Raising Fed Funds and QE Together!

We wrote a whole piece last night on our Substack but it did not save…so goes it sometimes and to be honest, when these things happen, we don’t get upset, rather we take it as it just wasn’t meant to be.

Anyhow we know the gist of our topic was the FOMC decision and not that they actually went 25bp, but rather the fact that Powell basically dodged every question possible about the future of tightening in the midst of the current banking crisis. He noted at the start of his speech that they are working alongside, US Treasury and FDIC departments to ensure the crisis doesn’t spread. However we do not understand the rhetoric that things are data dependent and inflation is still their number one problem. He said,

“Inflation remains too high and the labor market continues to be very tight.”

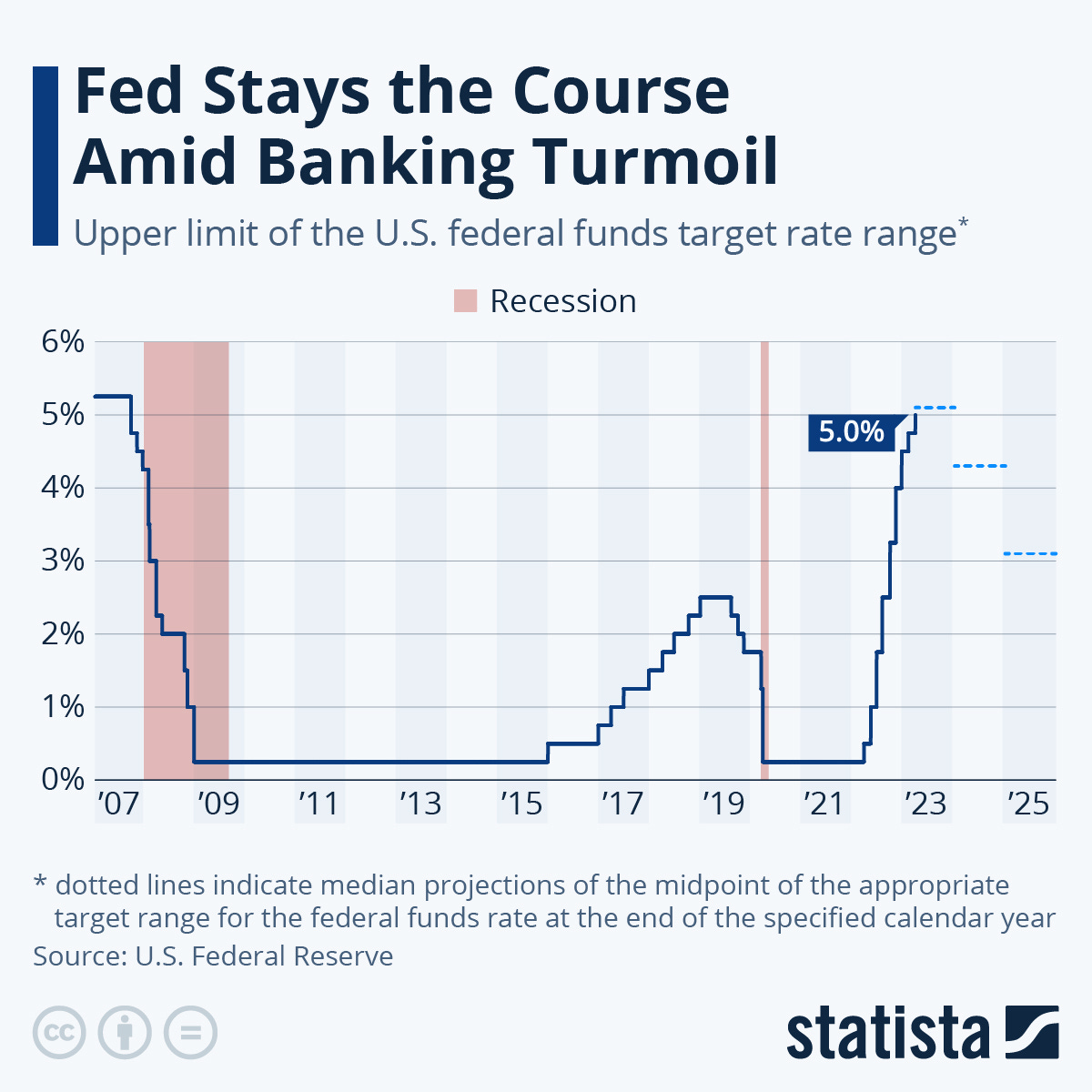

We like JPowell’s commitment, will give him that and this chart does do a good job of displaying that commitment as the Fed Funds is now at multi-decadal highs. Notice the anticipated future path of lower rates though. The global bond markets seem to think the FOMC is not going to stay up here for very long:

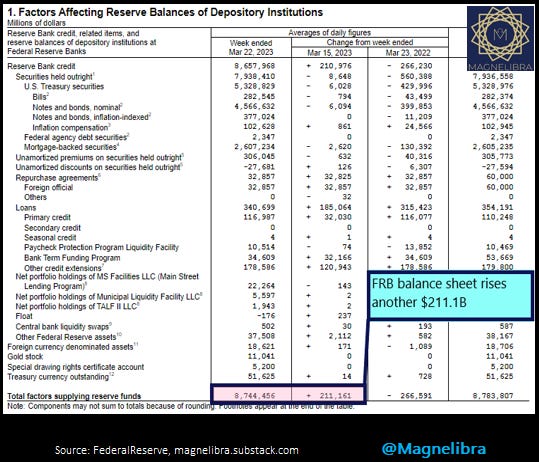

We suspect that we will see lower yields and a restart of QE in no time and nothing in the FOMCs balance sheet signifies that they are really concerned about price inflation. We have noted the annualized growth rate of the FOMCs balance sheet stands at a hefty 12% annualized over the last 25 years. Nothing in that is a recipe for keeping inflation down, especially in regards to asset prices. In fact today’s H4 shows another chunky $211B increase with the FRB balance sheet climbing to $8.74 T:

