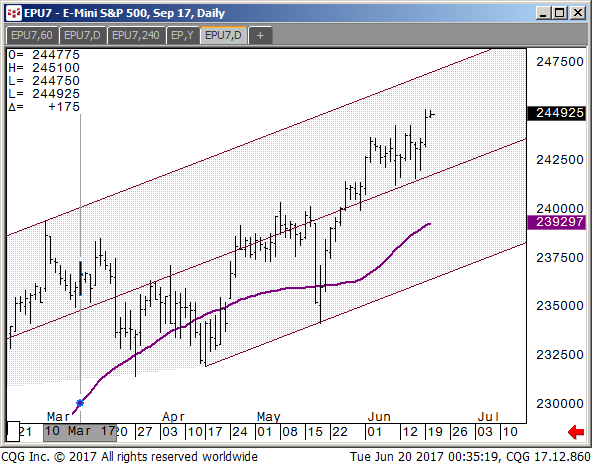

Speaking of the SP500 it continues to chug along and targets new highs on a monthly basis:

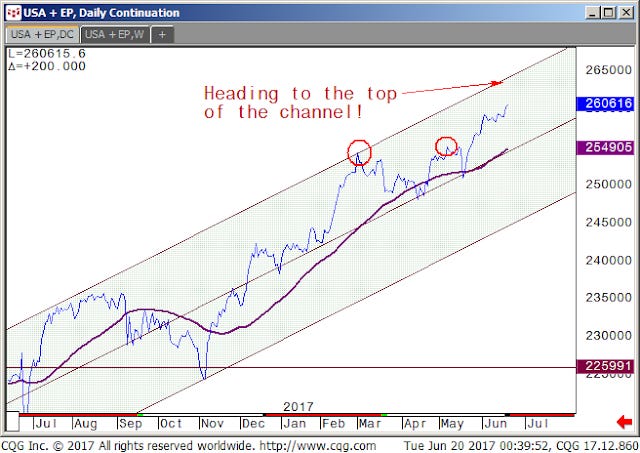

As far as our reflation chart, the combined SP500 with the 30 Year Bond future is still constructive toward the top of our channel:

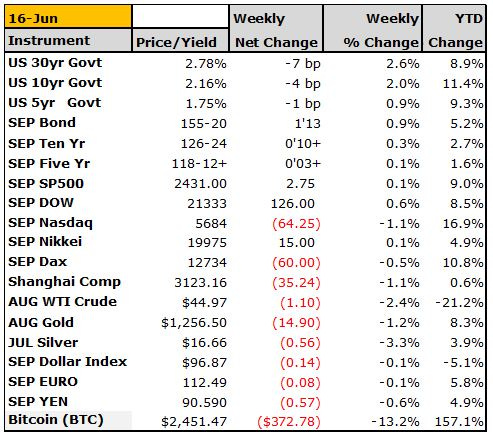

Finally we leave you with the weekly settles. Nasdaq still the leader but damage and asset reallocation may prove to be the turning point there verse the other indexes. The techs are still heavily overcrowded, yet they are supported by those non-zero sum players the central banks and sovereign wealth funds, so downside is most likely limited there. Crude continues its terrible year and Bitcoin gave some back this week after its huge run up. All in all, with summer in full swing we expect doldrums with periods of increased vol, which will most likely be met with further vol crushing strategies on the heels of a more supportive global central bank accommodation. Cheers!