Tesla Top 8 Again

Debt - Inflation - Bonds - Equities - Tesla - Chicago Bears Loss

As we noted in our last letter, the equity bulls are still in control. If there is one thing we have learned all these years is that trying to predict a top is, well, FUTILE. The markets are affected by so many various forces and subject to so many exogenous inputs, that the best and only thing good analysts can do, is watch the trend and recognize signs that it is about to change.

We have talked for a long time that one of these major forces of change is the Federal Reserve itself. We know the regime has changed and that they have begun changing the trajectory of their short term interest rate cycle from a hiking one to a cutting one. This is one of those primary forces that tend to have far reaching after shocks for global markets, good or bad, its never easy to tell actually, how markets will react.

The historical pattern has been for equities to fall post the rate cut commencement and that may be the ultimate path, however like our last few posts have stated, that doesn’t mean risk markets can’t continue to rise and that is exactly what they have done.

The current modern day equity markets do not function as they once have, they do not send proper pricing signals in regards to value or the status of our global economies. One of the main reasons they do not reflect the general status of reality is because the equity markets in particular their capitalization is a pure function of the total global liquidity that is continually pumped and primed.

I would not recommend any trader or investor try to pick a top on our equity markets because frankly there is far too much capital involved now that is not only concentrated among a very few, but rather a market that can consistently be bailed out by global monetary printing central banks.

You know many people think its crazy to call higher interest rates inflationary and I don’t want to get off topic, but higher interest rates today, from they way I view them are a direct subsidy now to the private sector.

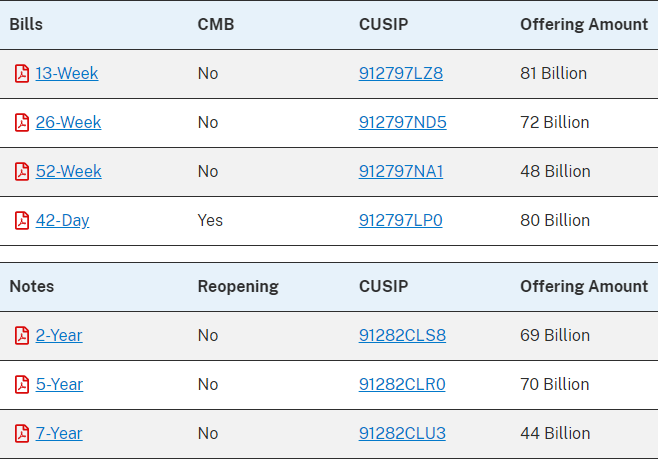

The higher rates allow for governments to pay an exorbitant amount of risk free interest to the private sector via T-bill and bond holder transfers. This year it amounts to $1.3T dollars in regards to the interest cost the US Treasury pays out. In fact this week we will see the US Treasury auction $464 billion dollars and the current US debt is $35.8T up a staggering $7 Trillion dollars in just 4 years!

Just this data alone should tell you the sums that are required to keep the risk train going and for those that think this needs to end some time soon, please don’t be foolish. Yes we hear talk of the US Dollar weakening, that Gold and Bitcoin for that matter will supplant and revalue the US Dollar. We agree that some of that has merit but honestly there are so many more US Dollar shorts out there that will run into a wall of empty coffers when they try to acquire US Dollars to pay off that said debt.

In simpler terms, the word Scarcity is all that comes to mind when it comes to actual US Dollars available to satisfy US debt outstanding. Not to mention the fact that the US Dollar is still widely accepted for goods and services globally and until that changes, well, I don’t think its a logical worry at this point, yea we know the BRICs are trying, but it will take decades to take ahold and there is still no guaranty it will work.

Yes US debt is out of control, but its a product of an overspending, unchecked US congress that will have to eventually be reigned in and that will be a topic for the next few years. We believe if the US congress and government spending can be restrained and interest rates fall, then the US fiscal position will greatly improve and this will benefit the US economy and fiscal position.

We have heard Stan Druckenmiller and Paul Tudor Jones talk about being short the US long end and that owning US treasuries was not desirable. Well that may be an investment choice for them, however when we look at ZIRP and when we look at a 4% plus US Ten Year coupon today, well 4% fixed seems pretty good comparatively. There are those that think inflation will pick up and the US will move into stagflation, well maybe we have already moved through that and maybe the FOMC sees that the economies are taking a turn for the worse and demand is about to fall off the cliff and drive economies into a recession. This for me is the most probable outcome and why the FOMC will continue their rate cuts. I agree with the cuts, but I would also like to see the FOMC balance sheet reduced below $6T. I believe cutting the balance sheet would stem inflation or the mechanism by which inflation runs in today’s economy far greater than cutting rates would.

