Share Buybacks Concentrate Wealth

Reduce shares increase EPS

What we are currently witnessing in the equity markets, in particular the recent tech giant earnings are the fact that these companies are announcing huge buyback programs. We believe this is for two very distinct reasons,

The companies need to offer this incentive to keep investor appetite strong especially given the current markets valuation amidst 5% Fed Funds and competing fixed income interest rates.

Concentrating wealth for the largest shareholders something QE does but this mechanism is truly the stealth form as investors generally cheer and bid up equities that announce buybacks, when in reality it is purely reducing float and increasing the power of the few that hold large chungks.

Let’s first look at how a company would buyback its shares:

The company decides to repurchase its own stock, either on the open market or through a tender offer.

The company uses cash, debt, or a combination of both to buy back the shares.

The shares are retired or canceled, which reduces the total number of outstanding shares of the company's stock.

As a result of the reduction in shares outstanding, the earnings per share (EPS) of the remaining shares will generally increase. This is because the company's earnings are divided among fewer shares.

If the company bought back the shares at a price lower than the original issuance price, it may recognize a gain on the transaction. If the company bought back the shares at a price higher than the original issuance price, it may recognize a loss on the transaction.

Furthermore there are tax consequences and this may also benefit the company especially if the share buybacks are occurring at record high equity prices, which may result in a tax loss. The tax treatment of a stock buyback depends on whether the shares were originally issued as a capital contribution or as compensation.

If the shares were originally issued as a capital contribution, then the tax treatment of the buyback will depend on whether the shares were repurchased for more or less than their adjusted basis. If the shares were repurchased for less than their adjusted basis, then the company can generally recognize a loss for tax purposes, which can offset other taxable income. The adjusted basis of the shares is typically the original purchase price, adjusted for any stock splits, dividends, or other adjustments.

If the shares were originally issued as compensation, then the tax treatment of the buyback will depend on whether the shares were repurchased at a discount or at fair market value. If the shares were repurchased at fair market value, then the company generally will not be able to recognize a loss for tax purposes. If the shares were repurchased at a discount, then the company may recognize a tax deduction for the amount of the discount, subject to certain limitations and rules.

Now let’s look at the concentration of wealth mechanism, then we will provide a real life example:

One of the biggest impacts of buying back shares is that it reduces the number of outstanding shares, which can have several effects.

First, reducing the number of outstanding shares increases the ownership percentage of existing shareholders, which can concentrate power among them. For example, if a company repurchases 10% of its outstanding shares, the remaining shareholders will own a larger percentage of the company than they did before the buyback.

Second, reducing the number of outstanding shares can increase earnings per share (EPS), which is a key financial metric used by investors and analysts to evaluate a company's performance. When a company repurchases shares, the same amount of earnings are divided among fewer shares, which can result in a higher EPS.

Third, reducing the number of outstanding shares can also improve return on equity (ROE), which is a measure of how efficiently a company is using its shareholders' equity to generate profits. When a company repurchases shares, it reduces the amount of shareholders' equity, which can increase ROE.

Overall, the impact of a share buyback can vary depending on the specific circumstances of the company and the market in which it operates. While a share buyback can have positive effects such as increasing EPS and ROE, it can also have negative effects such as reducing liquidity and potentially limiting growth opportunities.

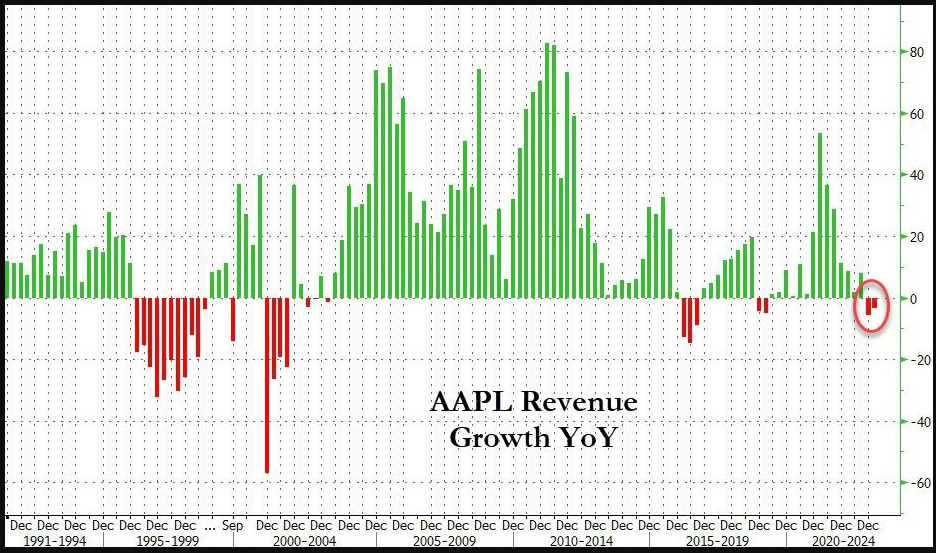

Now let’s look at the Apple recent announcement, which by the way, Apple has recorded consecutive back to back quarterly YoY revenue declines:

