Taxes Inequality and Slow Grind Higher Weekly Update April 17 2018

Well, it’s that time of the year again, where millions of Americans race to meet the deadline to file their annual tax returns. We have seen a lot of discussions about the tax code, the changes and various opinions as to the benefits and costs of Trump’s new tax plan.

It’s no surprise that #POTUS has been vocal the last few days about the glory of his tax plan and even #VPPence took to twitter today:

Despite all the administrations gloating, we feel it is quite comical that the federal tax code consists of some 74k pages, yes that’s thousands![1] We have an idea, how bout we get rid of income taxes and just issue bonds. This is a republic, right? Perhaps the people should vote on it, hell the US Government just borrowed $275B in Q1 alone. What is indeed both troubling and interesting at the same time is that Q2 borrowing jumps to $512B nearly double the first quarter amount![2]

So, what would be the difference if we merely added to the treasuries borrowing, another $400B a quarter? It’s not like the principal matters, its just the interest payments we need to cover right??? Furthermore, and what is certainly the biggest scam of all is the fact that individuals paid 5.3x more actual tax than the corporations for FY2017.[3]

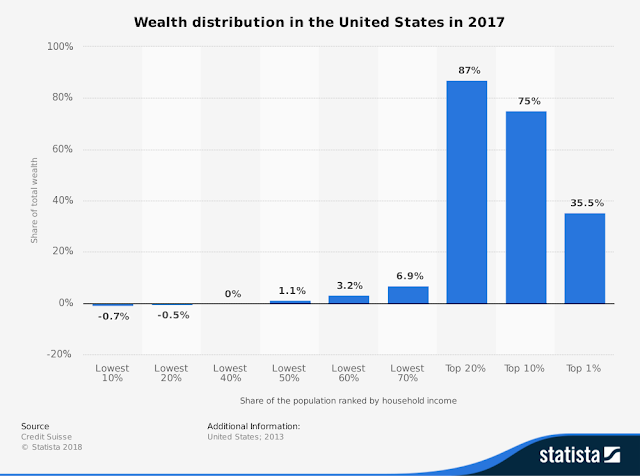

We are truly reaching the heights of Monopoly money, aren’t we? It seems as if the commoners trivial average wage is a mere footnote on the US Treasuries balance sheet. We hear rumors of so called wage inflation and yet, that seems more conjecture and even hypothetical in fact because, we don’t see it. What we do see is the staggering and certainly unsustainable income inequality that the US is exhibiting. We expect this from some third world banana republic but if the elite globalists think this is going to stand than they have not studied their history very well. In fact, we believe that the populist revolt that elected such a prominent celebrity to the highest office in the land is indicative of the overall concerns of the commoner base. Statista has a great chart of this inequality problem and in fact their latest figures point to the sheer magnitude of this divide, where 87% of the wealth in the United States is owned by 20% of the population. Even more staggering is the fact that the top 1% control nearly 36% of all the wealth:

So, we can talk tax remittance and percentages paid and the wealthy can claim they pay 97% of all the taxes but that is why we do not compare nominal amounts. In fact, even comparing percentages when it comes to the top 1% doesn’t make sense because their wealth is so exponentially higher than the average worker that the math doesn’t fit. We are certain of one thing; the data is suggesting that the fiscal and monetary policies do not exhibit general linear models and are in fact directly contributing to this inequality. Yeah, yeah, we will hear arguments till people are blue in the face that its always been Wall Street vs Main Street, but that is not the case. Yes, there have been super wealthy and their opposite extreme poverty, yet this duality has never been this extreme. A democracy and even a republic must recognize that a more equitable distribution will have a greater impact on the social fabric and civil well being of a nation than a hockey stick distribution. Perhaps we are just wishful thinkers, or maybe we just hope logic finds its way into halls of the NY Fed and DC.

The overall equity markets late last week seem to exhibit sell off exhaustion as those seeking protection via going long the VIX hit extremes. When we saw this, we figured where the weak hand was and that’s where it was. So, we thought to ourselves, what would be the easiest course for the equity markets given the extreme weak longs in the VIX? Well to grind higher, slowly but surely. This is exactly what they have been doing. We see some technical resistance at 2711 in the SP futures and we will show a graph later, but we have also seen correlations rise after getting pummeled. We aren’t sold on the fact that the equities are in clear sailing mode once again, rather we know markets never go down in a straight line and bounces, even prolonged ones are natural and necessary. Not even the US bombing strategic positions within Syria could derail the up move, so that was very telling. Oil did run up into Friday as those in the know, must have played the setup game in preparation for hostilities, but, the Trumpster had one thing in mind, send a message and that he did. The strikes were of the limited tactical precision type and they were effective.

