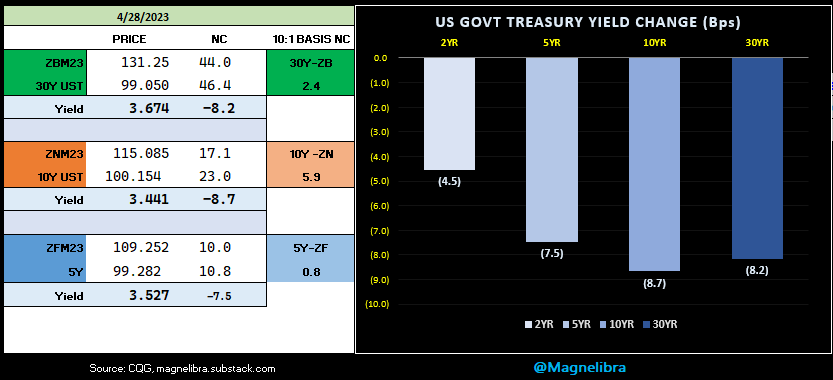

Strong US Treasury Cash Buyers

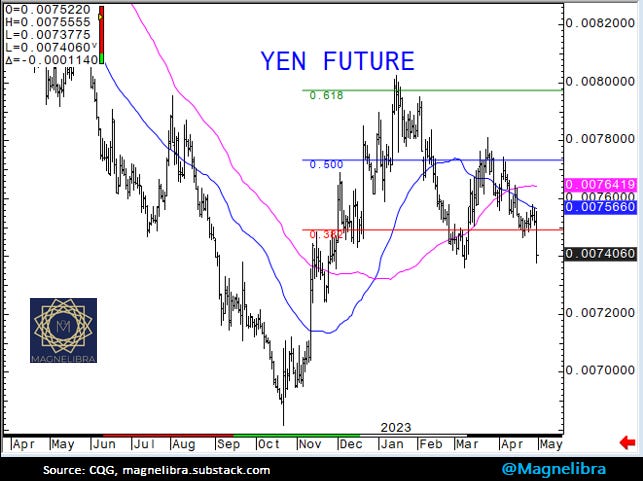

Comments out of the BOJ from Governor Ueda which sent US Treasuries higher overnight. Here are a few highlights from his comments:

"Uncertainty regarding domestic and overseas economic and market developments is extremely high. While trend inflation is gradually heightening, it will take some time to achieve our inflation target. As such, the risk of missing our price target with premature monetary tightening is bigger than the risk of experiencing inflation exceeding 2% due to a delayed tightening. The cost of waiting for trend inflation to heighten is low."

I want to be patient here and maintain easy policy a bit longer."

"We don't have anything in mind in terms of tying this to a near-term policy tweak.

Treasuries continued to climb after this mornings Personal Income and Core PCE came in line. We have month end demand here and given the FRB meeting next week (FOMC) many are expecting that the FRB is getting closer to the end of their hike campaign. As for now Treasuries are strong especially in the cash markets as there have been consistent buyers all night and day strengthening the basis (spread between futures and cash markets):

The US Govt 10Y is the star performer on the day down 8.7bp thus far. Today’s move has already erased 3/4s of yesterday’s sell off.

The Yen futures however did not like the dovish Ueda comments and currently is the weakest FX link on the day, while the dollar is weaker the Yen is down 115 pips:

The equity markets had a big up day yesterday led by the Nasdaq of course, and today we are seeing a minor continuation led by the SP500, which the futures are now poking their head out of the channel, funny how this set’s up pre FRB meeting isn’t it. The bulls have all their chips in right now:

With a 25bp hike coming, this means a >5% Fed Funds market and a level by which the FRB will try to maintain and hope things don’t go south quickly. The resiliency of the tech sector to continue to rise against a 5% Fed Funds and a 150bp plus negative carry is pretty spectacular. If there is one thing that Magnelibra understands now more than ever is that the excuse that we needed zero interest rates for so long should never be tolerated. For it is clear now, that even at current debt levels, 5% Fed Funds doesn’t seem to harm the economy the way that many have suspected.

We aren’t sure how long the global economies can handle this new higher equilibrium level, but we are slowly finding out with each passing day. This will truly affect consumer spending habits and sales should slow but not grind to a halt and that is what the FRB is hoping for. We are usually critical of the FRB and their mistakes, but we do believe higher rates are and have always been appropriate in order to maintain fiscal discipline. Now if we can get an administration to enact some budget constraints that would be something.

Also out today we saw the FRB analysis of the SVB debacle. The continued call for more oversight is a testament to the inability for the FRB regulators to use their current tools effectively. We did like that they admitted the following in their report,

Federal Reserve oversight of SVBFG proved inadequate for the well-documented and significant vulnerabilities and managerial weaknesses at SVBFG - Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank

Here is a link to the full PDF of their analysis. Let’s be honest this was complete arrogance out of the bank management, they knew the risks, they took them and there are no excuses for their actions and there are certainly no excuses for the FRBs failure to supervise them. Negligence all around. Here is the link, Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank

Alright, we will be back again.

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. Magnelibra the CTA and its Global Futures Benchmark Program may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

ALL RIGHTS RESERVED 2023