The Debt Engine That Runs It All

Why fundamentals don't drive equity markets, who does, and what three decades of derivatives trading has taught us about the only number that actually matters.

Last week we examined the technical market landscape and returned to what we consider the singular most important driver of nominal asset prices -the global central banks, and in particular, the Federal Reserve.

We have demonstrated repeatedly that the Federal Reserve’s asset base has expanded at a staggering annualized rate of 9.7% over the past nearly three decades. To our knowledge, no mainstream or social media financial voice has consistently quantified and communicated this figure the way we have. This is the real inflation rate. This is the singular source of base money creation and that base money is debt.

It is this mechanism, compounding silently over decades, that has enabled the highly concentrated accumulation of wealth at the upper echelons of the economic spectrum -systematically bypassing the natural laws of fundamental economic principles.

This is precisely why we have long maintained that equity markets have little to do with the allocation of capital based on fundamental economic drivers. What matters is where the top 5% are deploying their debt-financed wealth. Understanding that single dynamic reframes everything you think you know about how markets work.

📌 Key Data Points

Since 2023, Magnelibra subscribers have had access to our proprietary data on what we call the MEGA9S -the top nine equities ranked by market capitalization. Over the past three years, we have heard the word “bubble” applied to these names repeatedly. We still hear it. Yet rarely does anyone offer a rigorous, criterion-based rationale for what actually constitutes a bubble in this context.

Is it simply the magnitude of the move? The fact that Nvidia is up over 14.5x -does that alone necessitate a reversion? This has always confounded us, because at any point along that extraordinary ascent, a trader could have made the same argument and been wrong. We are not immune to this ourselves on certain timeframes. But we are also consistent in pointing out that more traders have been carried out feet-first attempting to fade equity rallies — particularly in individual names like Nvidia — than almost any other strategy.

Nvidia holds a special place in our history. We have been swapping their graphics cards in and out of our trading systems since the early 2000s. It was not until their GPUs attracted the cryptocurrency mining community — specifically the memory-intensive proof-of-work algorithms where Nvidia’s parallel processing architecture excelled — that the broader market began to appreciate what we already understood about the hardware. The AI tailwind that followed was a logical extension of that same architectural advantage.

