U.S. Treasury Bonds on Fire vs Short End

A trading lesson in treasury curves

Alright today we had some hot CPI and PMI numbers out of Europe and China and this has led to a continued inversion in the U.S. Treasury curve. Now for new readers that might not know what an inversion is, it is when shorter dated maturities like a 2Y and 5Y maturity have higher yields than say longer maturities, 10Y and 30Y bonds.

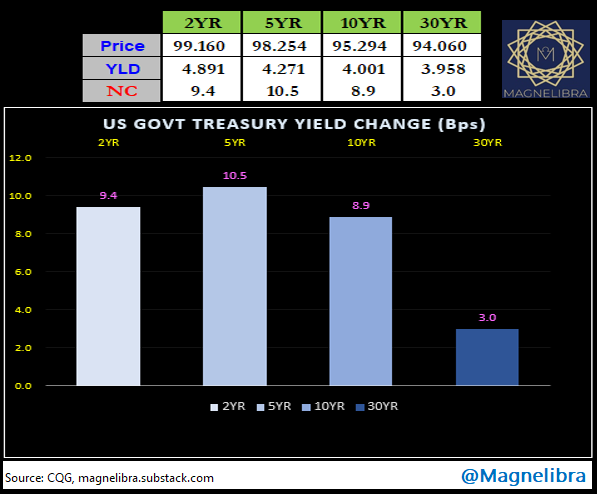

We have seen the quickest rate hikes in history and with that comes a very large inversion as seen in the 2Y vs 30Y complex whereby the U.S. Govt 2Y yield is 4.886% while the yield on the 30Y is 3.955% or an inversion of 93.1 basis points.

This inversion is very much an indication of higher short rate trajectories and are a result of the global central banks pushing short rates like the Federal Funds rate up to 4.75% which is up from the basically zero bound. Further exacerbating these curves are global bond market players that are driving longer dated securities like the 30Y bond down in yield as they know, eventually the central banks will cave and have to lower rates again. Well this has been the regime for quite some time, but as we have discussed in this letter time and time again, that regime has changed.

The global central banks for far too longed have used artificially low rates, coupled with massive amounts of quantitative easing (asset purchases) which have distorted the natural equilibrium of both cyclical economics as well as global interest rates.

We noted last year that QE combined with unprecedented fiscal monetary response out of the US Treasury directly to tax payers would lead us to an the kind of inflation that is “sticky.” Far too much capital, to then be concentrated in far too little of hands coupled with a supply chain disruption post Covid would usher in a new era by which all of this stimulus would lead to asset price appreciation, goods and services appreciation and housing appreciation…Now that time is over…all of that chasing has subsided and reality has started to set in, yet this time around global central bank balance sheets are about 4x from a decade ago and all taking marked to market losses on their securities that they hold.

We feel that this puts global central banks at a major disadvantage vs existing market forces and that higher rates are not a result of wanting to cull inflation but are a direct result of global central bank policy, that for far too long has allowed overleveraged entities to exist and continue to push market fundamentals far past equilibrium.

We know now that the big hope is on a large influx from China’s “post Covid reopening,” however we feel that too will be short lived and rather we will use the INVERTED YIELD CURVES, to tell us how time and time again, history has shown that recessions are soon to follow!

Let’s take a look at today, where the U.S. Treasury long end, the 30Y which started to show real strength yesterday vs the shorter end today, has all but left the short end in the dust as the 30Y trades at 94.06 a yield of 3.958% +3bp while the 5Y is 4.271% +10.5 basis points on the day: