The New SAFE HAVENS

Technology - Future -Risk & Reality

We sent out our subscriber only note earlier highlighting our Global Futures Benchmark Program Positions Tracker. We are no longer including it with the free subscriber notes, so if you are an analyst, trader, investor, interested in tracking Magnelibra’s proprietary program than you should subscribe and can do so by clicking here:

As you know we have dedicated our lives to this and we know for a fact the way we analyze markets is unparalleled and we can tell you right now, employees at some of the biggest banks and funds follow us, Point72 and Goldman Sachs to list a few. Anyway the work we did back in the old days would be strictly guarded and held secret. Yet we have taken a more collaborative view point and have decided that we can’t hold everything so close, that our intention is much more expansive and we truly want to make you think differently, make you understand and see things differently so you can see thru all the Bull$hit out there that exists to sway your rationality.

With that we want to first comment on the massive out-performance of the Nasdaq Index in regards to virtually every other asset class (outside front running junk bond purchases by the FED) no, but honestly we are here today to teach you something very, very important. So pay attention, take a deep breath and know this is probably the most important letter you will read this year.

As a 20+ year veteran of financial derivatives, if its one thing we have learned and learned thru experience is that irrationality is and will always be an innate human trait.

With that is the absolute miscalculation by today’s algorithmic PHD quant community to try and fit statically everything into a theoretical vacuum construct. Sorry to tell you but financial markets don’t work that way, evidence of this should be the fact that the only way HFT survives is that it pays for latency arb and front running data feeds from end user suppliers like CME Group, TD Ameritrade, Schwab, Robinhood etc. without latency they wouldn’t exist, period. Ok so with that, understanding that humans are irrational, we can now clearly make it an axiom for our analysis that follows.

Markets are now controlled by Global Central Banks or more importantly the U.S. Federal Reserve. As they control both the quantity of money supplied as well as the equilibrium level of “short term” interest rates.

Mathematics defines our entire reality as we know it, even if you don’t know it, well we are here to tell you that quantum mechanics, tetrahedron quasicrystal theory will eventually prove this as it is already making massive strides. Anyway all throughout nature we find mathematical principles, the golden ratio in particular and with this nature as chaotic as it seems does exhibit fractal chaotic beauty and so we can also impose that at times even chaotic irrational markets will exhibit symmetry and synthesis as long as we are viewing thru the correct lens.

Now what do we mean the correct lens? Well traditional economics will tell us to value companies and equities thru multiple ratio’s, Quick, Current, Free Cash Flow, Weighted Avg. Cost of Capital, Tangible Book, Book to Sales, yadda yadda yadda. Fortunately for you if you really want to look at things correctly, you will only need to realize one thing, that at this singular moment in time,

NONE OF THOSE MATTER ANYMORE!

We have stated time and time again, that academic economists and even modern day analysts are all taught the same, thinking linearity and rigidity exist in chaos, well they don’t. So we need only look at point #1 from above and realize that we only need to focus upon what the Federal Reserve (SPV of the US Treasury now) is doing.

Not only are they supplying the funds and controlling the rates, they too now are directly purchasing assets. Now if that doesn’t solidify why old valuation metrics won’t work, put simply they have hijacked the markets.

These are NON ZERO SUM players, NEGATIVE WACC funded purchasers that can NEVER, EVER TAKE A LOSS.

Yes we know that as their balance sheet grows their Dv01 grows and the systemic risk gets amplified. Yes great, but none of that matters to present day, scalpers, investors and traders all that matters is whether its QE or not QE that is truly the only question!

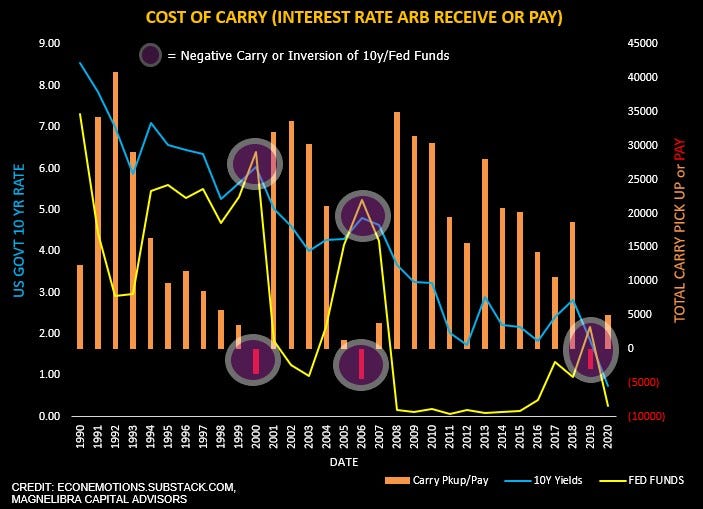

With all this we now present you with the holy grail of investing timing charts for those longer term players out there. We have shared similar charts in the past, but we have revamped it with a few more graphical points of interest. We are experts in fixed income arbitrage and this is not a chart you will see in the WSJ or any other Lame Stream Media publication. Its proprietary and unique but it points out very important inflection points over the last few decades.