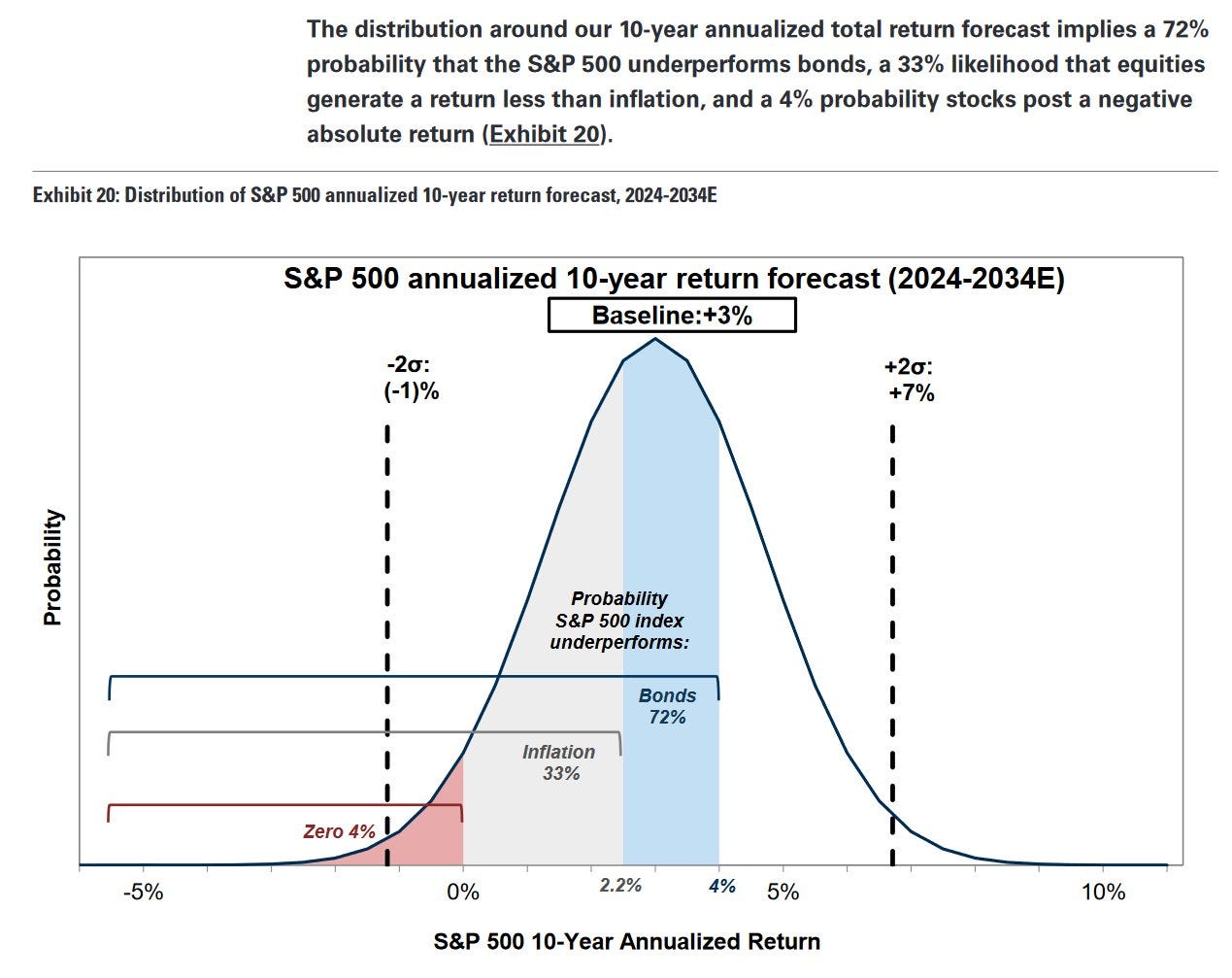

Back to Jones and Druckenmiller and their short US Treasury long end call, well Goldman Sachs doesn’t agree, so its not just me! GS put this annualized 10y return forecast out in regards to the S&P500:

So I guess there is a little cannon fodder for everybody, on one hand you have all this money supporting risk assets, on the other hand you have fundamental valuations so far stretched that the standard deviations on the annualized return comparisons for the S&P500 put it out of favor vs bonds, not to mention an election, FOMC meetings, I guess all opinions will be welcomed and entertained!

