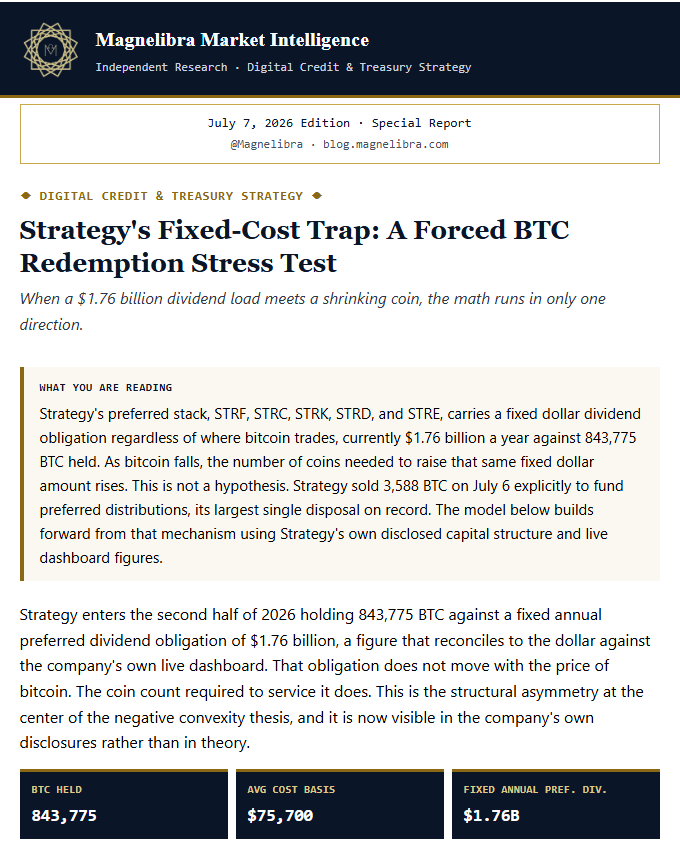

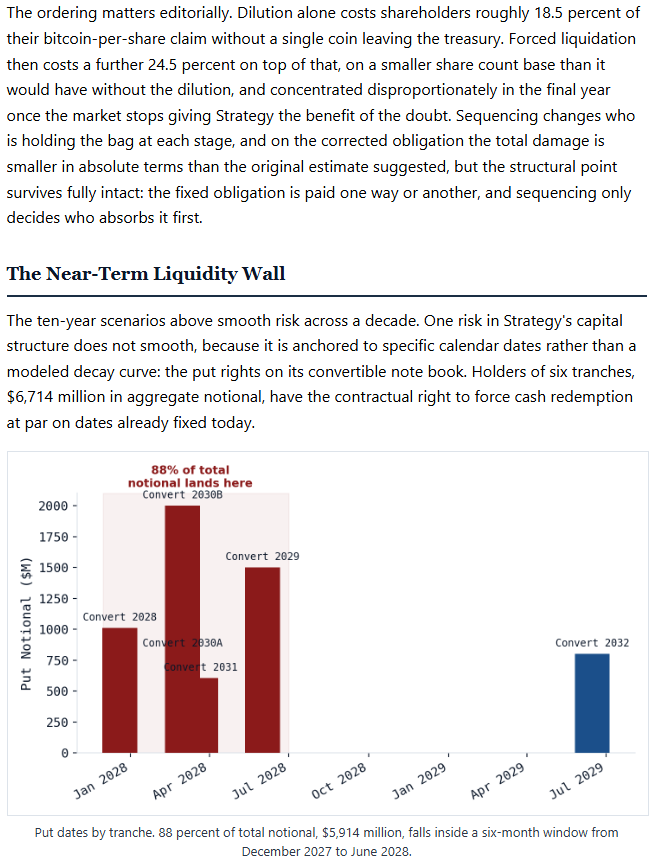

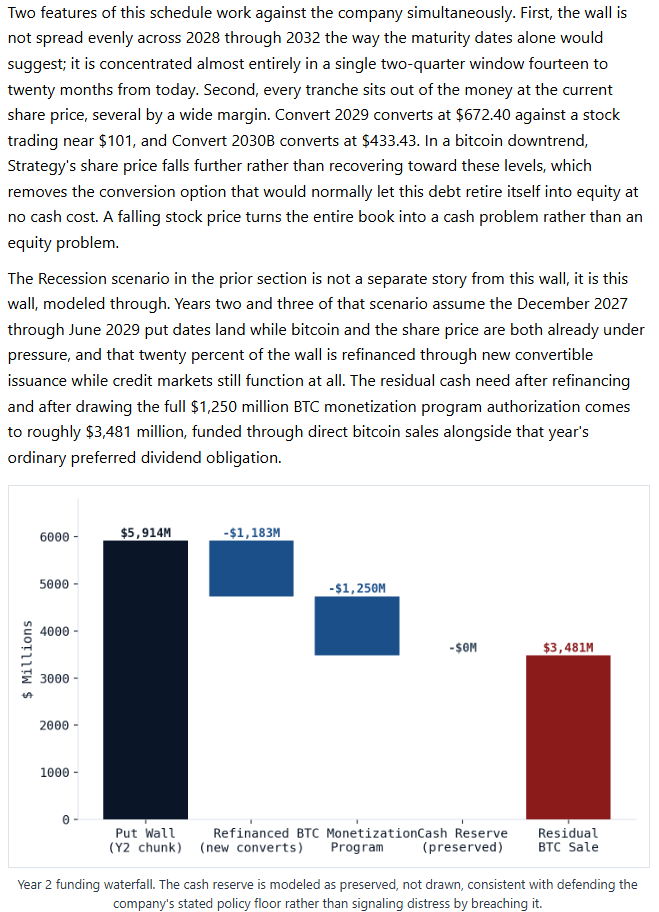

Strategy's Fixed-Cost Trap: A Forced BTC Redemption Stress Test

When a $1.76 billion dividend load meets a shrinking coin, the math runs in only one direction.

Strip away the ticker, the conference circuit, and the software business Strategy still nominally operates, and the mechanics walked through in this report describe something fairly simple. The company borrows and issues securities against cash flows it does not have, in order to buy an asset whose price it cannot control, and it repeats that cycle for as long as capital markets allow it to. That is not a treasury policy. It is a levered, single-asset hedge fund wearing a corporate structure, financed by a stack of preferred securities and convertible debt rather than prime-broker margin, but running on the same principle any leveraged fund runs on: borrow cheap, buy volatile, and hope the spread compounds before the bill comes due. Every model in this report is the same mechanism described from a different angle, because there is really only one mechanism here to describe.

The entire structure is a wager that bitcoin’s price appreciates faster than the cost of the capital used to buy it.

When that holds, the arrangement is spectacular, and it is the trade that built Strategy’s premium in the first place. When it does not hold, and every year bitcoin trades below the return the preferred stack demands is a year that condition fails, the same structure runs in reverse with more force than it ran forward, for the reasons the negative convexity models above lay out in detail. Strategy is not holding bitcoin so much as renting the right to hold it, from preferred and convertible investors, at a rate that must be paid whether the bet is working or not.

What gets lost in nearly all coverage of this story, our own included until this report, is that bitcoin’s actual utility function does not care about any of it.

The network settles transactions, secures its ledger, and does what it was designed to do identically whether one bitcoin is worth $60,000 or $1,000. (nobody but Magnelibra mentions this!)

The protocol has no opinion on Strategy’s balance sheet, and no opinion on price at all. A fair counterpoint belongs here: proof-of-work security is not perfectly price-independent, since a lower price eventually reduces the dollar value of mining rewards and could, at the margin, thin the hash-rate defending the network. That mechanism is real, but it is secondary to the point being made. The ledger’s basic function and settlement guarantees do not move tick for tick with price the way a leveraged balance sheet does. Strategy has built a wrapper that monetizes a bet on bitcoin’s price. It has not built anything that changes what bitcoin actually does, and the industry has spent the better part of a decade collapsing those two separate questions into one.