We know that inflation is a devaluation of ones nominal wage earnings, especially their net earnings or disposable income. This is the real problem and as the FOMC claims they fight inflation, in reality they are the single leading source of it, via their monetary leverage transmission mechanism.

This mechanism funds the ultra wealthy machine indirectly by offering a direct conduit to consistent capital that is then used via leverage to pay ever and ever increasing prices for assets like real estate and equities. The general economy does not see the bulk benefit of this, rather what happens to the general population is that they are priced out of these products, forced to take on more debt just to survive and in some cases, perpetually paying up for the single most important necessity that exists and that is shelter.

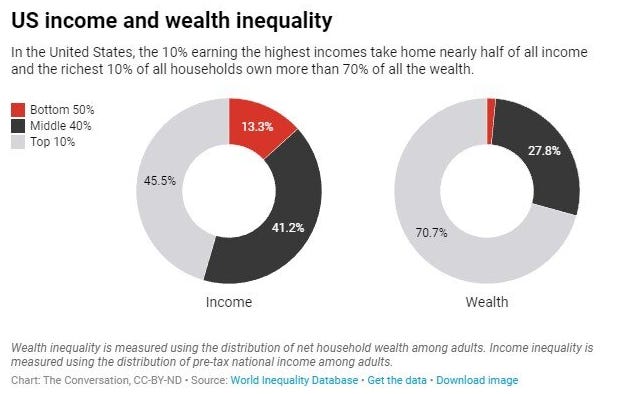

You see the fallacy of the FOMCs monetary machine is that it spreads symmetrically throughout the general economy. There is nothing further from the truth than that and the only data point needed is the fact that income inequality is at record proportions. Did you know that the top 10% of households hold 70% of the wealth in this country and the top 1% own hold 15 times more than the bottom 50%!

With this in mind and considering the graphic above, we often heat how inflation of the 1970s is akin to today’s inflation, well think of it in another way. Considering that in 1970 the top 1% owned 8 times more of the total wealth than the bottom 50%, today they own 2x that, meaning there was a greater overall wealth distribution profile or dispersion of income in the 1970s.