Our highlighted circles depict those inflection points which we entitle “negative carry” or in simpler terms when the Fed Funds rate is above the 10 Yr rate or what many call “inversion.” Carry pick up or Pay is the fundamental principal of all interest rate arbitrage games and it is why the bond market will always be ahead of the stock market when it comes to real market forces driving capital flows. Well not to mention that its a much larger overall market. The last 3 inversion years are noted in the chart and are as follows, 2000,2006 and 2019:

There is clear evidence that hedge funds continue to under-perform the broader markets, well they stand no chance vs the Nasdaq, which we will explain why shortly, but the reality is they are too slow in realizing the system is rigged and they can’t afford to trust that.

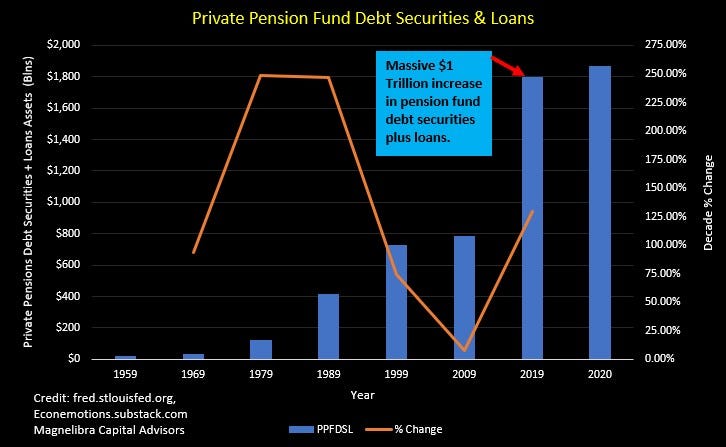

Well by not adjusting their mentality they have suffered and they have missed out on the reality that has been in place for over a decade. In fact they are only now starting to realize their folly, so too are the pension funds which as Calpers pointed out earlier this year, will now use leverage to obtain yield.

The reality of all this stems from the continued onslaught of negative equilibrium prices of real yields. The lower yields fall the further from reality pension funds become from their mandates which are stated at an actuarial level of 7%. This return is highly unrealistic in a negative real yield world, sorry but it is, and the fallacy of such expectations is manifesting itself before our very eyes.

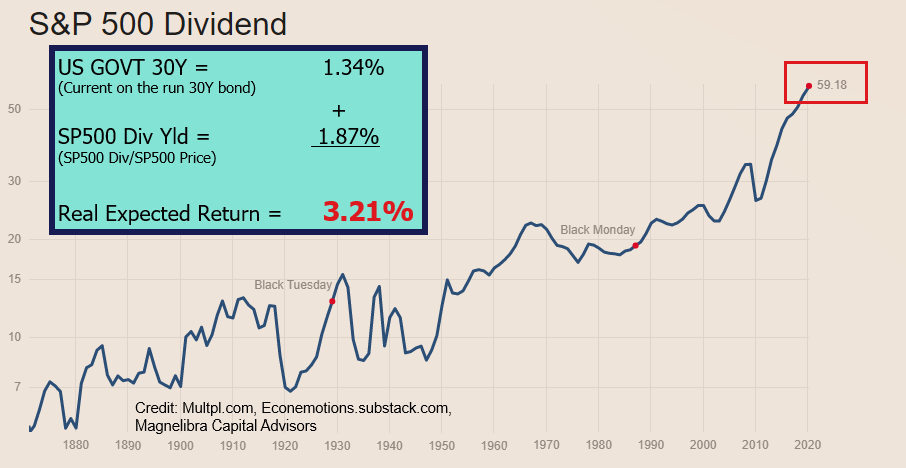

Magnelibra understands one thing very clearly when it comes to risk and reality. That is the longer term risk free return expectation is and should always be tied to a very simple equation which we have outlined here:

This equation is so simple, so beautiful and so true that we can now say for certain that a 7% return expectation given our inputs can only be achieved by reaching for yield thru one of two ports, riskier investments and or leverage. No two ways about it and thus the Pension Funds dilemma exists to the tune of more than 3.79 percentage points must be obtained via riskier outlets and leverage thus giving an added increase of overall loss given the economic and fundamental realities that under pin rational economics and everything we have been taught about corporate securities valuations.

Hell I wouldn’t want to explain this dilemma to a $50bln dollar pension fund and try to sugar coat it, you can’t and the treasurers, the fund managers they all know it, they are all complicit now and when things go awry as they always do, the value evaporation will be epic and scapegoats will be scarce. Furthermore we can see the pension funds distress in this little doozy of a chart we cooked up depicting the more than $1 Trillion in debt securities and loans within the private pension fund sector:

So that is our analysis of our fundamental economic conceptual backdrop. So with that we now want to touch upon the old “safe haven” bets of our prior reality. The majority will simply look at this as, where does the flow go when its “risk off” time? The traditional answer is and has always been out of equities and into bonds, well that is over to a certain degree. Those two asset classes are dominated by Central Bank QE flows either directly or indirectly. So where does that put us then. The obvious choice and its been this way for quite sometime but many continue to use the word “overvalued” when it comes to the Nasdaq Tech stocks. They will look at this excellent posted chart from Holger Zschaepitz and say, the FAANGMs are overvalued, how high can it possibly go?