First-mover status is a real advantage, and a fragile one. Financial and technology history is full of incumbents that looked unassailable until a narrower, better-engineered challenger took the ground the incumbent had left exposed, and we think that ground exists here. Our own view, for whatever it is worth, is that Monero (XMR) addresses two problems bitcoin’s design has not solved and arguably cannot solve without a fundamentally different architecture: privacy and fungibility. Every bitcoin is traceable on a public ledger back to its origin, which means individual coins can be tainted, blacklisted by exchanges, or flagged by chain-analysis firms over history a current holder had no part in. That is the opposite of sound money. Monero’s ring signatures and stealth addresses make every coin equivalent to every other coin, which is what fungibility actually requires, and bitcoin does not have it. Whether markets ever price that distinction the way we think they should is a separate and open question. Adoption, liquidity, and regulatory treatment still overwhelmingly favor bitcoin today, and we would be doing our readers a disservice if we implied otherwise. But we think it is a mistake to treat the incumbent’s technical position as total or permanent.

We want to close on the audience we think is least prepared for what this report describes: pension funds, endowments, and other fiduciaries carrying direct or indirect bitcoin exposure, whether through spot holdings, ETF wrappers, or equity positions in companies like Strategy.

We would wager, and this is opinion, not something we can verify, that very few of these allocations have been stress-tested against the specific mechanism this report walks through: a leveraged treasury vehicle forced to compound its own selling pressure into a falling market in order to service fixed obligations that do not care what bitcoin is worth. That is a different and more structural risk than “bitcoin’s price could fall,” and we suspect most advisory boards have modeled the latter and never been shown the former. If your fund carries exposure to bitcoin, to Strategy, or to any security in its preferred stack, the model in this report costs nothing to replicate against your own position sizing. We think every fiduciary with that exposure owes their beneficiaries the exercise, rather than taking an advisor’s word that it isn’t necessary.

-Team Magnelibra wants you to be at your best and we only put out content that puts your knowledge well above the rest. Please think about subscribing to support our work and sharing so that others can benefit from our insights. It only takes a minute to share to a few of your colleagues but it goes a long way toward increasing our reach.