This means more people had the capacity to survive the high inflation. Fast forward today and you can see that Main Street suffers far more severely than in the 1970s. We will here that credit access is greater now than back then, and yes this is true, however debt problems do not solve inflation problems, as eventually you are surviving but with the greater cost due to the interest and greater indebtedness eventually leaving you worse off than before.

So with that said, we understand the FOMC and the rest of the global central banks that have raised rates this week. They are correct to be concerned about sticky inflation, yet they are not appropriately attacking the source. The source is the balance sheet and their 12% annualized growth. The distortions this is creating continue to be compounded year after year after year.

We see the fruits of this expansion in the form of asymmetrical risk taken on by the very institutions entrusted with the fiduciary responsibility of protecting investors, depositors etc. Each and every time and with every decade that passes, the structural imbalances are combated with one policy and one policy only and that is Quantitative Easing.

This solution is also the problem and we aren’t sure why the central banks continue this charade, but we are certain that true anti inflationary money like Bitcoin will continue to be enemy number one. It has become so obvious the governments attempts to not only coopt this movement, via FTX and the like, and these desperate measures by the regulators fail to realize that Bitcoin is not a domestic U.S. issue, rather its global and the efforts here only hurt innovation and necessary change. The fact that they deny Custodia Bank a license is a testament to their conviction but also exposes the fact that their system is dysfunctional but will be protected at all costs.