Magnelibra always asks the question to a value investor when they posit statements like “investment X is overvalued, it can’t possibly be worth that!” to which our question is and will always be “Overvalued by what metric?”

You see what we are saying is that in a negative real yield environment whereby the majority of equities and bonds for that matter are fundamentally skewed via fundamental valuation principles where can one hide?

Well they are clearly hiding in the future of our world, in the companies that garner the most users, the most attention, the clearest shot at a technologically advanced world. Hey wait did we mention the massive amounts of cash hoard most of these techs hold as well? Bottomline:

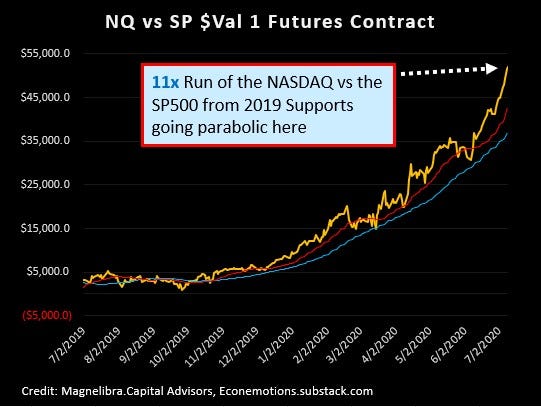

TECH STOCKS ARE THE DEFACTO NEW “SAFE HAVENS”

Here let’s look at our Nasdaq vs SP500 futures contract dollar value chart:

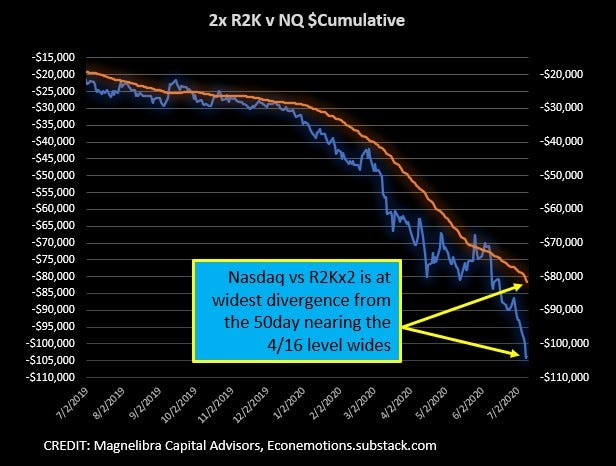

Now let’s look at the Nasdaq vs a 2x Russell2k chart and we would like to note the divergence from the 50 day MA is at its wide’s so any spreaders out there beware:

We know where everyone is hiding and rightfully so. So when your cohorts and friends ask if this stuff is overvalued, simply put the question back to them, “Overvalued by what metric? We can guarantee they won’t answer it rationally and certainly won’t have any data like you have now to back it up. This chart should solve any questions of why markets can rise despite 30m unemployed:

Moving on we have to look now at the US Govt 10yr chart which has backed off of that all important 58bp level we continue to target and outline so much:

We also wanted to include the Nasdaq Future which is nearing the top of the range channel and we suggest keep a close eye up here for a rejection:

Crude Oil continues to fail to close that gap, but we are still looking for a run up there to finally check that box off:

Finally we wanted to point out this chart of a new equity security, this company is doing something unique and when AI (artificial intelligence) is involved we have to take notice. Secondly insurance is a massive market and we can’t help but think a few big players will be put on notice plus we love the name LEMONADE INC:

OK feel free to share this letter, we have decided not to make this a subscriber only because we want you to share our fine work so we can grow our reach. We hope you got something out of today’s letter and that it helps you navigate our financial markets in a unique way. Feel free to share this as we pride ourselves in working with all of you in collaboration so that we all can benefit!

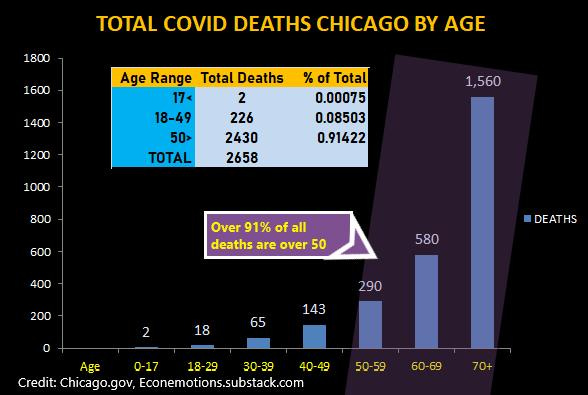

Good luck this week and before you go we wanted to leave you with the latest Covid data out of Illinois which is doing great in its fight to slow the spread and the proof is in the data, as well as a chart on some demographics on Chicago’s cases:

This chart should put the Covid Deaths from a risk pov into perspective:

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

I learned a great deal in about 12 minutes. Ty