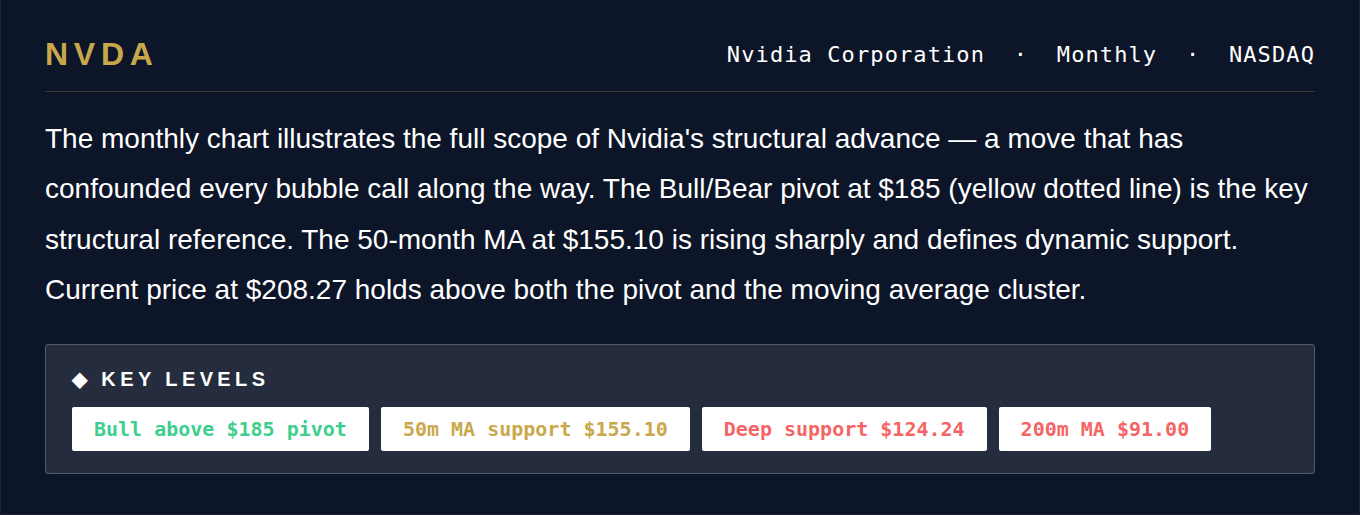

The consensus says bubble. But by what measure, at what level, and on whose timeline? This is why we anchor to our Bull/Bear pivot line as the structural momentum reference. For now, buyers have consistently demonstrated conviction near the $185 level:

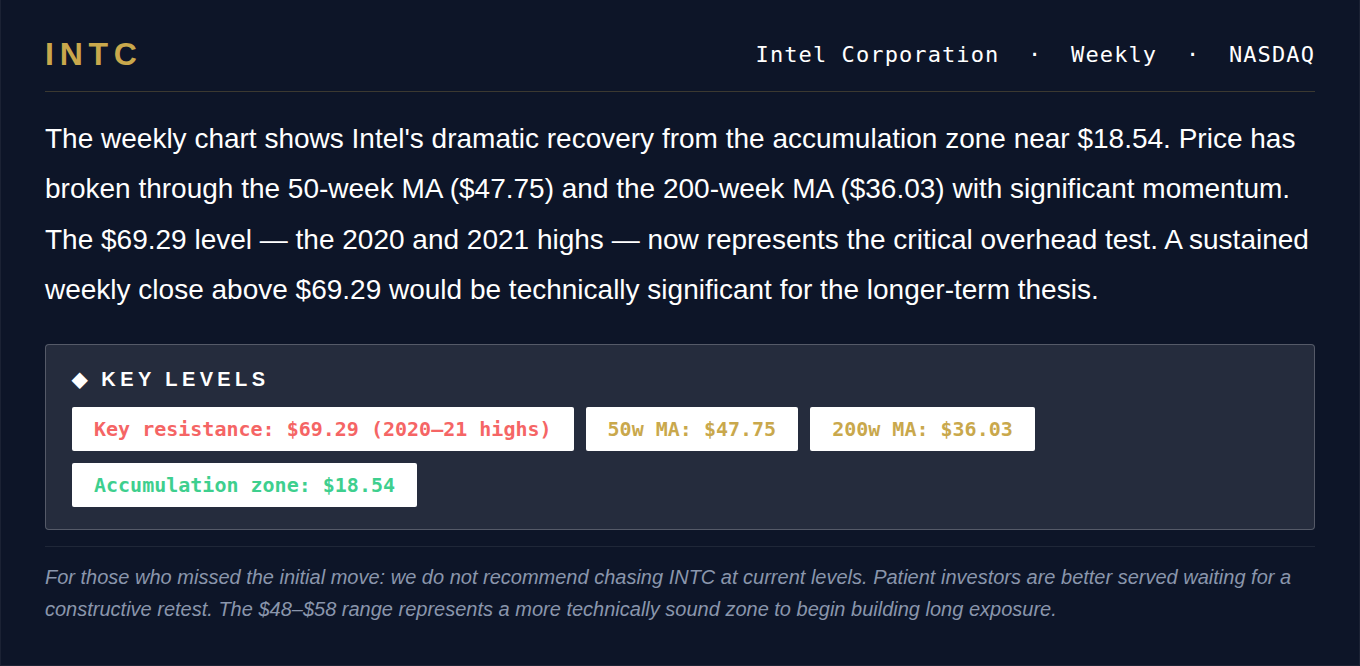

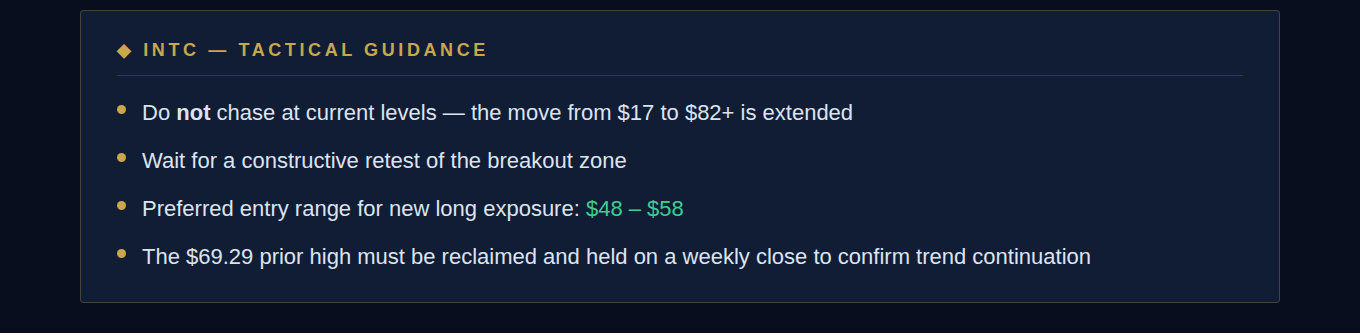

The second name we want to address is one we have been flagging for our readers since Intel traded near $18, a level that, at the time, represented extraordinary long-term value for a name of this pedigree.

Intel has received a meaningful boost from strong Q1 earnings, as the AI infrastructure tailwind has now reached the company in earnest, something we considered a matter of when, not if. However, we believe the prior structural high near $69, the 2020 and 2021 highs, represents the true test of this rally’s durability.

The equity markets continue their technically and AI-driven advance, and now you understand that in the long run, orthodox fundamentals are not the primary determinant of price. What determines price in the securities markets is whether the global central banks continue to expand their balance sheets through debt monetization — and who sits at the front of the line when that monetary spigot opens.

That front of the line is occupied by the large banks, hedge funds, and private credit operators. They receive this capital first. They leverage it. They deploy it in ways that systematically bypass conventional market principles, using their balance sheets to dominate flows across every tradeable instrument. Their algorithms are specifically engineered to identify the precise pain points of every market participant — and to exploit them.

Do not be discouraged. These participants are not competing for a few ticks. They are the semi-trucks on a two-lane highway. The skilled independent trader learns to read the draft, to move in the spaces between them, and to extract value from the spots the large players leave behind.

The Federal Reserve continues to be an active buyer of Treasury bills and is doing so in anticipation of moving further up the maturity curve into 5-year and 10-year securities once a new FOMC chair initiates a lower interest rate targeting regime. This is a question of timing, not direction.

If three decades of market analysis and derivatives trading has taught us anything, it is this: the top 5% do not ultimately lose. There are short-term drawdowns, episodes of apparent distress -but the global central bank infrastructure invariably provides the backstop, and the debt-monetary inflation cycle continues.