We know the fundamental players including ourselves continue to be disgusted with the large QE operations and global debt build. One vocal opponent to all this debt, is Lacy Hunt from Hoisington who continues to pound the pavement regarding this unsustainable debt accumulation. As our readers know, we agree with his position and yes debts contribution to growth is going in the wrong direction. Lacy points this all out in the following,

“In 1952, $3.42 of GDP was generated for every dollar of business debt, compared with only $1.39 in 2017. In the corporate sector, where capital as well as technology is most readily available, GDP generated per dollar of debt fell from $4.50 in 1952 to $2.50 in 2007 to $2.21 last year. The dismal trend in productivity confirms this conclusion. The percent change for productivity in the last five years (2017-2012) was equal to the lowest of all five-year spans since 1952. It was also less than half the average growth over that period.” [4]

One thing is very clear, debt is the new growth and it doesn’t matter, until it does, unfortunately.

Well, its earnings season and Q1 earnings are trickling in and despite the massive rise in 3-month LIBOR from .25% to nearly 2.35% the banks seem to be benefitting. Citigroup reported .08 cents earnings beat on $4.6B in revenue up 13% from last year. They also reported a $3.1B dividend and stock repurchase during the quarter. [5]That is surprising to us, as we figure given the lofty share price, the last thing they should be doing with extra funds is buying back stock! Bank of America also beat expectations as profits rose 30%.[6] We are quite sure the lower tax rate helped as well as the higher interest rates because we all know the rate they receive on their credit and loan repayments and the rate they pay to their customers is at decade wide spreads. Dare we mention their take of the $47B per year in free money from the Federal Reserve for the IOER mechanism??? Good news none the less for investors we suppose.

Also reporting was Netflix as their shares climbed 5% to $323 which puts their overall equity 2018 return near 60%! Their content spending continues to climb, hitting $10B this year, but they continue to add subscribers, 7.4 million in Q1 alone. Free cash flow is projected to stay negative for a few more years. The problem we see with that is twofold for Netflix. One they must continually pay up for content to stay at the cutting edge and second their $24.4B in debt is problematic, higher rates notwithstanding, effectively you eventually must make consistent profits to remain viable and to afford this said debt.

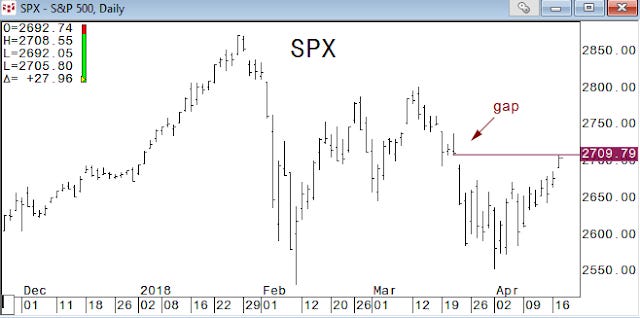

We commented last week in a few blog posts about the buildup of VIX protection and the most likely scenario that this would lead to and that was, a slow grind up in equities. The name of the game today seems to be, sniff out the largest weakest position and force them to the exits, well here is the SP chart (All charts courtesy of Keystone Charts Inc):

2711 is the Fib 61.8% so we would expect that to stall and offer some short-term players some decent levels to sell into. However, given the technical backdrop, the fundamental earnings picture may provide a continued slow grind higher.

Another thing we pointed out last week was the grind up in the DAX, which may be leading the US equity markets higher, but expect the green MA to have a say so:

As quickly as correlations broke down, we can see now that the US bond futures market is now following the equity markets higher:

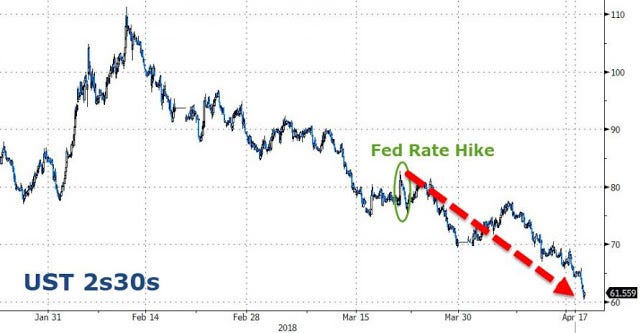

This bond move has the smell of US yield curve flatteners, meaning investors and traders continue to sell the front end of the curve (ED-5yr) and buy longer dated bonds. This flattening of the US Yield curve is widely expected and consistent with the hawkish tone of the Federal Reserve. Zerohedge posted this US 2s30 chart today, you can see the technical damage done to the curve via FED rate hikes as 2s30 hits 61.5 basis points:

Lastly, we are going to post a Bitcoin chart that we put in last weeks Crypto edition, but we figured it was worth a look here. There was plenty of news coming down the pipes about Soros and Rockefeller getting into the Crypto space. Well as you know, these types of players don’t say anything unless they want you to know and only after they have accumulated a position. Although Bitcoin was running into longer term supports in the low $6500 area, the bounce was in no doubt enhanced by the reports of these wealthy titans getting into the fray. There is also some talk of tax selling finally over and we tend to agree with that notion. As our long-time readers know we are bulls on Blockchain and Bitcoin and we continue to monitor the massive advances in the space, anyway here is the chart:

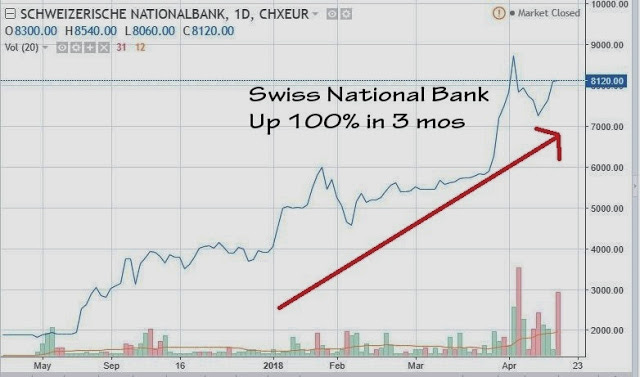

In conclusion we thank you for reading our letter and we hope you were engaged and enlightened. We will continue to monitor the geopolitical events as well as the fiscal and monetary decisions around the globe, speaking of monetary decisions and central banks, is the Swiss National Bank, a hedge fund, a central bank or just a legal counterfeiter? Who knows but their stock has been on fire this year, yes they are a stock as well:

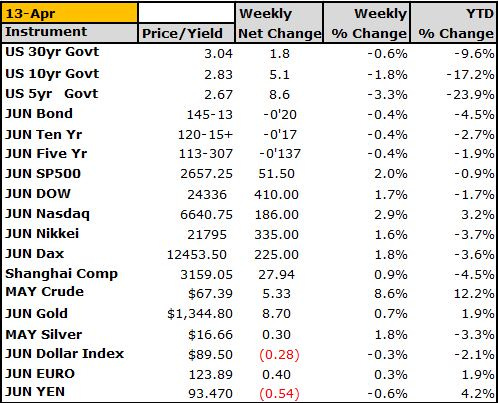

Not a bad gig, printing money and buying private assets, now you can see why the markets can’t fall, the central banks won’t let it! Ok that is it we leave you with weekly settles below, where you can see Crude oil had a great week up over 8% and as usual this year, the US 5yr is the whipping boy, have a great week Cheers!

DISCLAIMER: For Educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures nor an endorsement for the purchase and sale of ICOs or Cryptocurrency and should not be construed as such. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Mike Agne of Agne Asset Management LLC (AAM) and owner of www.econemotions.com and The CryptoCorner Newsletter, that you will profit or that losses can or will be limited in any manner whatsoever. The CryptoCorner logo and name is the sole right and property of (AAM). Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, (AAM) makes no warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed. DO NOT COPY OR FORWARD INTELLECTUAL PROPERTY WITHOUT PRIOR WRITTEN CONSENT AND OR APPROVAL

[1]https://www.washingtonexaminer.com/look-at-how-many-pages-are-in-the-federal-tax-code

[2]https://www.treasury.gov/resource-center/data-chart-center/quarterly

refunding/Documents/Q42017CombinedChargesforArchives.pdf

[3] https://www.usgovernmentrevenue.com/

[4] www.hoisingtonmgt.com/pdf/HIM2018Q1NP.pdf

[5] https://www.zacks.com/stock/news/299117/citigroup-c-beats-on-q1-earnings-as-revenues-improve

[6]https://www.zacks.com/stock/news/299242/bofa-bac-beats-on-q1-earnings-and-revenue-estimates