Profit Taking in US Curve & Equities Bid PreFOMC

Unchained Podcast must watch

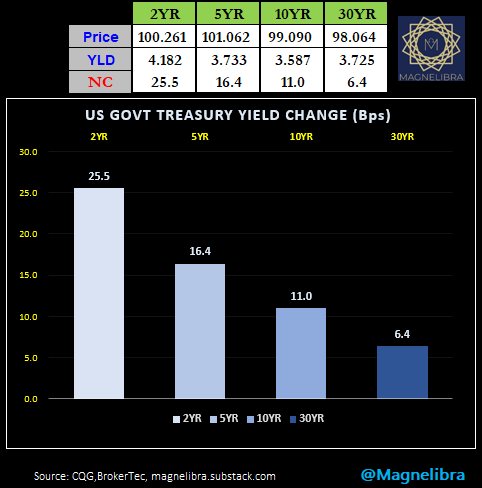

We are seeing profit taking in the US Treasuries pre FOMC decision. This is the normal course of action, especially after we have seen a record drop in the 2Y yields from 5.12% down to <4% and now sitting at 4.18%. The curve is flattening out with 2Y yields rising 25.5bp while the US Govt 30Y is +6.4bp:

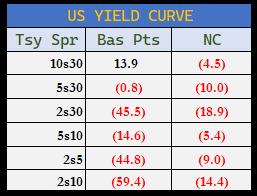

The yield curve indicative of the 5s30 spread is now back inverted at -0.8bp as its given up 10bp on the day.

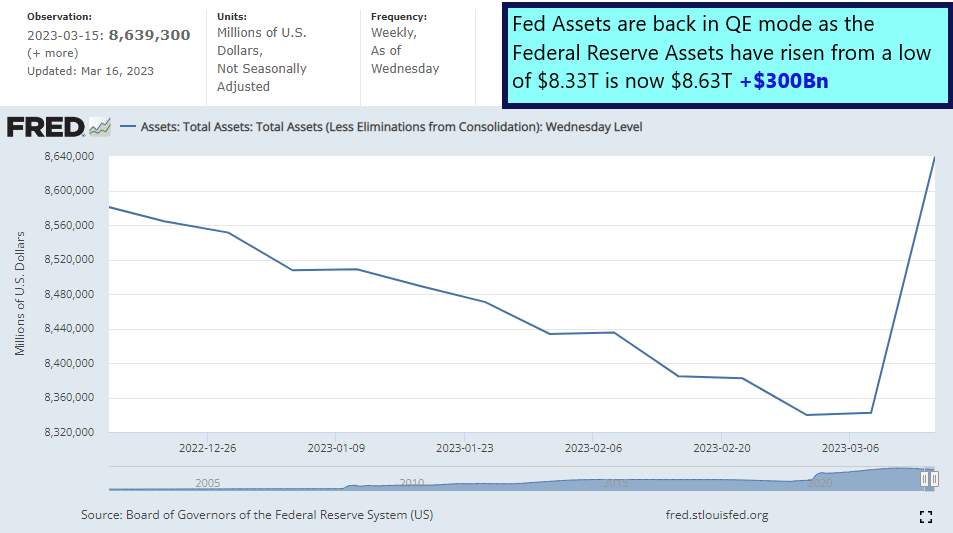

The equity markets are higher on the day as QE is back in vogue, expanding balance sheets is back in business and the FOMC is going to pause and reverse…or so investors think. Here is the latest chart from FRED in regards to FED assets:

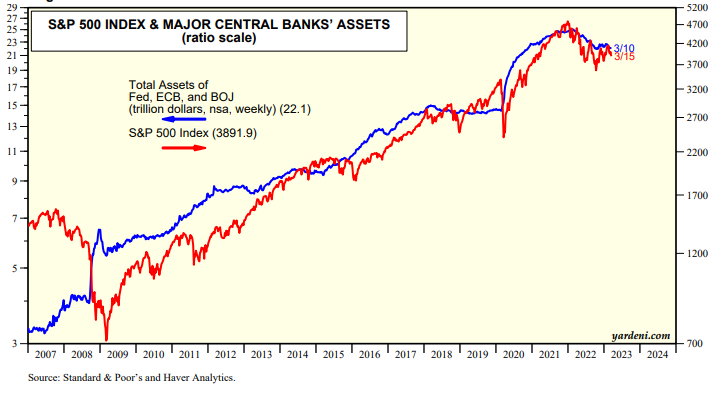

Given the fact that the correlation between expanding central bank balance sheets and equity prices, well, here is the most recent research out of Yardeni on the SP500 vs Major Central Bank Assets:

One thing I want to point out to Magnelibra readers is that in 2008 and in 2015 we saw balance sheets expand but the market went lower. We do feel that many are very complacent here and are relying on this QE as having the same potency on rising asset prices. However we aren’t so certain, we feel that the global treasury curves are telling us there are major liquidity issues and the measures central banks are taking now are sowing the seeds for some very major dislocations and asymmetrical moves. We have highlighted this fact that equities really start to sell off only after the first rate cut, historically.

In regards, to today’s action, in the Nasdaq June Futures, we did notice a decent amount of volume just recently up at 12812, so someone is selling this level and we suspect a battle here at this area:

The global central banks are trying to save a system that cannot operate in the frictionless digital monetary future. We know this , we have been saying this and now their concentration of wealth, which is the real result of all of this is in direct violation of Section 165 Sub Chp. C of Dodd-Frank. We know the regulators will turn a blind eye because they are in damage control and that’s all that matters. We also know that they are directly trying to impede the decentralized digital currency world, and desperately so as more are catching on that the US Banks cannot payout everyone, they cannot even payout 10% of the depositors and that is inherent of this system. The larger the FOMC balance sheet grows the worse the problem becomes, and the more obvious the problems will continue with both speed and repetition.

With this sentiment in mind and what has become blatantly obvious, is that there is a massive coordinated effort from our current administration, the Federal Reserve, SEC, FDIC and US Treasury to deny any institution, to debank the digital currency industry. In the recent Unchained Podcast, Laura Shin, discusses with Caitlin Long CEO of Custodia Bank and Meltem Demirors of Coinshares. We feel that if you really want to know what is going on, including the most recent banking woes, then this is a very relevant podcast. If you ever wonder how or why we are seeing massive interventions in the banking industry right now, trying to cover up this fractional reserve mess, well then you have to get informed as to the battle between traditional banking and the future of money, which we believe will be decentralized networks like Bitcoin. Anyway give this a listen, Laura Shin Unchained Podcast

With that let’s look at Bitcoin which is now back at the prior 0.618 near $28700 but we feel that the resistance ceiling is up at $36k:

Alright, so the decision is tomorrow, we will be back afterwards with the results and aftermath and we hope that someone at the press conference can at least ask some real questions to J Powell! We won’t hold our breath though.

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023