Powell Speech 1:30pm Est.

Technical Charts

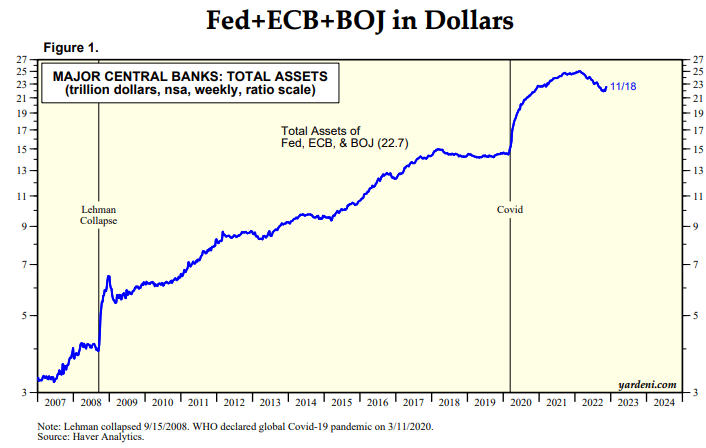

The markets are awaiting Powell’s speech today which takes place in DC at 1:30pm. We know that Powell has reiterated a more hawkish tone and as we have opined before, this is what we expect, he has to talk the talk if he is going to walk the walk. Remember readers when it comes to inflation, its the “expectation” or general consensus going forward when it comes to inflation expectations that they really need to corral. We also know this much debt in the system is actually massively deflationary as the burden of the debt tends to erode investor and business flexibility and any downturn in global economies will destroy the repayments theme. This is why QE is so important and has been the tool of choice for global central bankers over the last decade or so. We do not view QE as some magic growth tool, what it does is it merely BUYS TIME. If QE was the cure all then every global central bank would employ it and believe us, they definitely try too as this chart clearly points out:

Since 2020 these 3 central banks have increased their assets by $8T dollars or an increase of 53.3% in just over 2 years. No matter what the global circumstances Covid whatever, the facts prove QE is their only tool right now. Why wouldn’t we expect an inflationary lag by about 18 months when you drill this much fiat down everyone’s throats, well not everyone, first to the spigot Investment Banks of course who lever it to the hilt. Where is the empirical evidence that QE works better than no QE?

The Hegelian Dialectic seems to be used over and over again, problem - reaction - solution…Anytime we need a big influx of fiat to cover our systemic problems, well voila, some sort of economic calamity, its almost amazing. This isn’t the free market capitalism by any means, this is a hijacked rigged system requiring QE4EVR!

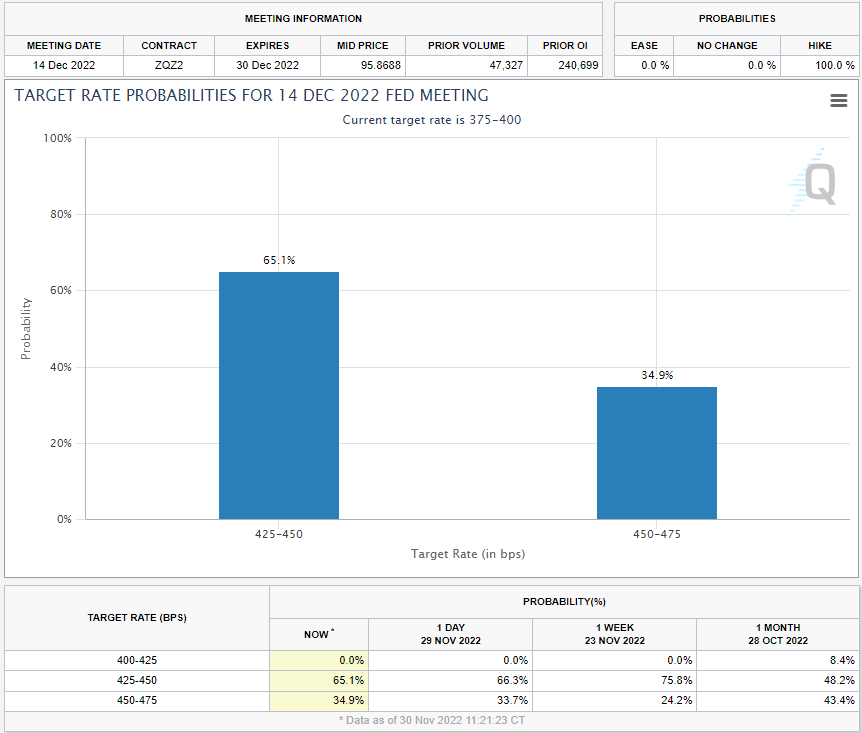

Ok So what will Powell do today? Most likely he will continue a hawkish tone as he can’t put his tail between the legs just yet, although we know he wants too. So let’s look at market expectations right now for the December FOMC:

Market participants are leaning 65.1% toward a 50bp hike. On October 20th, the expectation was for a 75% chance of a 75bp hike, so you can see already the market is front running the FOMC and signaling that the FOMC will pivot sooner than they want too. We believe as you know that December will be the last rate hike of this cycle. We believe that the global inverted yield curves will usher in a full blown recession come 8-12 months from now as the economy churns sideways to lower and the effects of higher interest rates crushes inflation, crushes economic demand and leads to a wave of defaults on all sorts of debt come Q2 2023.

So Powell will continue to speak his rhetoric and will avoid any comment on global inverted yield curves as he knows the truth of what they foretell but has to tow the company line. So where do the markets stand right now?