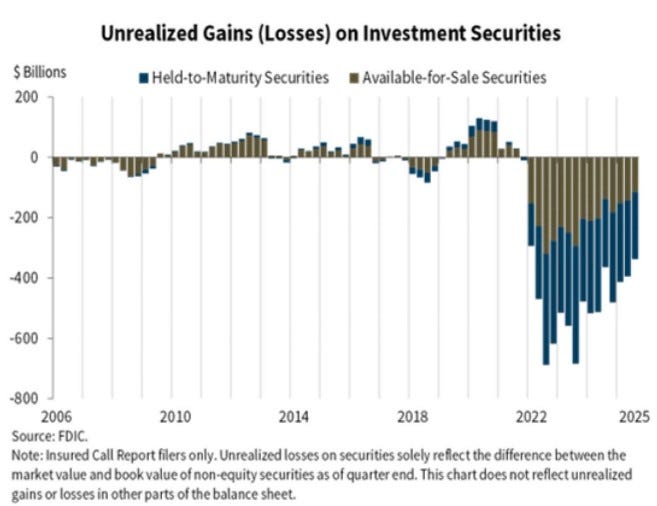

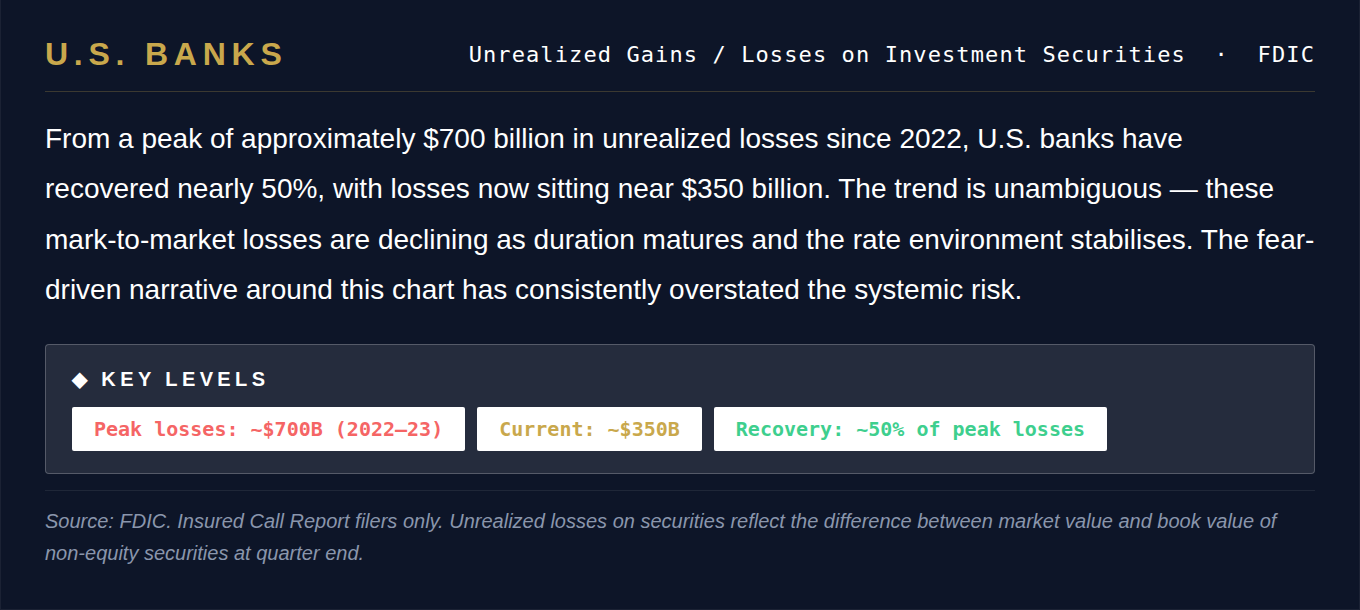

We frequently see the following chart circulating on financial social media of the unrealized losses on investment securities held by U.S. banks. A predictable cohort of fear-driven commentators use this chart to suggest systemic insolvency or imminent crisis. We have argued the opposite for three years and the data is proving us right.

We correctly argued for the past three years that these losses would be alleviated over time through a combination of duration maturity and a stabilizing to declining rate environment. Time and lower rates are the remedies and both appear to be in motion.

