Quick Note-10Y Futures CTA Analysis

We were reading the article on Zhedge today talking about the CTA positioning in the US Ten Year markets, it was referencing a quant at Nomura, Masanari Takada. He highlighted the levels by which he feels CTAs may accelerate the US Govts 10Y yields higher, in which he pointed out the 1.02% level.

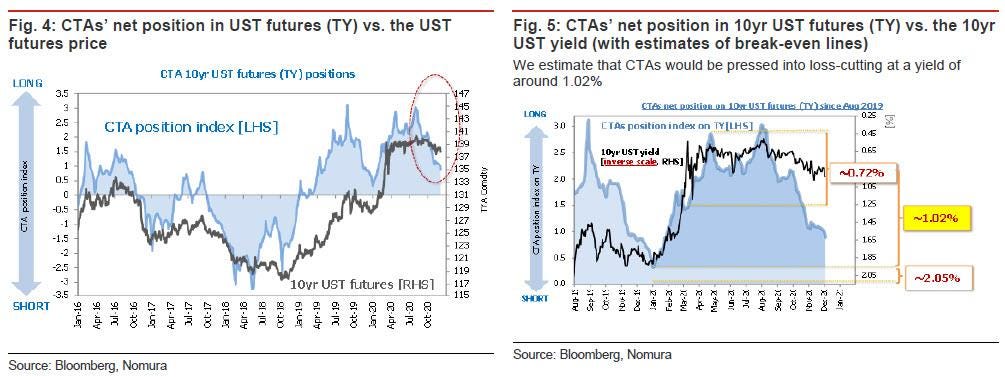

We noticed he put up a futures positioning chart vs the yields chart…Now as a long time fixed income arb, when we look at US Ten Yr Futures positioning, yes CTAs most likely are trend followers and will chase, chase and exit at extreme points. However we have to be cognizant of those players that arbitrage “basis” or US Govt cash vs futures. For me I think they have a very large influence on flows as do the curve or duration spread traders that are taking steepening/flattening bets.

So, our biggest question then is, how tight is the CTAs correlation with positioning and yields? He did post this chart:

From what we can tell the CTAs positioning since August has gone from a +3.0 to just under +1.0. However yields have moved maybe 20/25bp. For me it doesn’t seem like the CTAs will be the one’s accelerating the move up to 1.02% rather they may just be the ones to start to once again buy or accumulate.

Now from his chart on the upper left, he is highlighting the fact that in the futures the CTAs selling has not led to a big downturn in the price of the US Ten Year Futures. So what gives?

Well back to my first point about duration curve spread players and Basis Arbs. There are a lot of large investors/funds/RV that will continue to support US yields especially the long end of the short end, that which is the 10YR sector.

So we don’t agree that the CTAs will accelerate things here, rather and we would suspect the recent swath of large 10Y options strangles bracketing the 1%/0.65% area. We are certain that player would agree that it will take something pretty big to move the US 10YR past 1.02% or even below 0.65% again.

For now we feel the range has pretty much been established.

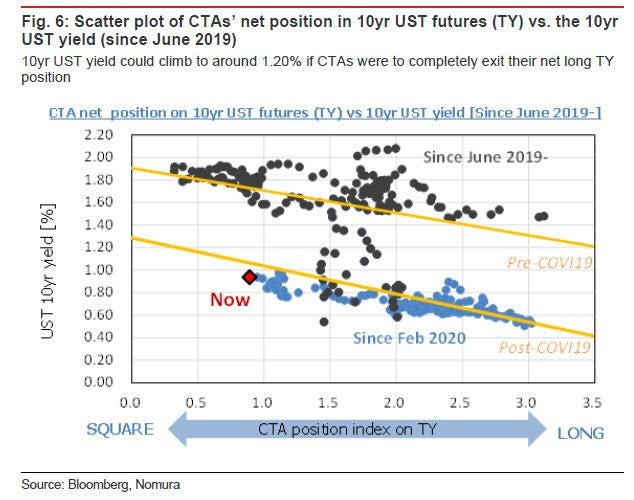

Takada also posted this chart:

Now you can see the Red Square current positioning, for us, we would suspect that CTA’s would be more inclined to start accumulating at the current levels rather than selling into a break of current levels. The risk/reward, as well as history is not on their side, but we digress, maybe some trend/momo types might, but we would rather suspect that trade would be very short lived, especially considering we don’t have a president elect and covid continues to press on.

Speaking of Covid, we don’t quite understand why the large push for mandatory mass vaccines continues despite the 99.97% recovery rate? Now we hear of immunization cards and not being able to travel? Hmm the logic in us tells us that there is more to this story!

The fact that the demographic most adversly effected by Covid is primarily (83% in fact) over 60 years old. Sure they could benefit from a vaccine, but mass vaccination? Hmm, especially an mRNA fast tracked one? Well us meager humans at Magnelbira Econemotions would like a bit more cost/benefit analysis before we become lab test subjects.

Anyway its clear that what is going on around the world might not be about Covid, but rather a larger much more extensive trample upon civil rights and individual freedoms. One which we don’t think will occur without a substantial backlash and fight, as if the mass protests around the globe aren’t evidence enough!

Anyway just wanted to go over the Takada analysis with our subscribers. We hope you learned something, we hope you share and continue to support our work! We sure cold use the help!

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.