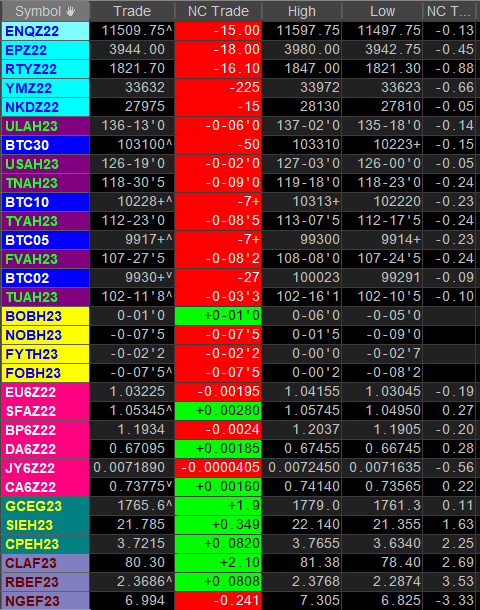

Equities are a bit lower with the Russell2k leading the way down

Bonds yields slightly higher with the front of the curve getting hit the hardest

US Dollar is mixed as its weaker against SF and AD but stronger vs EU, BP & JY

Metals strong across the board with Copper leading the charge

Energies strong with Nat Gas lagging:

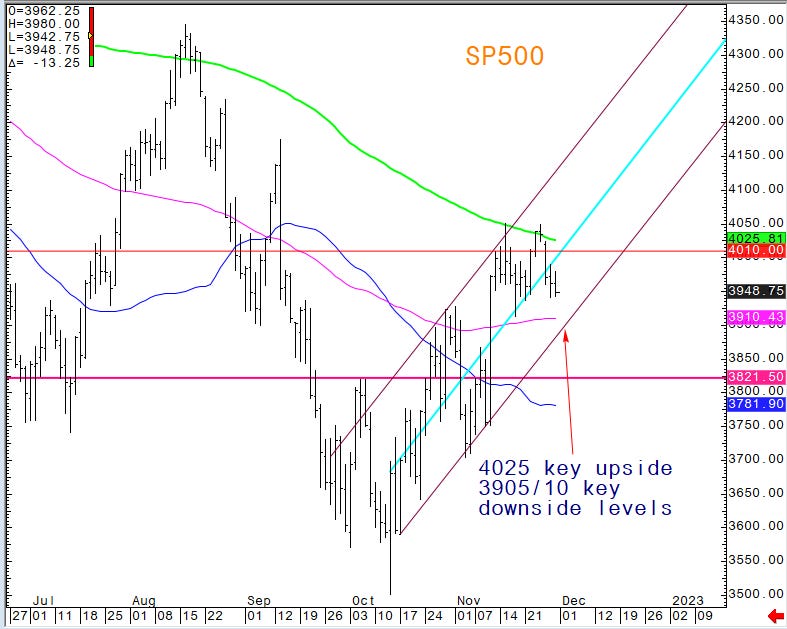

The SP500 has the 4025 high target as key resistance and bulls will look to hold any test of the Vwap down at 3910/05 area. A close below there would usher in some bearish reversal patterns and would most likely lead to further probes south:

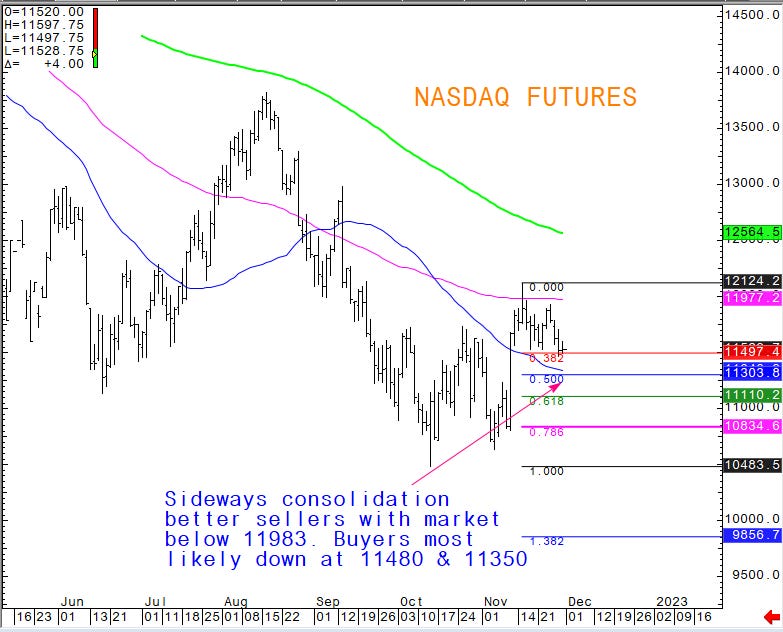

As far as the Nasdaq, 11480 is key a trade below there of any significant time scale 30 min or hourly and we would lean toward a probe down to 11350. Close below there and you target 11110:

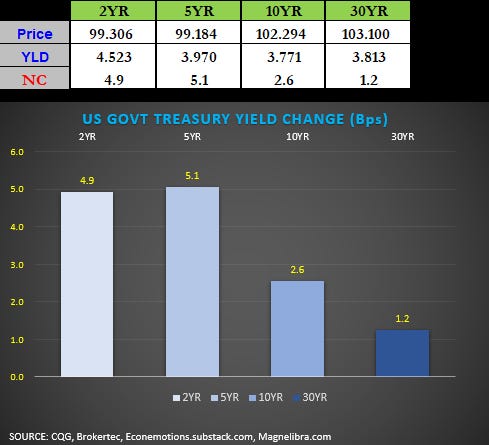

Bond yields higher led by the US Govt 2Y note today +4.9bp seems like a few accounts lightening up on a few steep yield curve plays:

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Econemotions covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2022