Stocks Saved By Reduced Volcker

GFBP Still Holding Hedged Short

What was mainly a non event day after the the stocks ended up being boosted late in the day by the large POMO operation announcement for tomorrow (QE, i.e. Monetization) and even more so by the FDIC announcing a loosening of Volcker Rule restrictions.

The announcement removes some of the restrictions that were put in place after the GFC and now will allow banks to take on large investments in venture capital and even more importantly companies will be able to now avoid setting aside cash for derivatives trades between different affiliates of the same firm. (Co-mingling and Leverage Much)

Anyway it’s good to see that at least one FDIC member has a moral hazard head on their shoulders, Martin J. Gruenberg put out this statement late today,

“Today’s Final Rule goes far beyond streamlining or clarifying the covered fund provisions of the Volcker Rule as asserted in the preamble.19 It would severely weaken the restrictions on relationships between banks and covered funds. It would reintroduce the types of high-risk investments and activities that contributed to the 2008 financial crisis, and risk repeating those mistakes in the current uncertain environment created by COVID-19. For this reason, I will vote against the Final Rule.”

A link to his full statement, which we feel is a #mustread for all investors can be clicked here, Gruenberg FDIC Statement

We aren’t shocked at the audacity of the FDIC to pull this, we can’t help but think there is zero tolerance for prudent investing behavior. It’s save the sinking ship at all costs, and we mean all costs even if it means taking on obscene amounts of levered risk! All that prudent regulatory oversight, well toss that out, its back to bailing out everyone and now everyone is a GSIB! Paging Deutsche Bank, Wells Fargo? Probably everyone else as well!

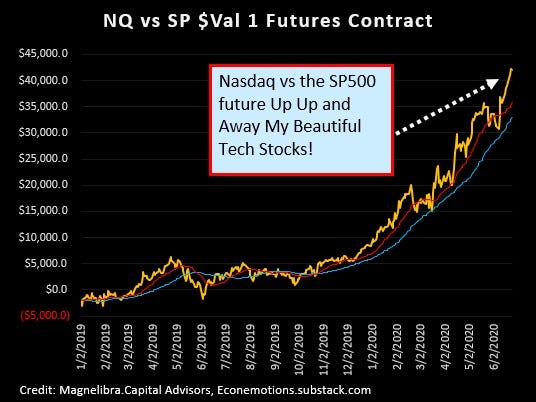

Anyway at least we can see the parabolic move in the Nasdaq vs the SP500 continues:

Not that the DAX means much to the Tech Heavy Nasdaq, but this chart seems to be weighing on our minds currently as it struggles with the prior trend channel:

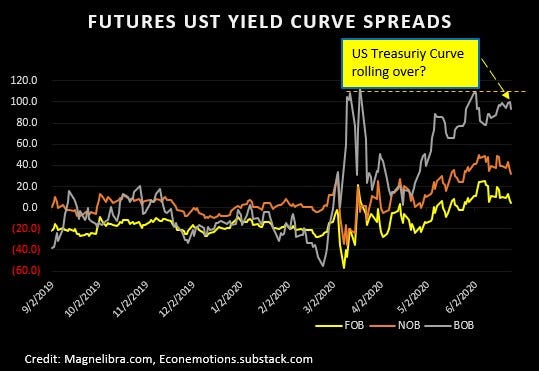

We have also seen a retreat in the US Treasury Curve as it seems to have turned to a more flattening path, this chart is the intercommodity futures spreads in the US Treasury futures markets, the FOB, NOB and BOB:

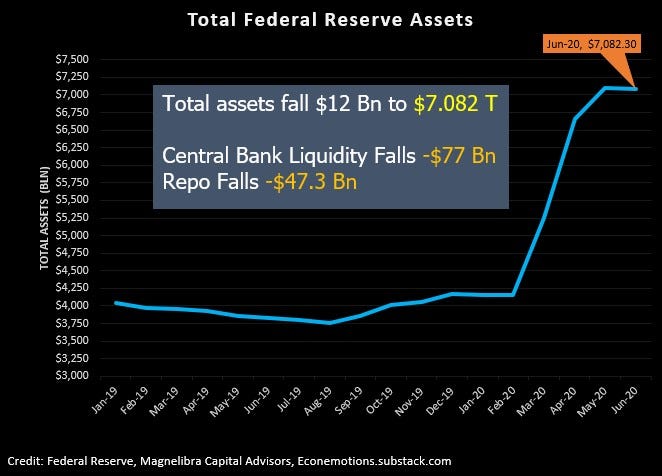

We also saw the FED H4 report out late today showing another decrease in total assets as Central Bank Liquidity Swaps dropped a massive $77 billion:

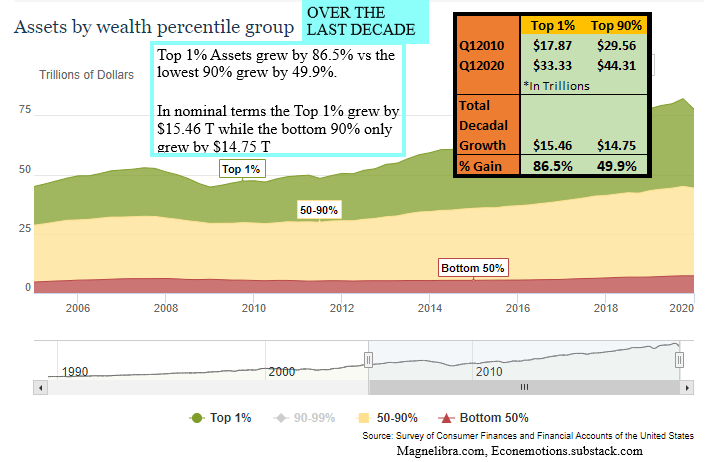

We are glad to see the FED also put out an income disparity chart, well they don’t call it that, but we will highlight our point. As you will see over the last decade the Top 1% grew their assets by a whopping 86.5% while the bottom 90% only grew by 49.9%:

So when people say QE doesn’t cause disparity, well toss them this little chart, logically it makes perfect sense, because who owns the assets? Who pays rent? Who lives paycheck to paycheck? A two tiered economy is what we have and its charts like this that prove it. Even an Austrian Economist that we are must admit the rationality for UBI makes sense well not really its more of a symptom of a disease, not a cure, but you get our point.