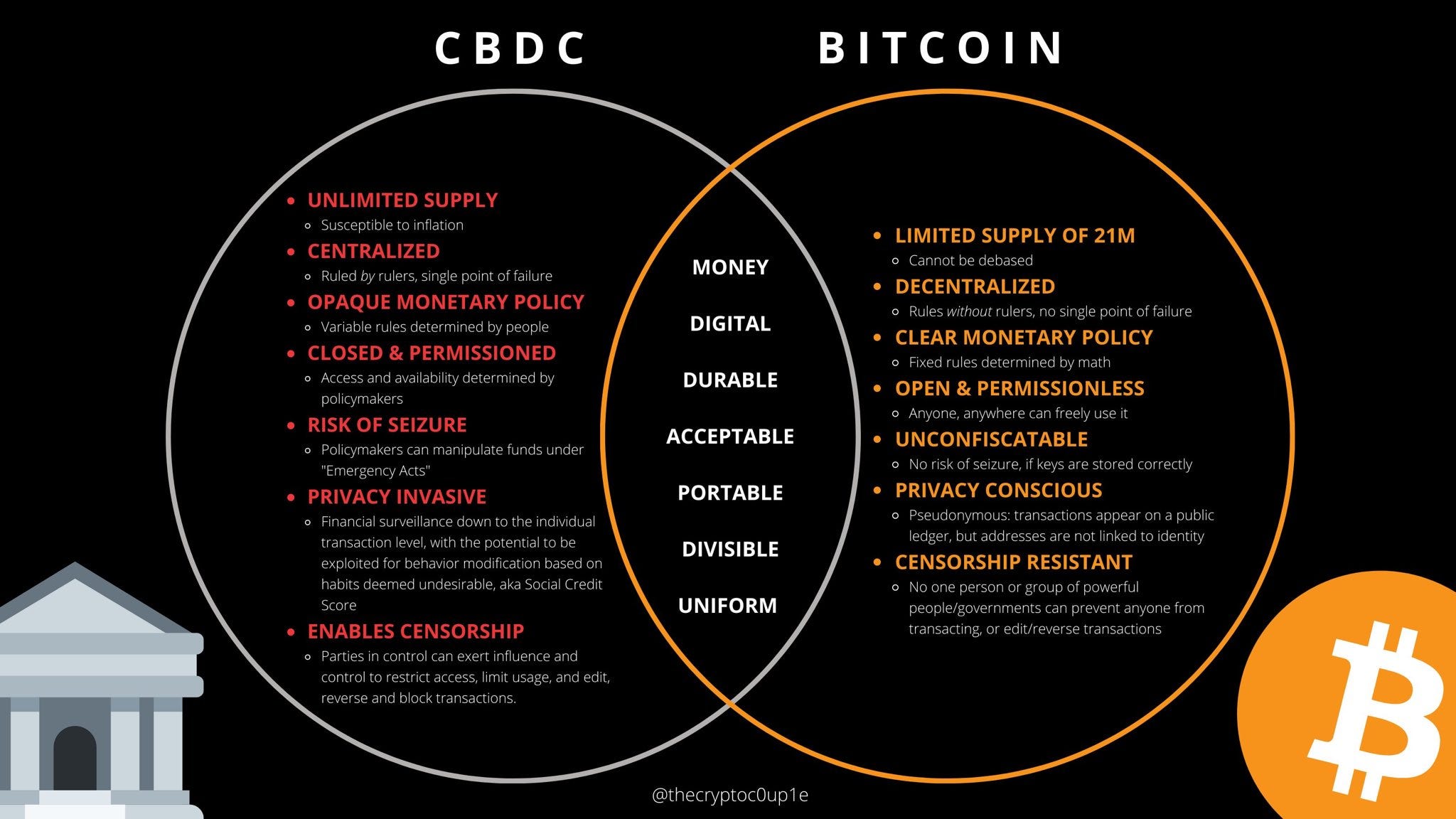

Here is an excellent graphic comparing what the global central banks are trying to implement compared to how Bitcoin a decentralized network actually works. You tell me which one should be the future, debt and inflation or P2P decentralized? You know where we stand!

With all this balance sheet talk and with all the rhetoric that the banking sector is fine and that ALL DEPOSITS are SAFE is an attempt to hide the reality of fractional reserve banking. The FOMC does not have the authority to insure all deposits, nor is there enough money in the system to do this. As we have stated time and time again, the majority of wealth is an illusion, it only becomes real or tangible when you exit a position, sell, liquidate and convert an asset into something tangible. This is why all deposits cannot be insured because the money doesn’t exist. The majority of money is digital credits, which can be written down, destroyed and zeroed out. This in fact is what reducing the FOMCs balance sheet does, it destroys credit, which is necessary especially given the fact that we have $3T in excess reserves doing nothing for the real economy.

