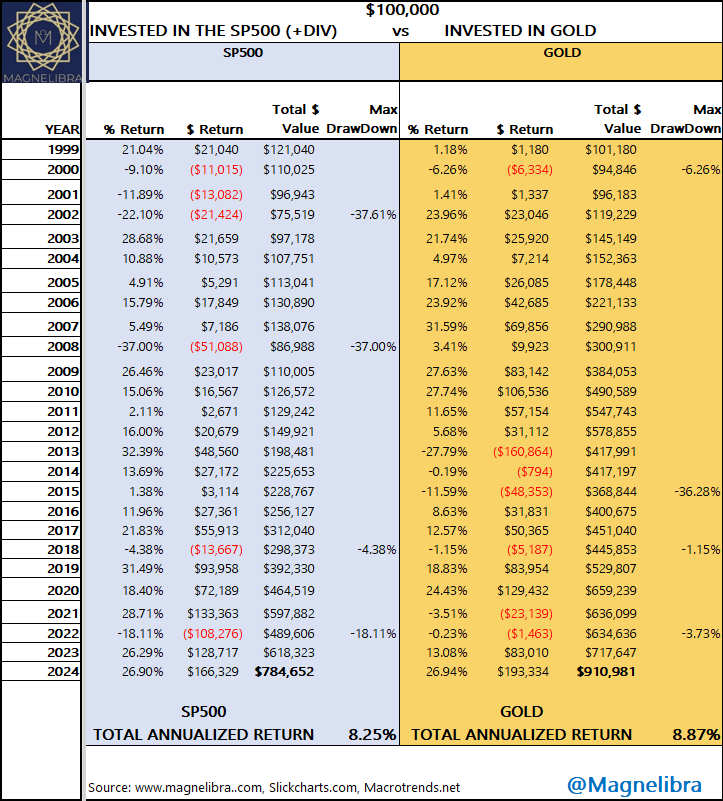

Time & Money -Favors Gold

This update is called Time & Money -Favors Gold and I entitled it because I was just reviewing the data that I have in regards to the last 25 years annualized returns. Not that I am shocked but in all honesty, the argument for owning a basket of equities in a portfolio vs owning physical gold, is well for all intents and purposes, dead to me. Now before I show you the data, I want to make something very, very clear. The basket of equities that I am referring to is an equal weight SP500 index fund. Now this has nothing to do with having individual equities in your portfolio, say the MEGA8s. In fact its why I prefer pooling the capital in a few names vs index funds. So just to be clear I am only talking about the annualized return of the SP500 vs Gold. Ok so without further adieu, here is the chart:

For me, this data tells it all, and its why Magnelibra’s expansive database that we have built is an excellent tool for calling out narratives. So we have a 7.5% greater relative percentage return.

What I continue to find is that the traditional ways of investing have changed into a more inflationary real asset return structured one than a traditional, let’s say 60/40 portfolio. The ramifications of this is that many have continued to underperform by warehousing their investments within long only index based structures. The typical structures offered via tax deferred outlets like traditional 401k and IRA structures. It seems to me that the future will continually advance toward more active style diversified approaches and away from traditional managed fund investing.

The future of investing will be coinhabited by advanced AI alpha chasing mechanized systematic programs, which by design go all in on alpha generating investments until they start to underperform and then they are shed for the “newest and shiniest” alpha generators. One thing that concerns us about this is the theory of diversification has been completely eliminated all together because you can’t have both diversified and alpha strictly driven processes. I suppose you can try to create a hybrid version of this, which is what we demonstrate by being an alternative strategy provider and offering you data to prove that you can hedge your long only equity exposure, that you can invest in alternatives, that you can hold physical cash or crypto and create your diversification that way. The buy and hold and the “spread it around” mentality is dead and it can be evidenced in the broader indexes underperformances toward let’s say the Nasdaq index, which is tech heavy and holds all the “in” stocks.

This is why year after year, you see wealth heavily concentrated in just a few names, in fact returns become self fulfilling in the post TARP, post Covid Stimulus world because the global central banks have hijacked traditional economic processes for one of monetary overwhelming mechanisms…Everyone talks about the FOMCs balance sheet and the $2Tn reduction off its highs and how the SP500 and Nasdaq continue higher…well what they don’t tell you is that the FOMC balance sheet is still 67% higher than it was 4 years ago and that move going from $4.1Tn to $7Tn is still the leading cause of asset price increase, because you can take that $7T an factor any multiplier you want to that and that is your real source of nominal asset prices. Its hijacked future potential and realized it forward to today, or robbing Peter’s futures earnings to pay Paul today!

