U.S. Banks -Bigger is Apparently Better & Safer

I am just amazed at how concentrated the total deposit base has become in the U.S. I thought all the GSIB, BASEL, Dodd Frank regulatory promises would lead to a greater dispersion of deposits not the opposite. It seems like the plan for reducing global systemic risks in the banking sector has given a way to making them even larger and more dominant. The latest data is quite alarming and not sure how Dodd Frank is being circumvented here but it is…Bigger question is why the FDIC, Federal Reserve and US Treasury are not intervening or at least commenting on this massive concentration of US deposits, exactly how is bigger better or even worse of a question, how is does this reduce overall systemic risk?

Here are a few of our concerns that Magnelibra has:

Antitrust concerns:

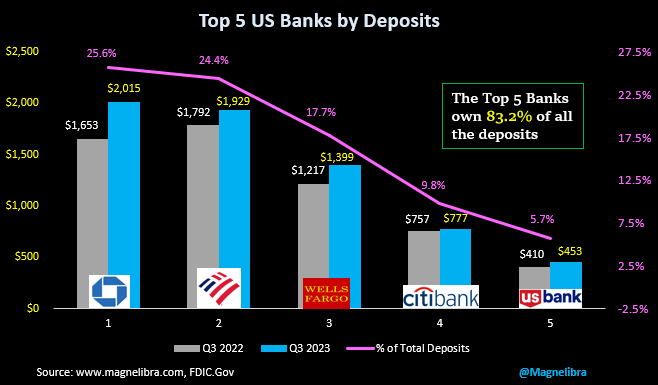

Dominant market share: With 25.6% of all US deposits, JPMorgan Chase has a considerable market share, potentially limiting competition and innovation in the banking sector. Smaller banks may struggle to compete for deposits and customers, stifling their growth and reducing consumer choice.

Barriers to entry: The sheer size and resources of JPMorgan Chase can create significant barriers to entry for new players in the market, further solidifying their dominant position and hindering competition.

Predatory pricing and practices: Concerns exist that the large banks might leverage their market power to engage in predatory pricing or practices, disadvantaging smaller competitors and ultimately harming consumers.

Too big to fail concerns:

Systemic risk: The interconnectedness of the financial system means that the failure of a large bank like JPMorgan Chase could trigger a domino effect, posing significant risks to the broader financial system and potentially necessitating government bailouts. (The poster child of this throughout the GFC was Deutsche Bank!)

Moral hazard: The implicit "too big to fail" perception surrounding large banks creates a moral hazard, incentivizing them to take on excessive risk as they assume they will be rescued by the government in case of failure. This can lead to financial instability and potentially higher systemic risks.

Reduced resilience: The dependence of a large portion of the financial system on a single institution can weaken overall resilience and make the economy more vulnerable to systemic shocks.

Policy considerations:

Addressing these concerns might require a multifaceted approach involving both antitrust and financial regulatory tools:

Antitrust enforcement: Enforcing existing antitrust laws to prevent anti-competitive practices and promote a level playing field for all participants in the banking sector.

Capital requirements: Adjusting capital requirements based on bank size and systemic risk profile to incentivize responsible risk management and discourage excessive deposit concentration.

Liquidity regulations: Enhancing liquidity regulations to ensure banks have sufficient resources to weather financial shocks and reduce the risk of contagion in case of failure.

Structural reforms: Exploring potential structural reforms to reduce the size and interconnectedness of large banks, potentially including divestitures or restrictions on deposit concentration.

We believe the financial regulators are complicit and seem to be circumventing the rules that already exist. Section 165 of Dodd Frank clearly sets a 10% threshold for one banks deposits as it relates to total deposit base. This is being completely ignored and done on purpose. The regulators should be promoting competition, maintaining financial stability, and protecting consumers remains a key challenge for policymakers. It seems strange that this would be the case today after a decade of ZIRP and QE, but its a concern from the investment side because Too Big Too Fail has now become WAY TO BIG TOO FAIL! Don’t think for one minute the likes of these big banks aren’t playing balance sheet games in the financial markets and playing 3 Card Monte with their overall systemic risk!

We will be back with more in our podcast later, subscribers that are following our MEGA8 Tracker our educational long only hedged program, you will see a new hedge on today’s tracker it is the 12/29/23 expiration 408 Call at 2.50. We liked the nice pop in the market thus far to work off yesterdays massive late day move. Here is a current snapshot of where things are currently:

The US Bond market is seeing yields up slightly and equities are green thus far:

As far as the other markets, FX is higher, with Crude and RBOB lower and Metals up slightly.

We will be back later.