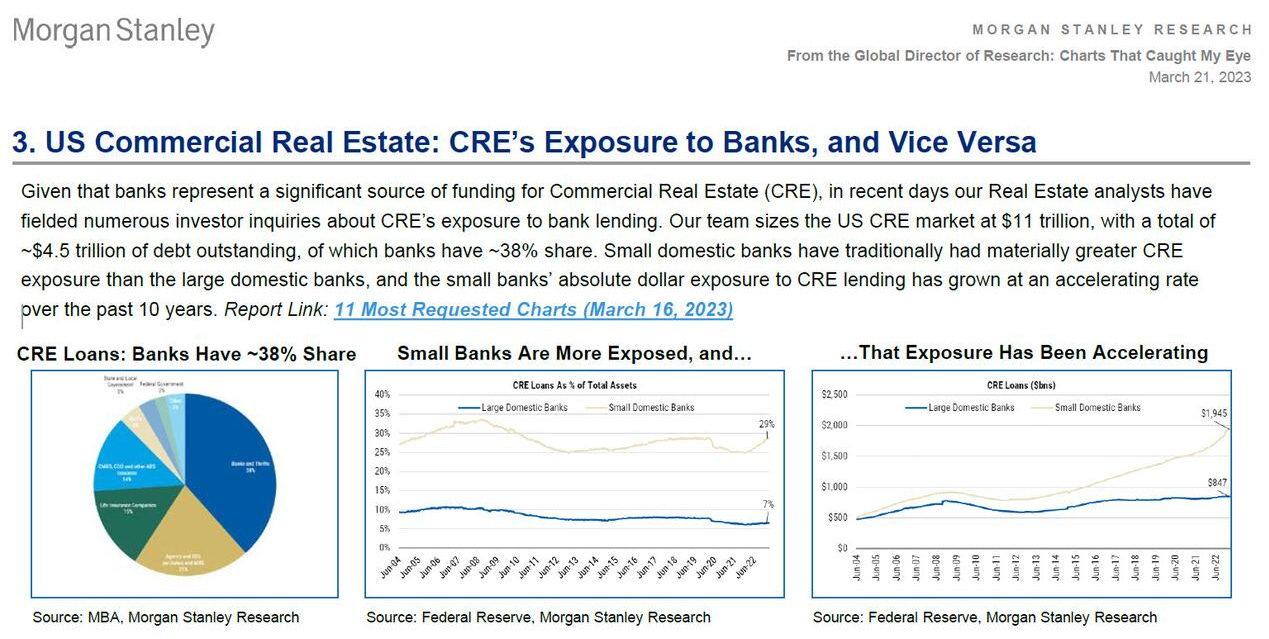

The banking sector worries have just begun, the next problem that is on everyone’s radar now is commercial real estate. The following Morgan Stanley chart given the weakness of smaller banks, should be an eye opener for our readers here:

Look, the bottom line is no matter how much the FRB wants to fight inflation, higher rates are not sustainable, nor is shrinking the balance sheet. It should be obvious that the global asset classes that have benefitted the most, continue to be the recipients of bailout, after bailout, decade after decade. We just aren’t sure that the overall banking sector can survive this, nor do we believe the FRB wants them too. It seems as if its all a set up to concentrate deposits in order to implement tighter controls. So keep an eye on out for word on CRE exposure, we suspect this shoe has already dropped!

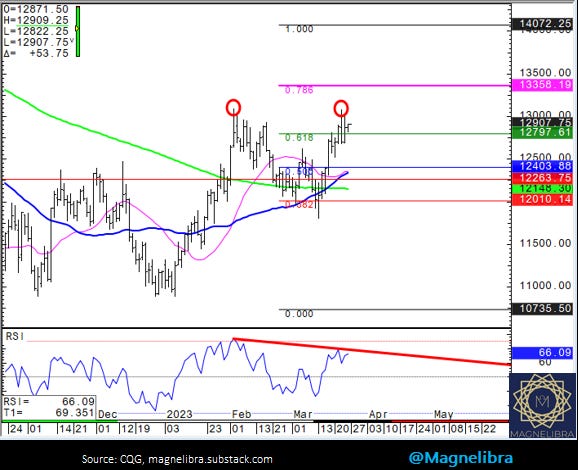

Ok let’s look at the markets, right now we are seeing the June Nasdaq with 2 solid rejections of 13k and weakening RSIs putting in a decent double top. We saw follow through selling in size late in the day today and for us 12797 is the key to confirming this top, bulls are still in control as long as we do not close below that level tomorrow!

As far as the June SP, the 4000 strike is key as it is the top of our channel here and a heavy vol. strike price. 3990 is key today and above we can test a breakout of this channel but below we risk a break down to 3948 area then 3913:

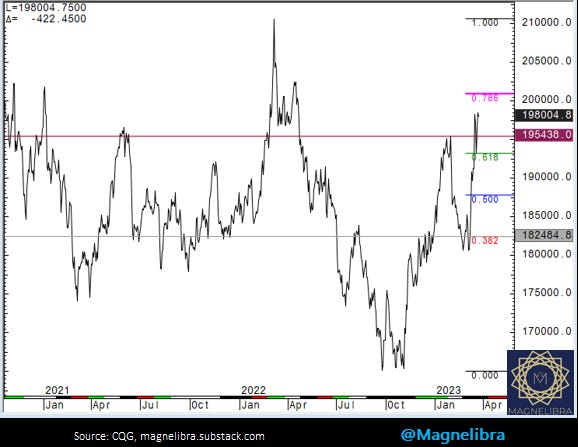

We are keeping a close eye on the June Bond Futures as they trade above the 200p Vwap and are the weak link on the US treasury curve, but we feel a break of 133-08 will bring some fast money looking to breakout out of the multiple highs up there over the last 5 months!

Our last chart is the Gold/Silver futures contract spread. Golds recent outperformance since Mid January has pushed us up to resistance. However we would be patient with this and look for gold to have one more push to new highs, possibly near 2035 and sell gold vs silver near the fib 0.786 target/reversal area:

We will get some PMI numbers tomorrow to give us a peek at ongoing inflation compression and as usual weekly options expiration so good luck and keep things manageable!

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023