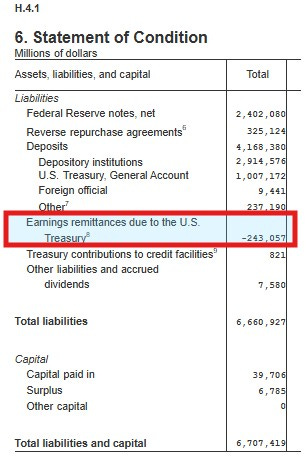

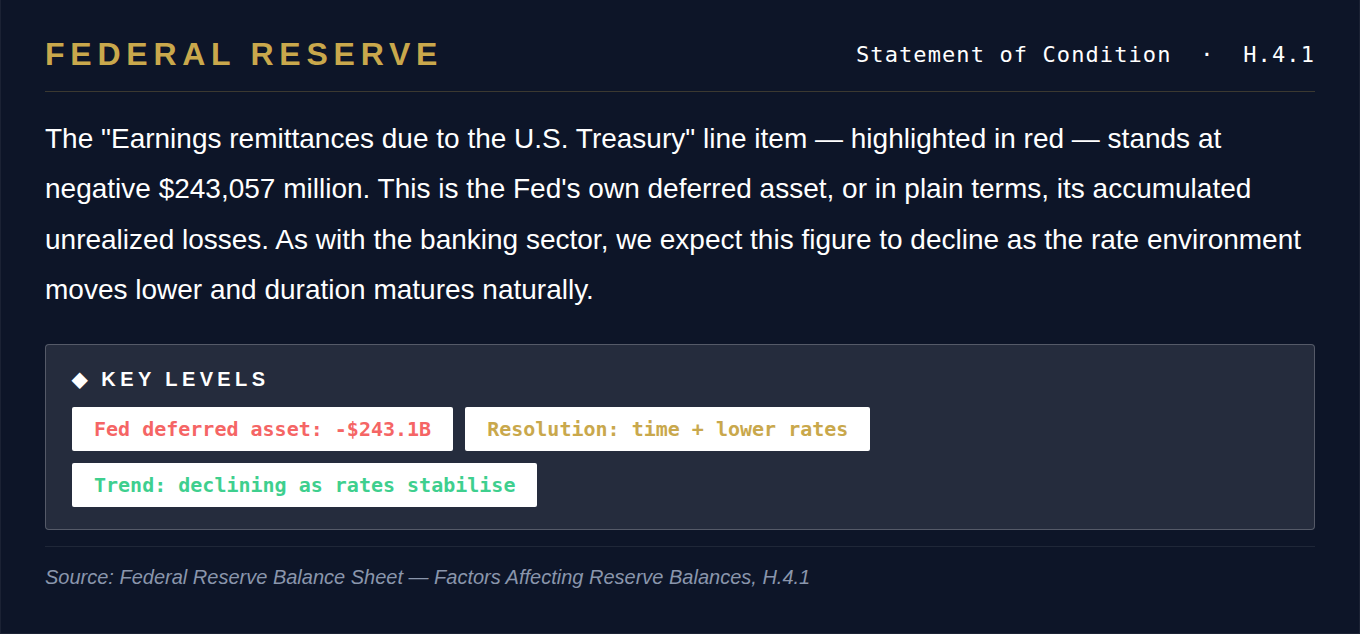

We expect the same dynamic to play out with the Federal Reserve’s own deferred asset, an accounting term for the Fed’s unrealized losses, which currently stand at approximately $243 billion:

We have considerably more analysis in our subscriber-only section, where we go deeper into U.S. Treasury markets and yield curves, equity and futures positioning, our proprietary data reports, and the full suite of markets we cover.

Our mission remains what it has always been to translate three decades of derivatives trading and institutional research into a clear, non-linear framework that gives you a genuine edge in understanding how financial markets actually function. We always encourage our readers to dig deeper. There are very few voices willing to convey this message with consistency and without agenda.

For trading questions, market setup discussions, monetary policy topics, or anything else on your mind, we are here. Subscribers can use the chat icon for direct access, or reach us via DM or email. Our goal is to help you sharpen your skills, become a more informed participant in these markets, and continue building together.

We genuinely appreciate every one of you for reading, for engaging, and for believing in what we are building at Magnelibra. Wishing you an excellent day ahead.