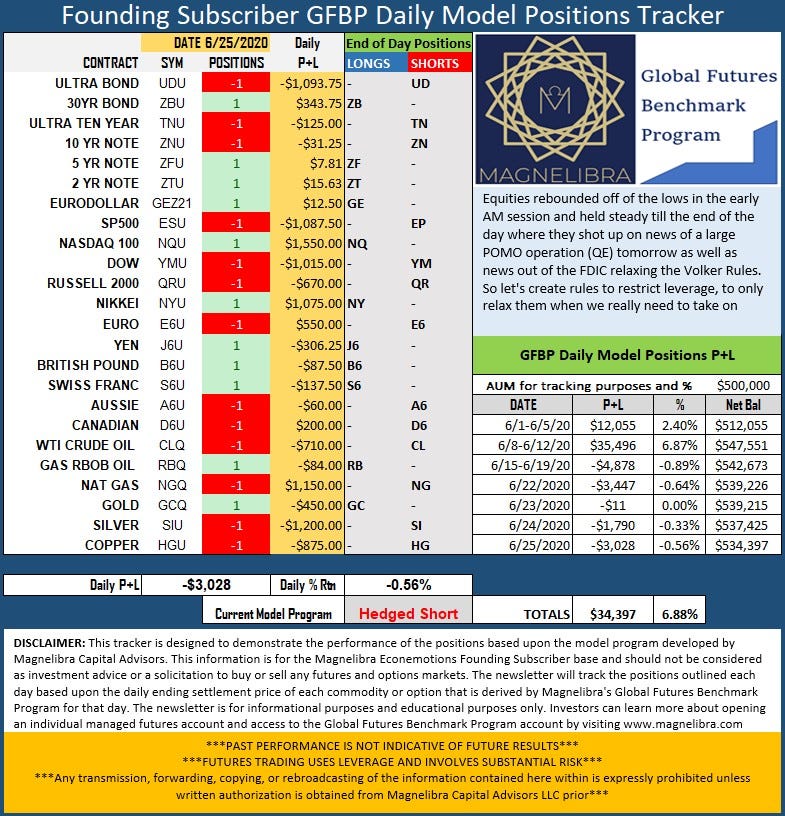

Ok finally to the GFBP Positions Tracker which has struggled a bit, which is expected as we battle out here at the highs in equities, it still sits in a Hedged Short mode. The only changes to the tracker is the roll from July to Sep in the Silver and Copper markets. We aren’t impressed at the bears abilities here in equity land, they keep getting thwarted by the removal of prudence out of our regulators. Will this all work this QE, this removal of prudence, is still up in the air:

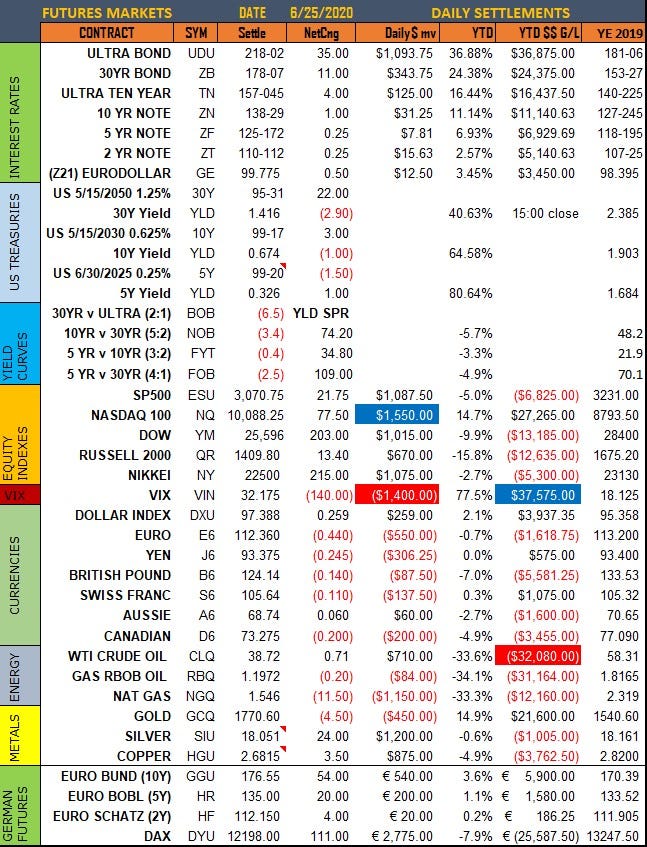

As far as the settlements for 6/25/20:

We tend to think the equities continue to be priced for perfection, actions like what the FDIC did today, shouldn’t be taken positively. Rather it should be taken as a warning as to how bad the underlying fundamentals truly are.

When you toss out a decade full of reform and equities rise because of it, you have to kind of ask yourself, what the hell are we really cheer-leading for?

We either want legitimate markets or we don’t

We either want a free market economy or we don’t

We either want equality in opportunity or we don’t

If we can simply take a decades worth of reform, toss it out the window and rewind the tape to make the same mistakes over and over again, this should tell you something about the very system that we have all become so reliant upon and who really pulls the strings.

OK, we hope you continue to spread the word on our work here with your friends and colleagues, remember, knowledge is key and it is the absolute goal of Magnelibra’s Econemotion to put you always ahead of the pack. When your family, friends and neighbors ask, how you know all this stuff, we hope you point them in our direction. We hope you consider contributing to our work and joining as a monthly subscriber and for the professional traders and investors, join our Founding Subscription because the position tracker is a uniquely proprietary driven model designed as a global macro market analytic that we believe can help to advance your trading and investing game.

-Magnelibra’s Econemotion

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.