Ok also this week we saw Tesla put itself back in the top 8 of all market cap stocks with a massive gross margin beat coming in at 19.8% vs expected 16.8%, operating income was $2.72B beating the $1.96B estimate as well and Free cash flow was massive $2.74B expecting $1.61B! All in all Tesla posted an awesome week +22%:

Tesla added over $155B to its market cap closing near its all important $271 weekly marker. Let’s see if this stock sees early selling this week taking advantage of this recent run or if we get a close this week above $271 indicating continued strength.

Ok let’s move to the equity futures, the Nasdaq has held up over the last few weeks, but honestly it has gone nowhere since that weekly run up in July, so this holding pattern is still here after 3 months. The election move will be very telling but there is no reason to think we get a big move until then, my take is put structures will be favored in the post election playbook:

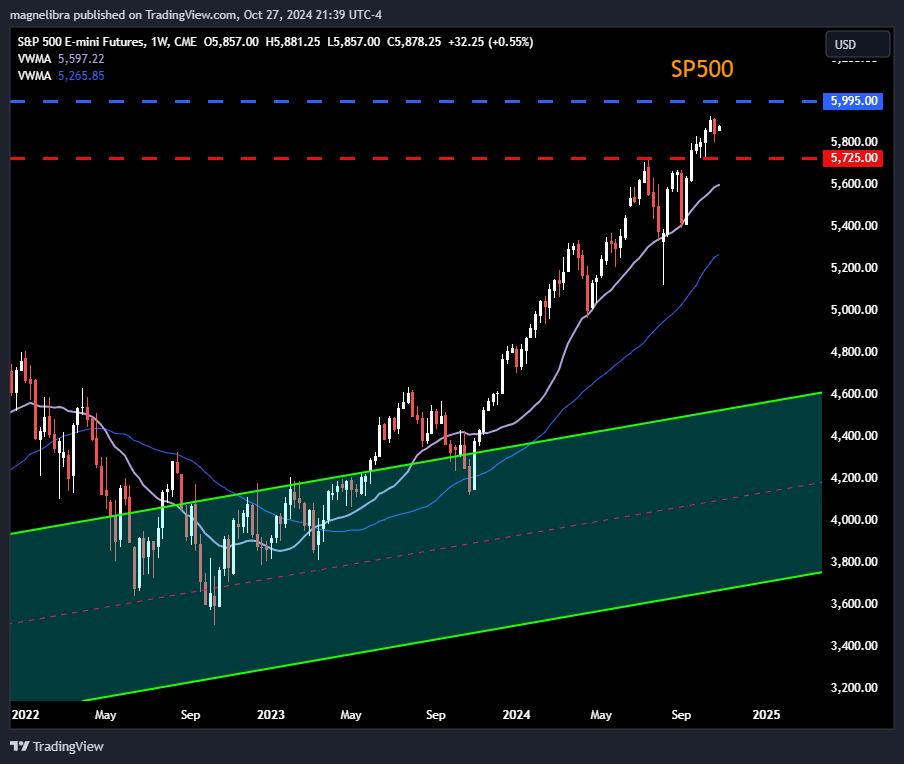

The SP500 futures are painting the same picture although the contract has outperformed the Nasdaq since July and this last run up has been met with a negative weekly bar last week, so bulls are still in control but a chunk of armor has been pierced here:

Another chart that took a weekly hit here is Silver, its had a great run off $27 but we are seeing selling at these levels:

Sellers are showing up in Crude Oil as well and we would suspect a Trump victory would see oil pressured even lower, the chart structure is negative now:

Well its Halloween week and honestly until the election we expect flows to be mainly two ways with bouts of profit taking in some of these risk assets that have flown so high in anticipation of election volatility. So keep the powder dry and we will continue to tell you what we are seeing in the charts here and in the economy overall. Tonight we also wanted to say condolences to all the Chicago Bear fans out there, tonight’s loss was, well disheartening to say the least!

Alright, we will be back with our settlement page highlighting the returns of the markets we follow so you can track along with us how each of the different sectors are performing. Also we wanted to give a shout out to the Money Machine Newsletter, they post trading examples, shares ideas and analyzes markets and data. The Substack can be found here,

As always do your own research and see what you think, but the work there may fit some of your styles and risk profiles, some 8,000+ investors start their week with Money Machine Newsletter's insights to get smarter about investing in stocks. It's free, it's fast, it's a no brainer—just your weekly dose of market-beating stocks in a 5-minute read.

Till next time.