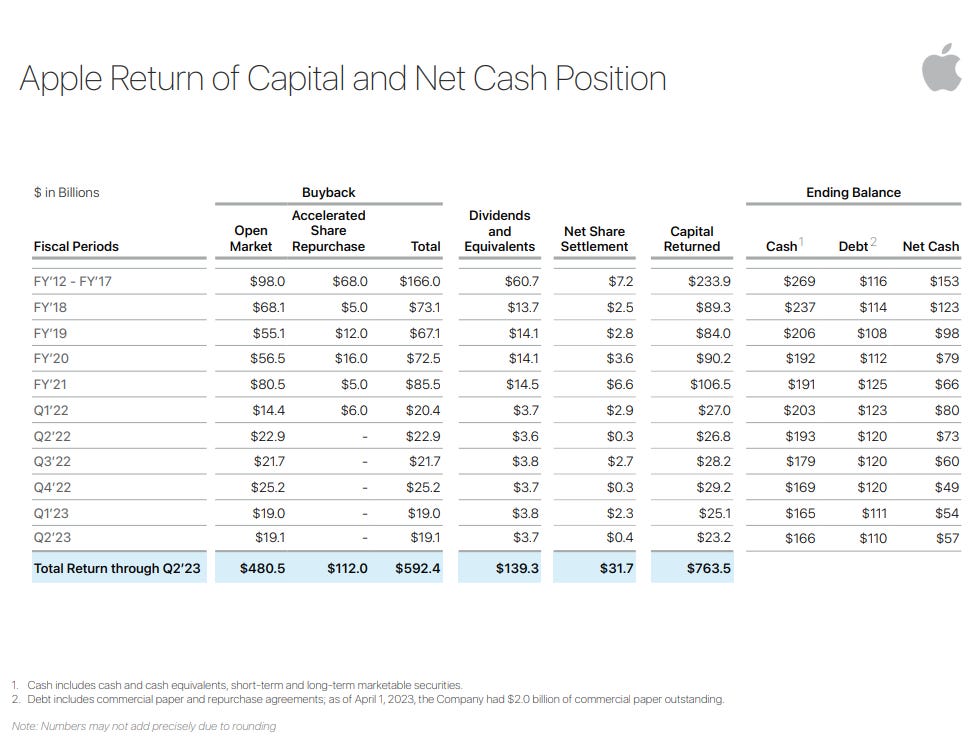

In 2012-2017 Apples net cash positioned averaged $153Bn, fast forward to today, Q2 2023 net cash $57Bn a reduction of nearly $100Bn!

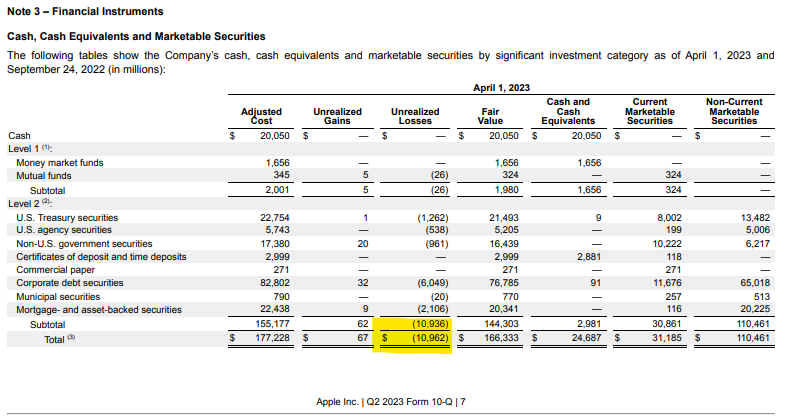

Furthermore Apple Inc. is reporting nearly $11Bn in unrealized losses on its securities holdings with the bulk of the M2M loss in corporate debt securities:

So despite Apples declining revenues and cash hoard, the company still went ahead and announced buybacks, how long can this last?

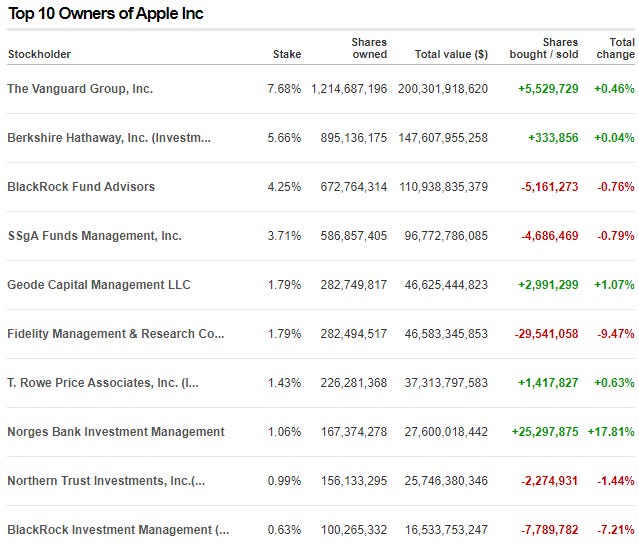

Furthermore, When looking at Apple Inc. and its total shares outstanding has been reduced down from 26.52B in 2012 to 15.96B currently. This is a reduction of 40% or an annualized decrease in the supply of stock of 5.4%! Eventually this will have to level off, especially once the cash hoard starts to go negative. Perhaps that is the tell we will require in order to revalue the buying frenzy that has since this equity rise 14x in 10years. One thing is certain, these top 10 holders continue to concentrate their wealth via mechanisms like stock buybacks and Quantitative Easing.

These are the stealth mechanisms that many do not see on a day to day basis, but clearly is evident in the actions by central banks and the mega cap Tech stocks. Issuing Securities, Issuing debt, these are the credit creators, these are the monetization mechanisms that have taken over for traditional bank lending mechanism which is nascent.

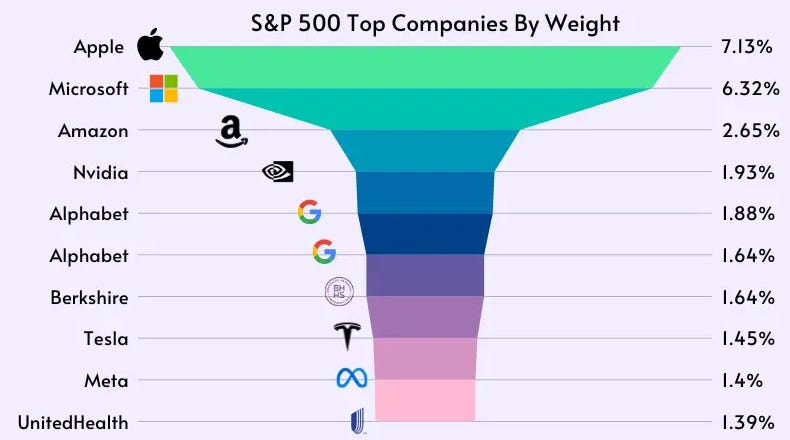

Nobody really talks about these as wealth concentration creators, but it is quite obvious to us and it should be to you. We always here that equities are overvalued and they have to come down. Well there is some truth to that but the reality isn’t for every stock. That may be the reality for the majority of equities, but the market we have today is dominated by about 10 large names and nobody else seems to matter.

Alphabet Inc. announced a $70B buyback and their total shares already in just 4 years has dropped 8%. So you can see the trend, this is how you keep valuations high, however with interest rates greater than 5% these companies better hope we do not see a severe downturn. If we get the higher for longer coupled with the onset of a global recession, then assets no matter how concentrated will be sold. We just wonder what it will take for investors to realize they can get 5.25% risk free from the US treasury on a 91 day TBill vs equity and corporate bond risk. We believe some investors have begun this exodus and as time goes on it will be interesting to see how much leverage gets purged from the system.

Today we see the Nasdaq +300 points or 2.3% with a hefty post FRB, earnings move and this type of buying in front of a absolutely insane 3M/10Y inversion seems very curious to us. We can only say that there is a lot of hope that the global central banks will resume the money printing, yet we do not see it that way just yet. Investors are continuing to take on risk when the global bond market is stating otherwise…the battle continues!

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023