None the less the writing is on the wall, the monetarist tool will always be the weapon of choice and its why time vs money is truly an important facet of investment that you have to understand. Right now the FOMC is smoothing time by reducing its balance sheet off its 2.25x highs from 2022 and has raised rates to sterilize home equity so it is not a source of inflation. That is another thing many don’t realize, I keep hearing about this massive equity in homes, well truth is it is immaterial because,

Its unrealized and untapped, therefor its theoretical utility

Its a nominal value based upon past pricing of an asset, the future holds no guarantee that the home bought in 2023 and valued at 2023 levels will be valued at those same levels in 2025 or beyond, 2008 is our proxy for that!

So no we do not believe in that home equity wealth effect at this point with where rates are. However as time goes on and all that supplemented income via credit card spending at rates of 25% or greater combined with say your 3% mortgage, well maybe the convexity refinance rate is closer to 5.5% than many think…meaning maybe mortgage rates have to only fall to 5.5% before we see our first real wave of home refinancing and equity extraction. However the big problem moving forward is that home owners are being assaulted on two fronts, taxation and insurance and I don’t see any of those going lower any time soon. So for me, the forces at play here that make people naively believe that housing always holds its value, well, they just ain’t lookin!

Ok so that is our time & money initial thoughts, I have so much more but this is already getting long.

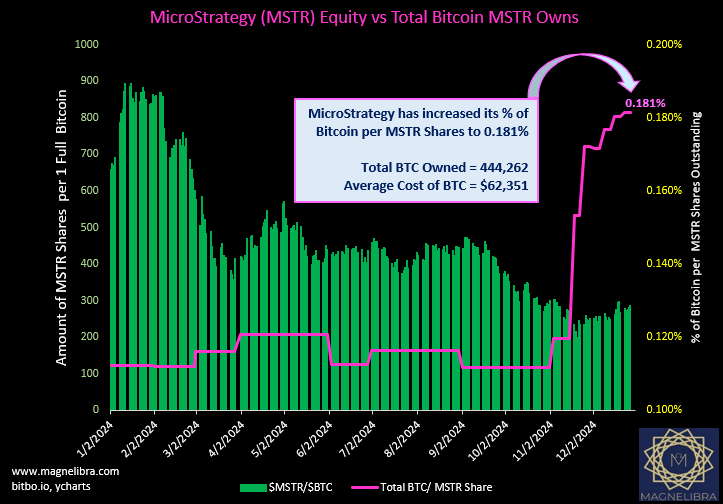

Let’s move over to MicroStrategy who just last week issued a Form Pre14A which is a request to shareholders to approve a 30.3x increase in the total authorized shares to 10.3bn from the current 330m. This is a vote for authorization, but doesn’t mean they will issue that many.

Its a clear attempt to assuage a market place with the specter of potential demand. I love Saylor’s plan, but I honestly think he’s 10 years too late. The factor return gets exponentially more difficult to obtain the higher the fiat the price goes.

Once bitcoin trades back to its 200 week, moving average, which it always seems to do MicroStrategy, will be lose billions. He should have begun this at a much lower price and even now should buy discounted BTC not buying at highs. When BTC does move back down, and BTC is well below his DCA (dollar cost average) price it could potentially cause them to have to liquidate bitcoin in order to pay their bond holders, should raising capital become difficult. The Bitcoin 200wkMA is down at $42k and MicroStrategy’s DCA is now $62,351:

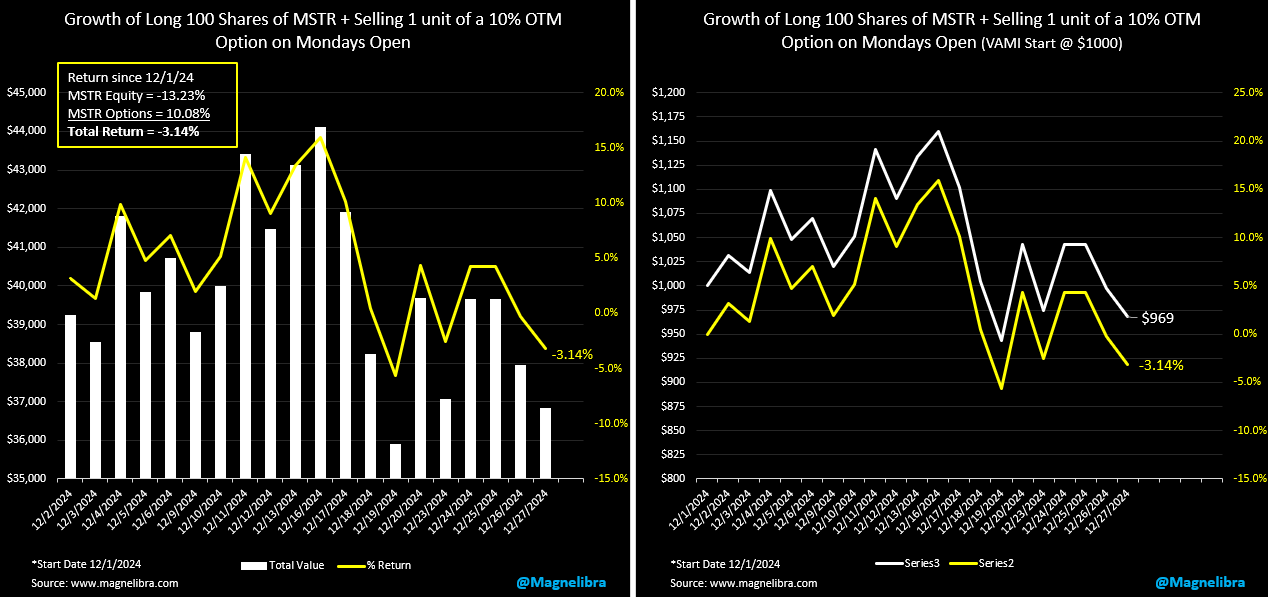

We cover this company and their ongoing gamma trade which is a volatility swap for owning the shares and the game that all the convertible bond holders are playing. We developed a simple tracker to monitor the stock vs the weekly volatility premium intake using the 10% OTM call option for that week. Here is the latest data, let’s just say the equity portion continues to exhibit weaker and weaker pricing, and we are certain that the announcement for an authorized share increase vote isn’t helping the stock:

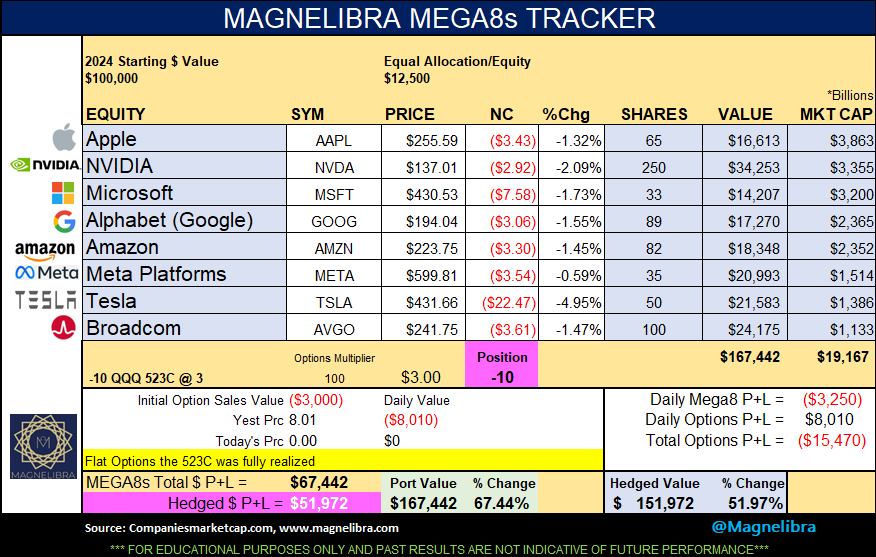

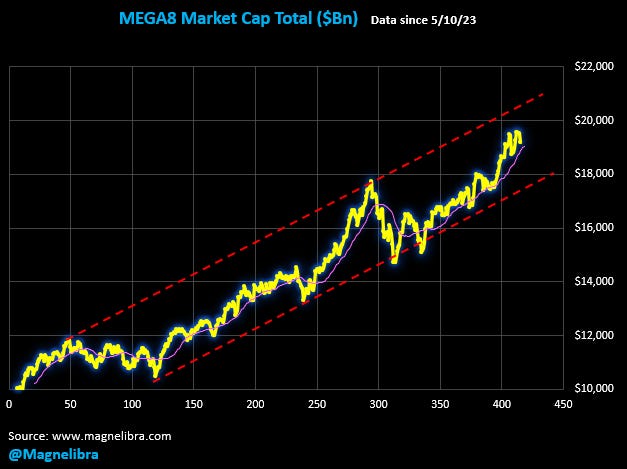

Ok, let’s move over to the MEGA8s and just so you guys know come the start of 2025 we will reset this tracker back to an equal weight of the top 8 mega cap stocks. The hedge for last week was the QQQ 523C and it expired worthless so full value on the premium there and the hedge did its job. We suspect 2025 to benefit from the hedges and add value to this long only basket, so we hope you decide to follow us along next year as well:

We will suspect this grouping to test the lower bounded red line some time next year:

This group has been in a solid uptrend for 2 straight years:

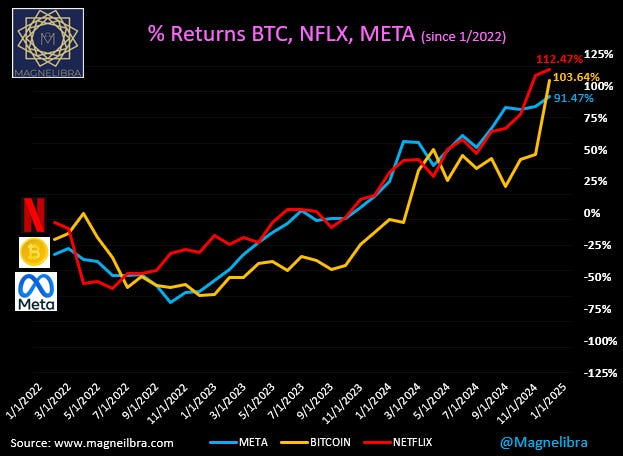

We also wanted to toss this chart out there comparing Netflix, META and Bitcoin, and when we talk about convincing some of these equity guys to buy into Bitcoin, well you can see, when compared to other well established assets, well BTC doesn’t look like such a huge outlier now, Netflix is actually a better performer since 2022:

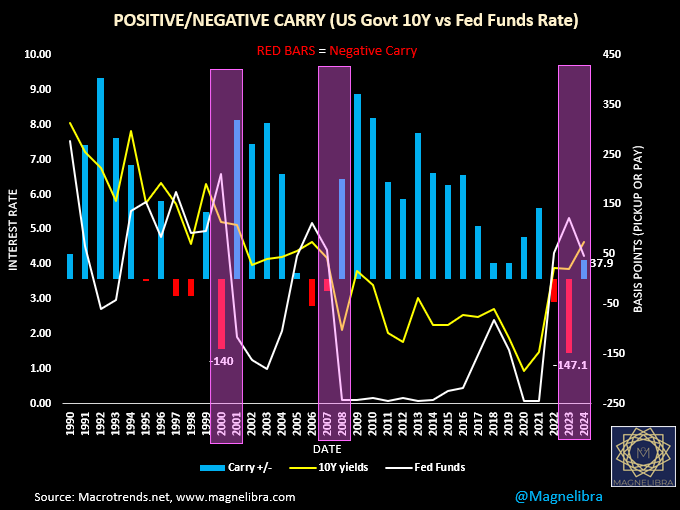

One thing I want you guys to keep an eye on and a very important data point that we know your other friends and colleagues do not have, that is unless you share our work with them (which you should) is this next chart. This is the US Govt10y vs the Fed Funds chart, this is now out of negative territory and we suspect, this will have some major implications for global assets:

This is a very important turning point in the market and one of the main reasons we believe volatility will be high in 2025!

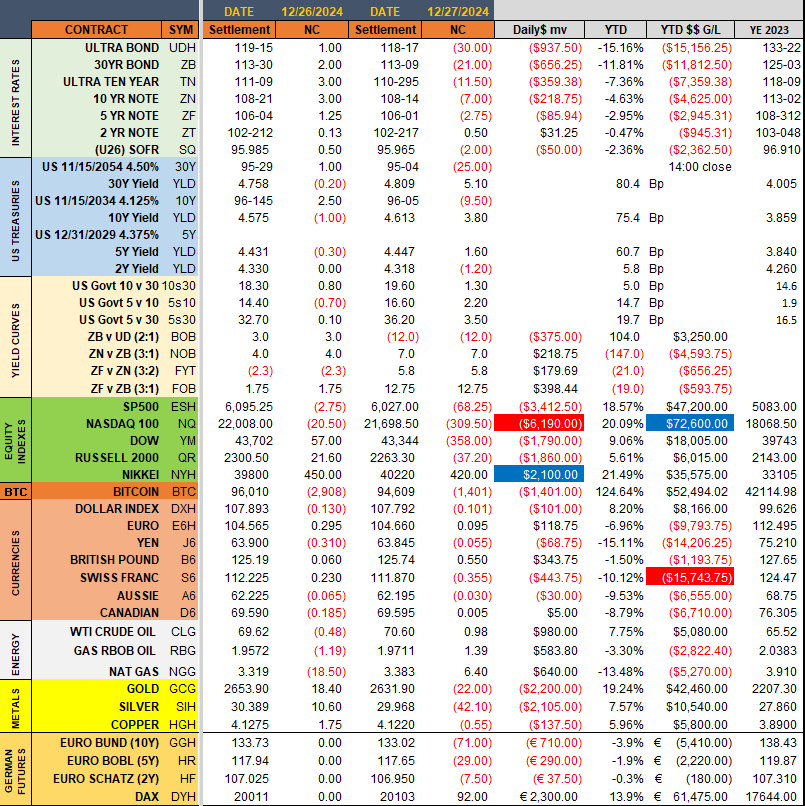

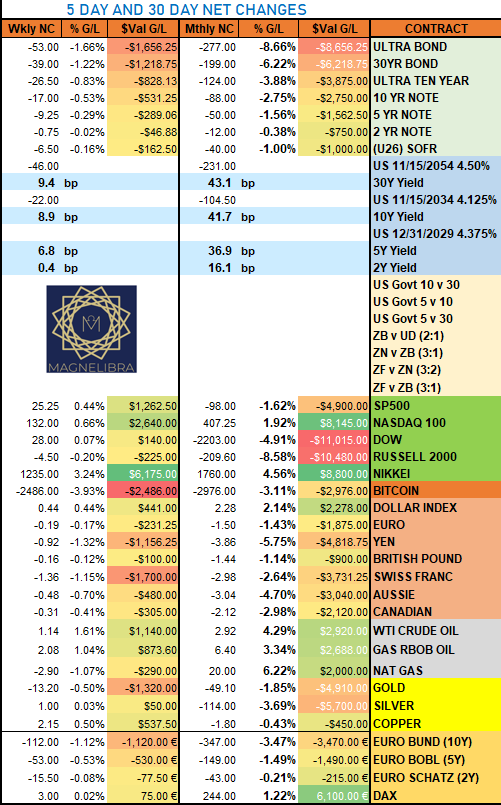

Ok lets go with the settlements page now:

The Russell2k and the Ultra bond are the big 30day losers falling -8.58% and -8.66% respectively and the winners are Nat Gas and the Nikkei +6.22% and +4.56% respectively:

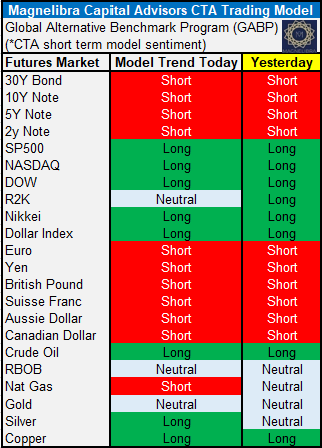

As far as our Magnelibra CTA market sentiment tracker we have a move out of the R2k into neutral land, Nat Gas moved to a Short and silver is back into a Long:

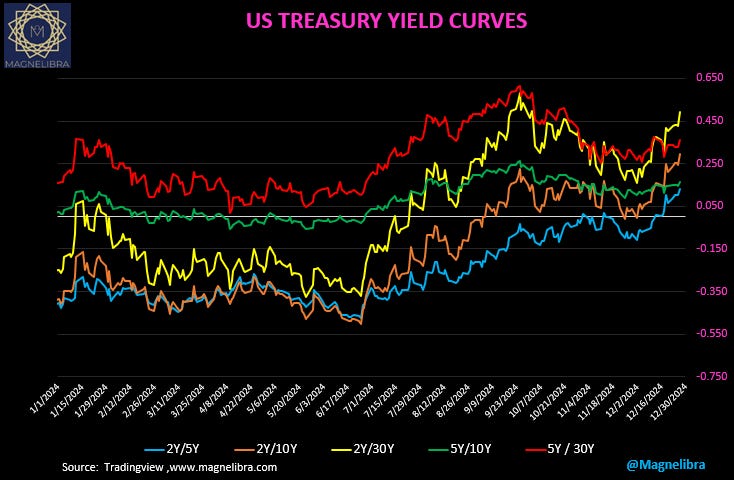

Finally let’s look at the US bond market and curves. What we have seen transpire in the bond markets is truly unprecedented, as yields have shot straight up in the longer ends of the curve. Now we believe a lot of this has to do with the stronger USD putting pressure on emerging markets that have to sell their US Treasuries to close their funding gaps and underperforming economies. None the less here are some of the charts. This first one is the US yield curves moving back to their more normal distribution of steepening in the curve as all the spreads are now positive:

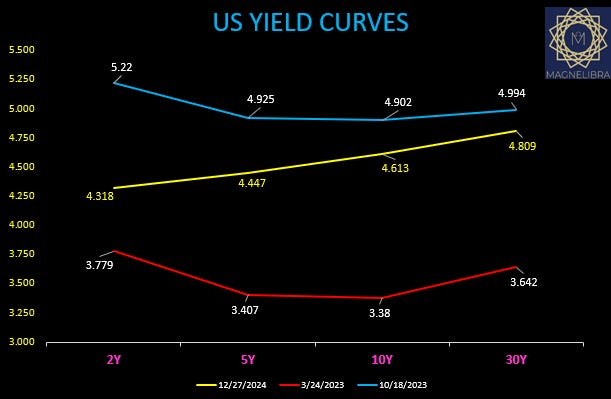

Here is the high and low levels in regards to overall yields, and the yellow line is the present day value of where the yields are respectively:

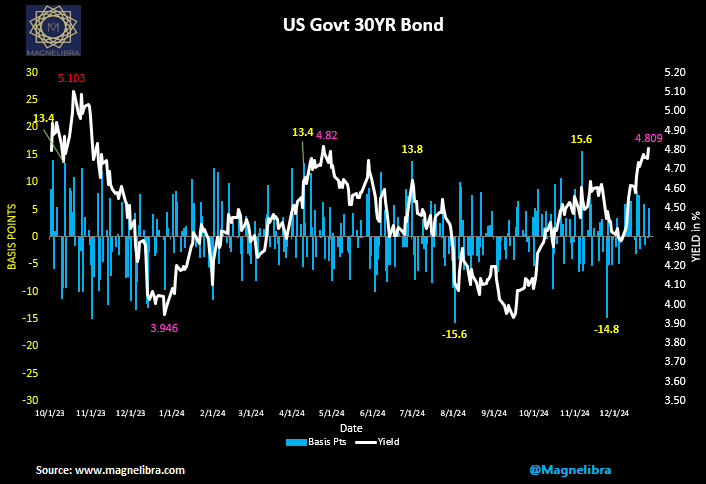

Here is the US Govt 30Y pushing its early Q2 2024 closing highs and +90 basis points since their Sept. lows:

I feel this is all great timing for a rotation out of equities come Q12025 and into some of these longer end structures. I am not sure of the real catalyst but I would suspect there would be natural sellers come January and February looking to take profits and defer tax payments on those capital gains for another year. Anyway those are just a few of our thoughts and I hope that you guys guys take it all in and digest all that I say.

There is a lot to look forward too in the coming year and we are excited to continue to bring you fresh perspectives and maybe for those playing along with our trackers and creating their own trading and investing ideas. I look to continue to add value for you guys and all in all I honestly do believe the data that we present, the manner by which we present it is hopefully adding the value I think it can into your lives. Anyway Happy New Year to all of you.

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of or from Magnelibra Capital Advisors. Magnelibra the Commodity Trading Advisory and its proprietary long/short commodities, futures and options managed accounts may hold long and or short positions in the various futures and markets that Magnelibra covers. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed. If you are interested in opening an individual managed futures and options account to compliment your overall investment portfolio you can visit our website at https://magnelibra.com for more information. We are implementing a new trading program launching at the start of the new year, which will include access to Bitcoin futures and options. Please contact or make inquires directly to our introducing broker Capital Trading Group, please contact Nell Sloane at nsloane@capitaltradinggroup.com

All Rights Reserved Magnelibra Capital Advisors LLC 2024